- Netflix dropped after Q1 2023 earnings

- Headline results in-line with expectations

- Subscriber growth slowed significantly

- Free cash flow surge as content spending dropped

- Stock pulls back but remain within upward channel

Netflix (NFLX.US), US video streaming company, reported Q1 2023 earnings earlier this week and they turned out to be a disappointment. While headline results were mostly in-line with expectations, slowing subscriber growth raised concerns and triggered a drop in company's shares. However, was the report really that bad? Let's take a look at the details.

Q1 results come in-line but forecasts disappoint

Looking at headline Q1 2023 results released by Netflix on Tuesday after market close, one may struggle to understand why post-earnings share price drop occurred. Earnings and sales were mostly in-line with expectations. However, a key metric for Netflix - subscriber additions - disappointed as the company added just 1.75 million new subscribers in the period, compared to 2.3 million expected. Moreover, the company issued disappointing guidance for Q2 2023 that points to lower earnings, sales and new subscriber additions. On the other hand, the company said it is on track to meet its previous full-year financial objectives and full-year free cash flow was boosted from around 3.0 billion USD to at least 3.5 billion USD.

Q1 2023 earnings highlights:

- EPS: 2.88 USD vs 2.86 USD expected (3.53 USD in Q1 2022)

- Net Income: 1.305 billion USD vs 1.29 billion USD expected (-18.2% YoY)

- Revenue: 8.16 billion USD vs 8.18 billion USD expected (+3.7% YoY)

- Free-cash flow: 2.116 billion USD

- Paid memberships: 232.5 million vs 233 million expected (221.64 million in Q1 2022)

- New subscriber additions: 1.75 million vs 2.3 million expected (-0.203 million in Q1 2022)

Q2 2023 forecasts

- EPS: $2.84 (exp. $3.08)

- Revenue: $8.24 billion (exp. $8.47 billion)

- Subscriber additions to be similar to Q1 2023

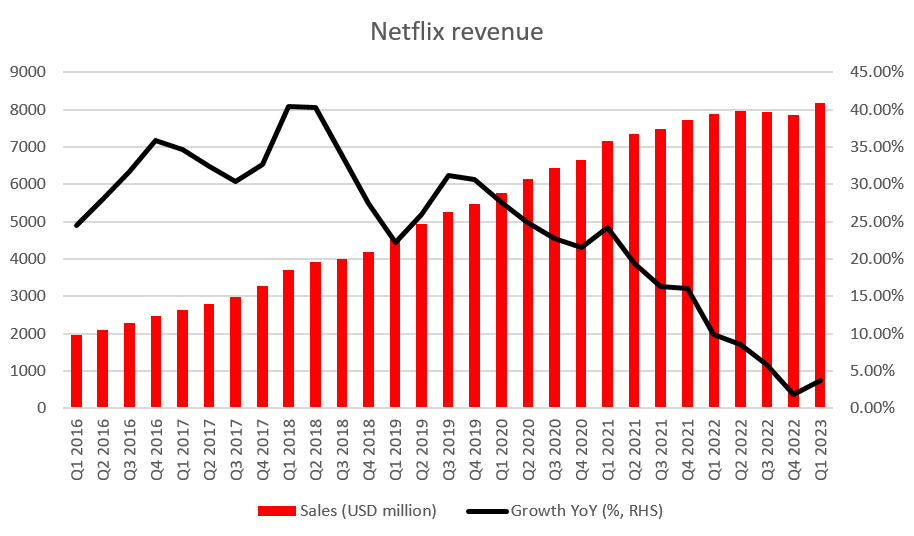

While Netflix revenue growth has improved compared to Q4 2022, it was still one of the slowest in the past couple of years. Source: Bloomberg, XTB Research

While Netflix revenue growth has improved compared to Q4 2022, it was still one of the slowest in the past couple of years. Source: Bloomberg, XTB Research

Password-sharing crackdown postponed

Netflix has been finding it harder and harder to attract new subscribers. There are a number of reasons behind it - rising costs of production that limit the number of new titles produced and streamed on Netflix platform as well as rising competition in the industry. The latter is especially true as video streaming companies start to sign exclusive deals with major film production studios, meaning that customers now have to subscribe to at least a few different platforms if they want to have access to well-known classics. As such, account-sharing has been on the rise and Netflix estimates that as much as 43% of users share their passwords with others. Netflix vowed to crack down on this for a long time as putting an end to account sharing could help review subscriber growth, or at least boost profits via introduction of paid sharing schemes. Actions were expected to be taken in Q1 2023 and positively impact results as soon as in Q2 2023. However, the company announced that it decided to postpone the crackdown until Q2 2023, meaning that expected subscriber boost will occur later in the year, and it looks to be the prime reason behind weaker Q2 2023 forecasts.

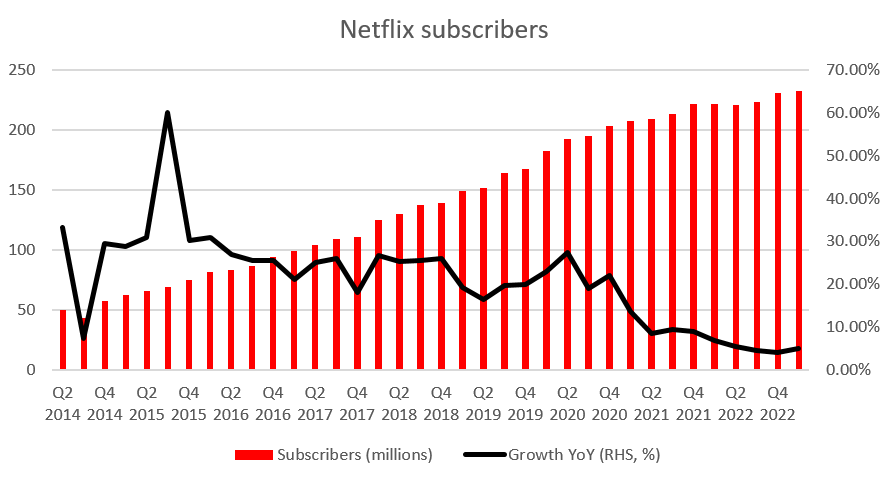

Netflix's subscriber growth slowed significantly as competition in the video streaming industry and costs increased. Company hopes that a crackdown on password sharing (now expected in Q3 2023) will help revive it. Source: Bloomberg, XTB

Netflix's subscriber growth slowed significantly as competition in the video streaming industry and costs increased. Company hopes that a crackdown on password sharing (now expected in Q3 2023) will help revive it. Source: Bloomberg, XTB

Free cash flow surge to boost buybacks?

One of the positive highlights of Netflix Q1 2023 earnings release is a massive surge in free cash flow. Company reported $2.12 billion in free cash flow for the quarter, the highest on record, driven by 2.18 billion in cash from operations, also the highest ever. Jump in operating cash flow came as companies spent less on content assets ($2.45 billion in Q1 2023 compared to almost $3.6 billion in Q1 2022). Netflix plans to keep content spending in check and decided to boost full-year FCF forecast from around $3.0 billion to at least $3.5 billion. This is probably the most important takeaway from the earnings release when it comes to share price outlook as higher free cash flow would allow Netflix to engage in more buybacks.

More prudent content spending led to a surge in Netflix operating cash flow, which has driven a spike in free cash flow. Source: XTB Research, Bloomberg

More prudent content spending led to a surge in Netflix operating cash flow, which has driven a spike in free cash flow. Source: XTB Research, Bloomberg

A look at the chart

Netflix slumped over 10% in the after-hours trading on Tuesday. However, this drop was trimmed ahead of the Wall Street session opening on Wednesday after company's executives soothed investors' concerns a bit during earnings call, for example by saying that rollout of paid sharing scheme has gone well in countries that already saw it and will be continued on most of company's markets in Q2 2023. Ultimately, stock launched Wednesday's trading with a rather small, around-3% bearish price gap.

Taking a look at Netflix chart (NFLX.US) at D1 interval, we can see that the stock has been trading in an upward channel since mid-2022. What looked like a potential upside breakout in January-February 2023 period was halted at resistance zone marked with 38.2% retracement of the 2021-2022 slump and the stock returned back below the upper limit of the channel later on. Share price tested $320 support zone after earnings and so far it looks like bulls have defended it.

Source: xStation5

Source: xStation5

Palo Alto acquires CyberArk. A new leader in cybersecurity!

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

US jobs data surprises to the upside, and boosts stocks and pushes back Fed rate cut expectations

Market wrap: Oil gains amid US - Iran tensions 📈 European indices muted before US NFP report

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.