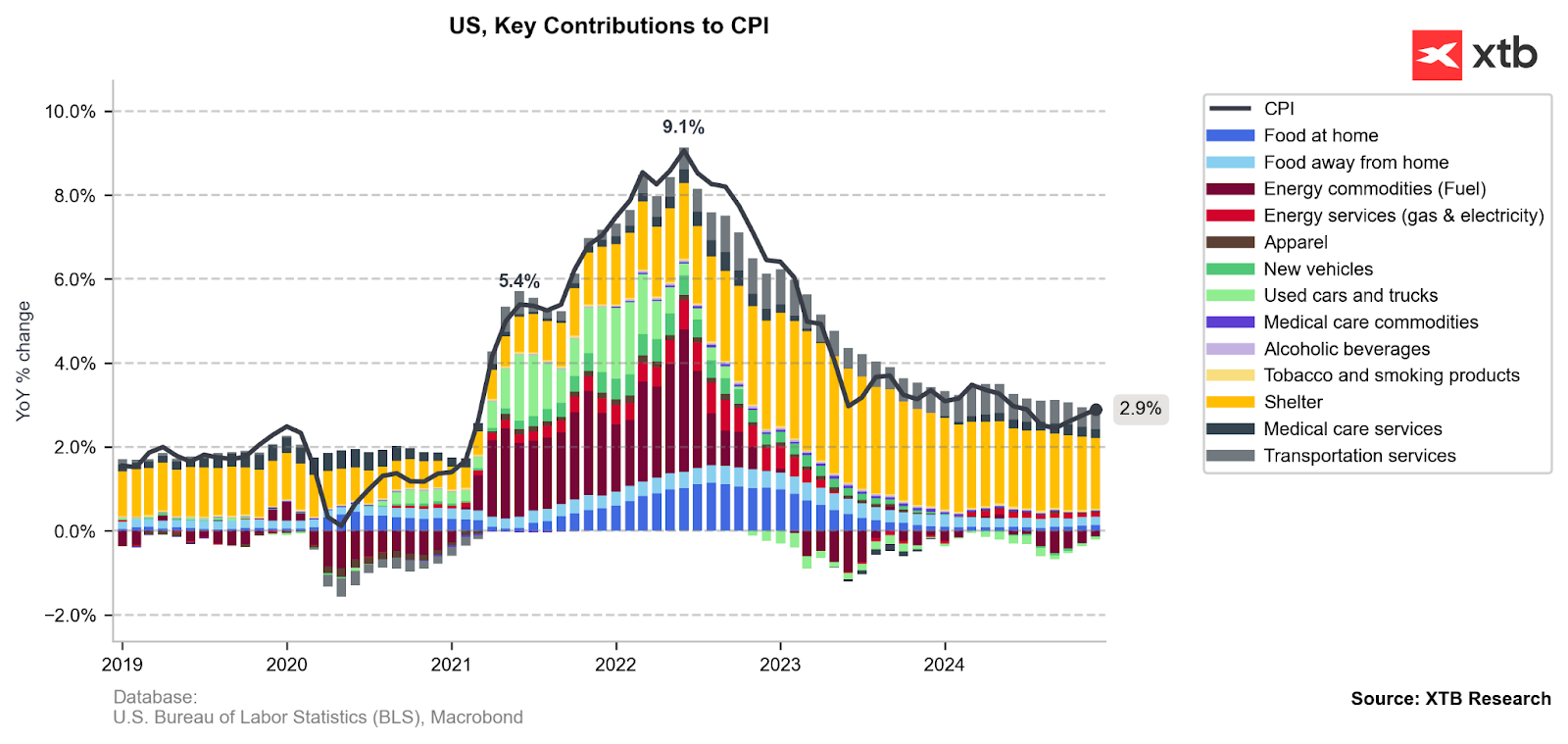

Today’s CPI report delivered another downside surprise, echoing yesterday’s producer price index data. Headline CPI rose in line with expectations to 2.9% year-over-year and 0.4% month-over-month, but core measures came in below forecasts and below previous reading. Core inflation eased to 3.2% year-over-year from 3.3% previously, while the monthly figure showed a 0.2% increase, compared to the 0.3% expected. Core inflation is a key metric for the Federal Reserve, as it strips out the most volatile components, such as energy and food prices.

The higher headline CPI figure is primarily attributable to the minimal negative impact of fuel prices. Over the past several months, fuel and car prices have been exerting downward pressure on inflation. However, this negative contribution is now minimal. It is conceivable that we may see a positive contribution from fuel prices as early as January. On the other hand, it is important to remember that this is linked to the volatility of commodity prices.

The negative impact of fuel and car prices is now marginal. On the other hand, we continue to see a diminishing impact from shelter inflation, which is helping to restrain core inflation. Source: Bloomberg Finance LP, XTB

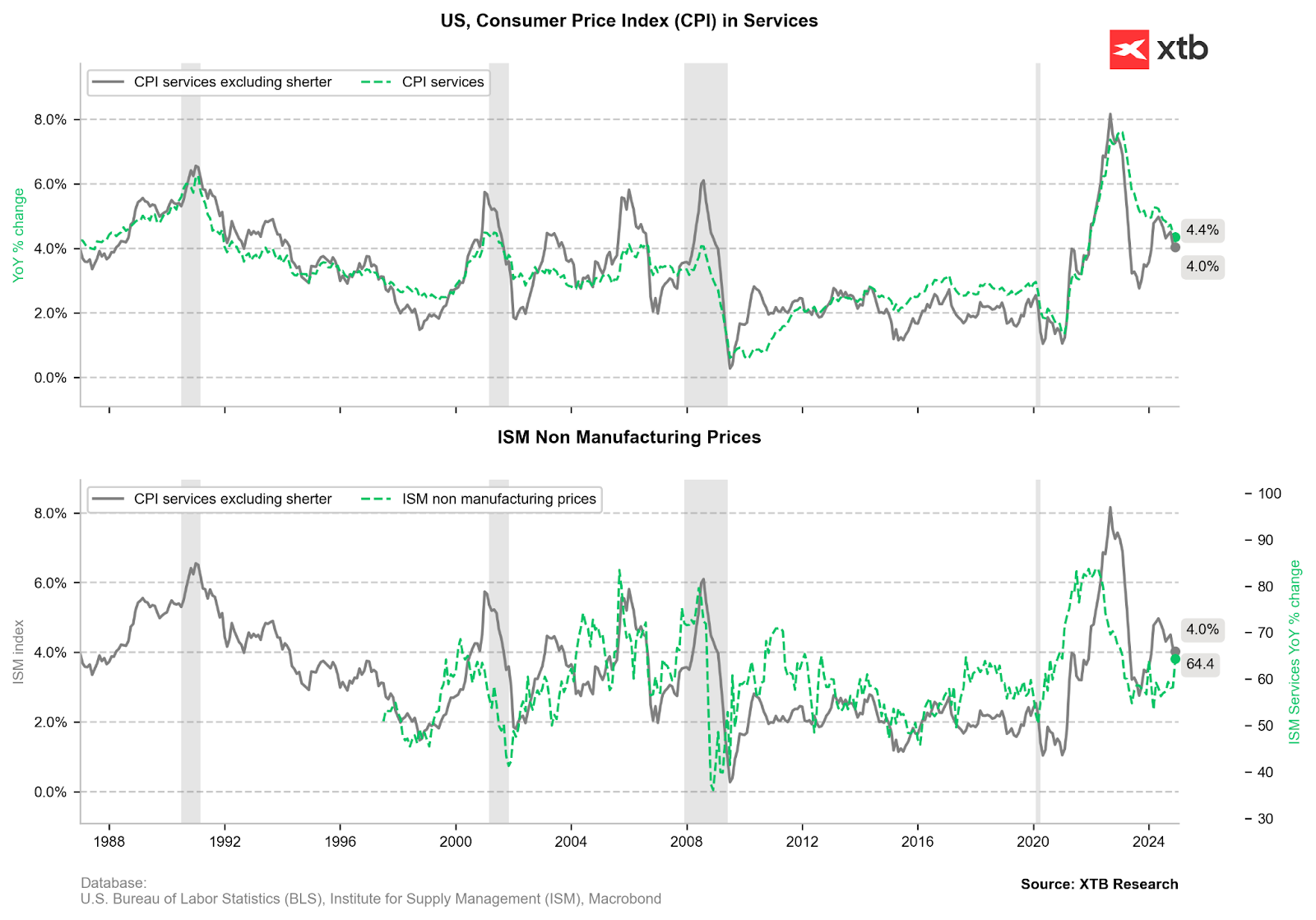

A positive development is the decline in services inflation, including shelter. Of course, both of these measures remain very high compared to their levels in the 2010-2020 period, which were close to 2%. Moreover, the sharp rise in the price sub-index from the ISM services report raises concerns about a resurgence of inflation in the near term. Source: Bloomberg Finance LP, XTB

Market Reaction

The market is reacting with considerable euphoria. EURUSD is rising and testing the 1.0350 level, even though the pair fell below 1.0200 at the beginning of this week. This is due to the pricing in of a full rate cut in the first half of this year, whereas previously the market was not pricing in the first cut until September. In addition to a cut in the first half of the year, the market is also pricing in a cut at the end of the year with a 50% probability. Nevertheless, in the near term, inflation could be very volatile, given energy and food prices, which may depend heavily on future Trump policies.

The US500 is rebounding by more than 1% today, just before the cash session opens. This is the third potential day of gains for the index futures contract. We are also seeing the largest increase in bond prices in a long time. The US500 is approaching the 6,000 point level, but first it must decisively break above the falling trend line and the 38.2% Fibonacci retracement level. Source: xStation5

Economic calendar: NFP data and US oil inventory report 💡

Morning Wrap: Dollar in a trap, all eyes on NFP 🏛️(February 11, 2026)

Daily summary: Weak US data drags markets down, precious metals under pressure again!

US Open: Wall Street rises despite weak retail sales