- Alphabet, Microsoft and Intel to report earnings today

- Reports will be released after close of Wall Street session

- Cloud, AI and ad revenue in focus in Alphabet earnings

- Microsoft cloud revenue expected to slow

- Attention on Foundry business in Intel earnings

Traders will be offered Q1 2024 earnings reports from 3 well-known US tech companies today after close of the Wall Street session. Alphabet (GOOGL.US), Microsoft (MSFT.US) and Intel (INTC.US). Reports from the three could help shape sentiment towards US tech sector. However, traders should keep in mind that markets are unpredictable and an earnings beat does not necessitate a post-earnings share price surge - disappointing earnings from Tesla sent EV manufacturer shares flying, while Meta Platforms is slumping in premarket in spite of reporting better-than-expected results. Let's take a quick look at what market expects from Alphabet, Microsoft and Intel, and what to focus on.

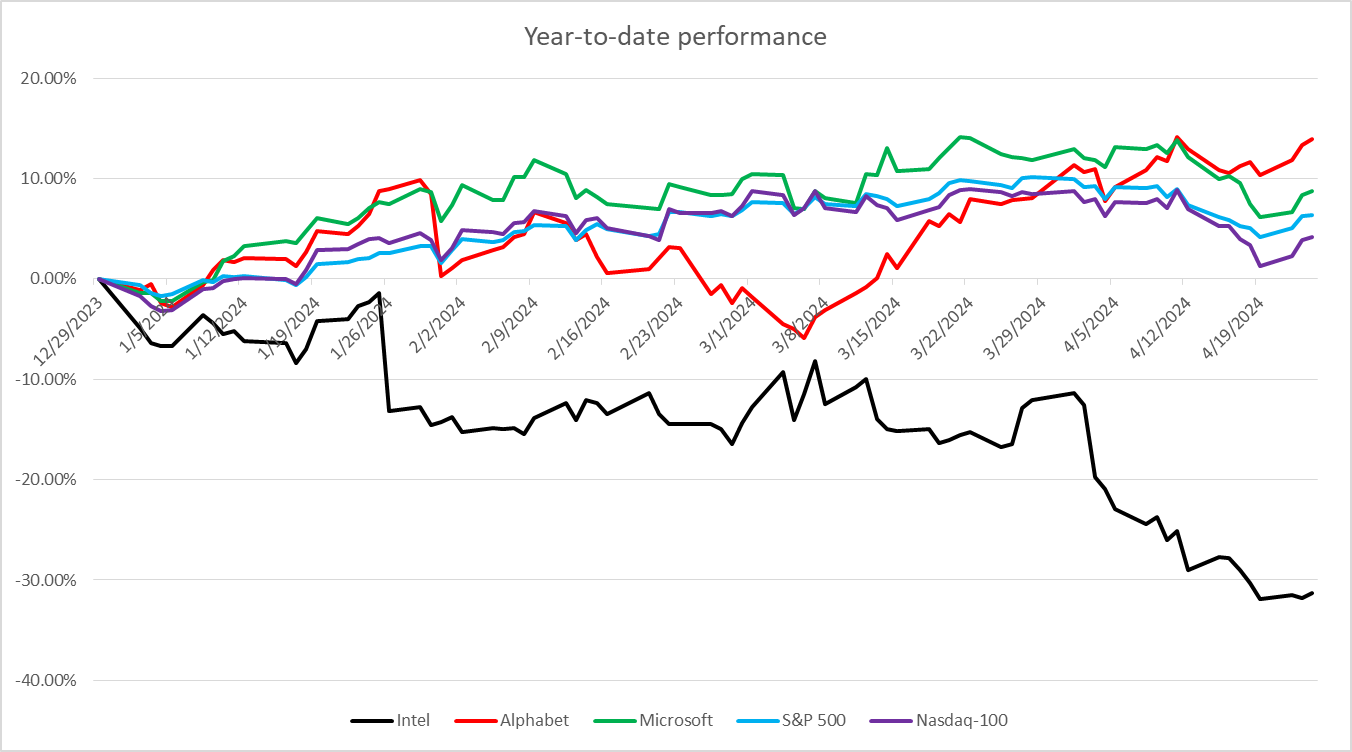

While Alphabet and Microsoft outperformed the broad market so far this year, Intel has been underperforming significantly. Source: Bloomberg Finance LP, XTB Research

While Alphabet and Microsoft outperformed the broad market so far this year, Intel has been underperforming significantly. Source: Bloomberg Finance LP, XTB Research

Out of three large US tech companies reporting earnings today, Microsoft looks the most expensive in terms of forward P/E ratio. Source: Bloomberg Finance LP, XTB

Alphabet

Alphabet (GOOGL.US) has been outperforming S&P 500 and Nasdaq-100 so far this year, gaining almost 14% year-to-date. Attention in Alphabet's report will be mostly on three things - AI, Cloud and advertising. Option markets are implying a 5.7% post-earnings share price move.

Alphabet is expected to report an over-13% YoY growth in total Q1 2024 revenue. Cloud growth is expected to remain strong. While this segment has seen its growth decelerated as it grew in size, analysts' expected year-over-year cloud revenue growth to remain more or less on the same level as in Q4 2023, which was higher than growth recorded in Q3 2024.

Cloud will be watched closely as it is Alphabet's fastest growing segment, but investors will also pay attention to advertising - company's biggest source of revenue. Company is expected to report an over-10% growth in ad revenue, an acceleration from 9.5% reported in Q4 2023. If confirmed, this would mark the fifth consecutive quarter of accelerating ad revenue growth.

Last but not least, any comments on AI will also be watched closely. A dive into AI is helping fuel Google Cloud growth therefore the two will likely be analysed in tandem.

Q1 2024 expectations

- Revenue: $79.04 billion (+13.3% YoY)

- Google Services: $69.06 billion (+11.5% YoY)

- Google Advertising: $60.18 billion (+10.3% YoY)

- Google Cloud: $9.37 billion (+25.8% YoY)

- Other Bets: $372 million (+29.3% YoY)

- Hedging: $96 million (+14.4% YoY)

- Google Services: $69.06 billion (+11.5% YoY)

- Revenue excluding Traffic Acquisition Costs: $66.07 billion (+13.8% YoY)

- Gross profit: $44.72 billion (+14.1% YoY)

- Gross margin: 56.9% vs 56.1% a year ago

- Operating Income: $22.39 billion (+28.6% YoY)

- Google Services: $24.3 billion (+11.8% YoY)

- Google Cloud: $672 million (+252% YoY)

- Other Bets: -$1.12 billion

- Hedging: -$1.65 billion

- Operating Margin: 28.6% vs 25% a year ago

- Net Income: $19.6 billion (+30.2% YoY)

- Net margin: 22.4% vs 21.6% a year ago

- Adjusted EPS: $1.53 vs $1.17 a year ago

- Capital Expenditures: $10.24 billion (+62.8% YoY)

Alphabet (GOOGL.US) remains close to an all-time high. Stock pulled back in the first half of April 2024, but has since managed to recover almost all the losses. Stock is trading a touch below $160 resistance zone, and a strong Q1 earnings report may push the price to new record levels. Source: xStation5

Alphabet (GOOGL.US) remains close to an all-time high. Stock pulled back in the first half of April 2024, but has since managed to recover almost all the losses. Stock is trading a touch below $160 resistance zone, and a strong Q1 earnings report may push the price to new record levels. Source: xStation5

Microsoft

Microsoft (MSFT.US) has been outperforming S&P 500 and Nasdaq-100 so far this year, gaining over 8% year-to-date, following a 90% rally in 2023. When it comes to upcoming earnings report, investors will focus primarily on cloud business, which has been a key growth driver recently. Options markets imply a 4.8% post-earnings share price move.

Microsoft is expected to report an over-15% year-over-year growth in total revenue in fiscal-Q3 2024 (calendar Q1 2024). Cloud is expected to remain the biggest segment in terms of sales and a key driver of growth. Revenue growth in Intelligent Cloud segment is expected to slow to around 19% YoY, from 20.3% YoY in fiscal-Q2 2024 (calendar Q4 2023). However, it is expected to be faster than 15.9% YoY growth recorded in a year ago period. However, a broader cloud revenue category - Commercial Cloud Revenue - is expected to see growth slow below 20% YoY for the first time in history.

AI will be an important theme in the earnings release. More precisely, how it impacts growth in Azure cloud. AI contributed 300 basis points to Azure growth in fiscal-Q1 2024 (calendar Q3 2023) and this contribution increased to 600 basis points in fiscal-Q2 2024 (calendar Q4 2023).

Fiscal-Q3 2024 was also the first full quarter following a consolidation of Activision into Microsoft after an acquisition. It is expected to acquisition help accelerate revenue growth, but at the same time was dilutive to profits.

Fiscal-Q3 2024 expectations

- Revenue: $60.88 billion (+15.2% YoY)

- Productivity & Business Processes: $19.54 billion (+11.6% YoY)

- Intelligent Cloud: $26.25 billion (+18.9% YoY)

- More Personal Computing: $15.07 billion (+13.6% YoY)

- Commercial Cloud Revenue: $33.93 billion (+19% YoY)

- Gross profit: $42.31 billion (+15.2% YoY)

- Gross margin: 69.1% vs 69.5% a year ago

- Operating income: $25.64 billion (+14.7% YoY)

- Productivity & Business Processes: $9.93 billion (+15% YoY)

- Intelligent Cloud: $11.71 billion (+23.6% YoY)

- More Personal Computing: $4.51 billion (+6.6% YoY)

- Operating margin: 43.0% vs 42.3% a year ago

- Net income: $21.06 billion (+15.1% YoY)

- Net margin: 34.0% vs 34.6% a year ago

- Adjusted EPS: $2.83 vs $2.45 a year ago

Microsoft (MSFT.US) reached fresh all-time highs above $430 per share in the second half of March 2024. However, stock has begun to struggle later on and dropped around 8% off the record highs. Declines was halted at the support zone ranging below $400 mark and stock started to recover. Will fiscal-Q3 earnings release provide fuel for a rally to fresh all-time highs? Source: xStation5

Microsoft (MSFT.US) reached fresh all-time highs above $430 per share in the second half of March 2024. However, stock has begun to struggle later on and dropped around 8% off the record highs. Declines was halted at the support zone ranging below $400 mark and stock started to recover. Will fiscal-Q3 earnings release provide fuel for a rally to fresh all-time highs? Source: xStation5

Intel

While Intel (INTC.US) is a smaller company and may not draw as big attention as Alphabet or Microsoft, its report will also be watched closely. After all, it is one of top US semiconductor stocks. Intel has been lagging S&P 500 and Nasdaq-100 significantly so far this year, dropping over 30% year-to-date. Option markets are implying a 7.4% post-earnings share price move.

Intel is expected to report an 8.5% YoY growth in total Q1 revenue, with the largest Client Computing segment expected to see an almost-30% growth and Datacenter & AI segment expected to see an almost 20% revenue drop. However, a lot of attention will be paid to Intel Foundry business. Intel is trying to reshape itself as a global chip foundry company. Foundry business is manufacturing of chips for third parties, just like TSMC does. Intel has received a lot of funds from CHIPS act to expand manufacturing capacity, but there are some hurdles to growth. One of the biggest ones, that differentiates it from TSMC, is the fact that Intel also designs its own chips, and it limits growth potential for its Foundry business. Why? Some companies, like for example AMD, may be unwilling to use Intel's Foundry services as it would require handing Intel, its direct competitor, blueprints to its new designs. However, Intel may attract customers among companies that do not design chips of similar class and use as Intel. Those include, for example, Nvidia and Apple.

As Intel touts Foundry business as next growth driver the outlook for the segment will be watched closely. Nevertheless, one should keep in mind that the segment accounts for less than 2% of Intel's total revenue and its growth has been slowing in the second half of 2023, therefore it will take time before it becomes really meaningful for company.

Q1 2024 expectations

- Revenue: $12.71 billion (+8.5% YoY)

- Client Computing: $7.39 billion (+28.1% YoY)

- Datacenter & AI: $3.45 billion (-19.2% YoY)

- Network & Edge: $1.35 billion (-13.8% YOY)

- Intel Foundry: $170 million (+44% YoY)

- Mobileye: $372 million (-18.8% YoY)

- Gross Profit: $5.70 billion (+24.8% YoY)

- Gross margin: 44.5% vs 38.4%

- Operating income: $562 million (-$294 million a year ago)

- Operating margin: 4.8% vs -2.5% a year ago

- Net income: $580 million (-$169 million a year ago)

- Net margin: 4.5% vs -1.5% a year ago

Intel (INTC.US) has been underperforming significantly this year. Stock kept moving lower, breaking through a number of support zone and has reached the lowest level in half a year. However, sell-off was halted in the second half of April and a positive surprise in Q1 earnings report may help launch an upward correction. Source: xStation5

Intel (INTC.US) has been underperforming significantly this year. Stock kept moving lower, breaking through a number of support zone and has reached the lowest level in half a year. However, sell-off was halted in the second half of April and a positive surprise in Q1 earnings report may help launch an upward correction. Source: xStation5

Daily summary: Weak US data drags markets down, precious metals under pressure again!

Datadog in Top Form: Record Q4 and Strong Outlook for 2026

US Open: Wall Street rises despite weak retail sales

Coca-Cola Earnings: Will the New CEO Withstand the Pressure?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.