-

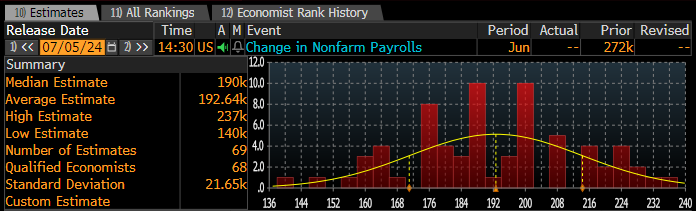

Analysts estimate that nonfarm payroll rose by 192,000 in June versus 272,000 in May

-

Additional indicators in this report, namely unemployment and labor force participation, are expected to show no deviation from May readings

-

The situation may be slightly different in the wage growth category. Hourly wage rates in y/y terms are expected to be +3.9% vs. +4.1% in May

-

US100 is trading in the region of its historic highs ahead of the NFP report

-

The tone of the report may determine whether this barrier will be permanently broken through, or whether we will nevertheless see a pullback in demand on risk-linked instruments

-

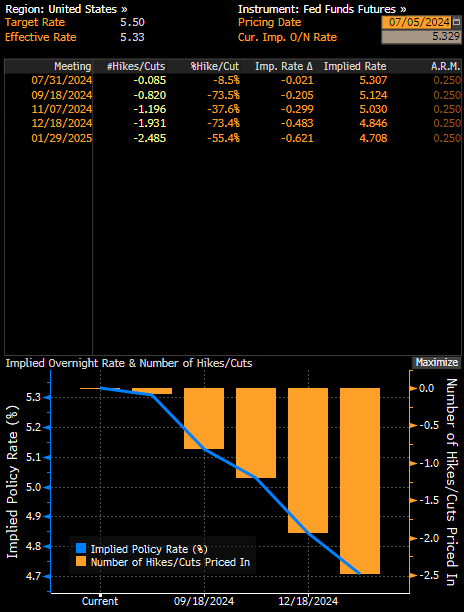

At the moment, swaps estimate that with 82% probability (cumulative value) the Fed will make one rate cut of 25 basis points by September this year

-

It seems that the most favorable scenario for the market would be a below-expected reading, as a very large drop in momentum could put a question mark over the prospect of a soft landing in the U.S. and be perceived as a signal of a 'higher cost' of hawkish Fed policy to the economy

-

Recent data from the U.S. labor market suggest a cooling, although historically it remains quite robust

Ahead of us is this week's key reading, NFP data from the US labor market. It is widely believed that the data for June will show lower job growth, which will confirm to Fed bankers that the time is slowly coming to consider the timing of the first interest rate cut in this tightening cycle. Worse data could theoretically allow for an extended rally in global markets linked to "risk," stock indicess, cryptocurrencies or currencies excluding the dollar. At the moment, swaps estimate that with an 82% probability (cumulative value) the Fed will make one rate cut of 25 basis points by September this year. A worse reading could increase this probability further, which would open a window for a bullish Wall Street reaction. So what to expect from today's data?

The non-farm sector and wages will be key

The June employment report is expected to show 190,000 new jobs, with the unemployment rate likely to remain at 4.0%. Source: Bloomberg Financial LP

Meanwhile, a closely watched measure of wage inflation, average hourly earnings, are expected to rise 3.9% y/y, following May's 4.1% increase. If the data turns out to be lower or equal to Wall Street expectations, it could reinforce the dovish tone of CEO Jerome Powell's comments at the Banking Forum in Sintra last Tuesday. Source: Bloomberg Financial LP

What data is Wall Street 'hoping for'?

Looking deep into the latest data from the U.S. labor market, among others, the ADP report, benefit claims, the Challenger report and JOLTS, we can see that the readings suggest an ongoing, slow cooling. First, benefit claims stabilized at slightly higher levels, in a range between 220,000 and 240,000.

- The ADP report came in stronger than forecast, but the ADP itself signaled that without seasonal industries like tourism and hospitality, private sector employment change would have been decidedly weak.

- A somewhat contradictory light was shed on the situation by June's JOLTS vacancy report, which turned out to be higher than forecasts and higher than previously when the market was expecting a m/m decline. The Challenger report also showed a nearly 50% lower rate of planned layoffs than in May

Remarkably, however, historically, labor market data have not been leading indicators and have typically recorded sharp weakening, already in the midst of an ongoing recession. As a result, the market could perceive a major 'bump' in the data as a signal that it is too late for a 'soft landing,' which does not seem a desirable scenario for equity markets.

- Given the totality of factors, Wall Street may 'like' the mixed situation in the labor market data, as this one still gives hope for a soft landing and faster easing of Fed monetary policy.

- This leads us to conclude that a favorable reading for the indices today would be in line with, or slightly below, forecasts. On the other hand, a stronger NFP would likely be met with a negative reaction from the indices, putting a question mark over the upward reaction to Wednesday's weak ISM PMI data from services.

Fed's implied interest rate path

Fed-funds futures indicate that with an 82% probability (cumulative value), the Fed will make one rate cut of 25 basis points by September this year. The NFP reading is highly likely to change this figure, and it is the upward or downward revision that will be key to the market's reaction to the data presented. Source: Bloomberg Financial LP

Bitcoin (D1 interval)

The crypto market has been in a negative mood since Tuesday. The most popular cryptocurrency has already fallen more than 26% from its historical highs, which classifies it as an instrument in a technical slump. If the declines continue, the most important support point at the moment could be the psychological zone of $50,000. On the other hand, the most important point of resistance seems to be the pierced zone of the 200-day exponential moving average (gold curve on the chart). Source: xStation

US100 (D1 interval)

Nasdaq 100 (US100) futures are climbing to new historic highs. Buying volume has prevailed since the beginning of July; at the same time, the first two weeks of July statistically turned out to be the best two-week period of the year for the US stock market. Source: xStation

US Open: Iran rejects Trump’s peace plan as S&P 500 remains resilient

Market wrap 📈 European indices on the rise despite Iran - US tensions

BREAKING: Nasdaq dips amid Iranian statement cited by the Fars News

No surprises from UK CPI, as hopes rise for peace in the Middle East

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.