November brought a lot of turmoil to the markets. Donald Trump's victory caused a significant movement in financial markets, manifesting the so-called "Trump Trade 2.0." As a result, cryptocurrencies reached record levels (Bitcoin alone rose by over 40% in just one month), American stocks also gained, marking the best month in an already excellent year, with index valuations reaching all-time highs. So, what does the outlook for December's growth look like? Will Santa Claus come this year, or will the market skimp on gifts for investors?

Santa Claus Rally as One of the Most Popular Anomalies

Start investing today or test a free demo

Open account Try demo Download mobile app Download mobile appThe Santa Claus Rally refers to a market anomaly that primarily occurs in the last days of December and the first days of January. This anomaly is characterized by increased growth in stock market indices in the days leading up to Christmas, although pinpointing the exact start of the rally is challenging. Some point to the week before Christmas, while others define the rally as the last five trading sessions in December and the first two days of January. Still, others refer to the general December stock market gains as the Santa Claus Rally.

The heightened euphoria at the end of the year is based on reasons detached from market valuation fundamentals (as with most market anomalies). Increased market optimism is attributed to holiday investor sentiment, reduced fund activity due to year-end closures, leaving more room for individual investors who are generally more optimistic about the market. Other reasons for the rally include the influx of cash from holiday bonuses and investors utilizing limits from investment programs..

How Has the Santa Claus Rally Fared in the 21st Century?

With technological advancements, markets are increasingly quick to price in various information, thereby gradually phasing out traditional anomalies described in textbooks. So, is there still room for such a well-known effect in the 21st century, or is it a relic of past investor imperfections?

We examined the average monthly returns of the American stock market (using the S&P 500 index), the German market (DAX index) and the broad European market (STOXX Europe 600 index)

From the perspective of monthly returns over the past 24 years, December shows relative strength in major indices, although it was not the strongest month in any of these markets. Moreover, the more liquid the market, the greater the tendency to eliminate this anomaly, reflected in smaller differences between the average monthly return and the average return for December.

Comparison of average monthly returns and median returns of the S&P 500, DAX, STOXX Europe 600 indices Source: XTB Research, Bloomberg Finance L.P.

The smallest differences are observed in the S&P 500 index, which on average increased by 0.74% in December. The median for December was 0.98%. Thus, on an average level, the index performs better in December than the average for all months, although the difference in this case is marginal, amounting to only 0.17 percentage points. In the case of the median, December does not perform better, and the American market is the only one among the indices we examined where the median return in December is lower than the median return for all months, with a difference of 0.13 percentage points.

Average returns of the S&P 500 index in different months. Source: XTB Research, Bloomberg Finance L.P.

Slightly more optimistic sentiments in the last month of winter can be observed in European markets. For the DAX index, the average return in December is 1.13%, which is 0.61 percentage points higher than the average for other months. An even larger difference is seen at the median return level, where December outperforms other months by 1.95 percentage points. Thus, among the major markets, investors on the German stock exchange show the greatest tendency to favor December from the perspective of median returns.

Average returns of the DAX index in different months. Source: XTB Research, Bloomberg Finance L.P.

In the broader European market, December does not seem as euphoric, ranking only 5th among the months with positive average returns. Nevertheless, the average return of 0.86% is significantly higher than the monthly average (0.2%), and at the median level, the difference is even more pronounced at 0.96%.

Average returns of the DAX index in different months. Source: XTB Research, Bloomberg Finance L.P.

What About the Classic Rally?

For each of the indices, December performs slightly better compared to other months, but the Santa Claus Rally can also be viewed from a more detailed perspective than just the returns of the last month. The most popular approach points to a period starting 5 trading days before the end of the year and lasting through the first 2 days of January. This is the period we decided to examine to see how the "classic Santa Claus Rally" has fared in the 21st century.

What may be somewhat surprising is that over the past 24 years, the Santa Claus effect has been noticeable in almost every market we studied. Similar to December, it was weakest in the American index, although the difference between the average return during the rally period and the average 2-week return (we used 2 weeks due to the similar number of trading sessions in this period to the length of the rally itself) is higher than in the case of monthly returns. Once again, the median return for the S&P 500 index was lower during the rally period than in the average 2-week period.

Interestingly, for each of the indices, the average return during the rally period was not only higher than the average 2-week return but also higher than the returns in December. This indicates that in European markets, the last days of the year may indeed present stronger growth.

Comparison of average returns and median returns during the Santa Claus Rally period for the S&P 500, DAX, STOXX Europe 600. Source: XTB Research, Bloomberg Finance L.P.

Which sectors should be closely watched?

Investors interested in the Santa Claus Rally phenomenon should pay attention to companies that are particularly dependent on the holiday sentiment. The retail sector stands out in this regard. The holiday season is a time of increased shopping and consumer spending. The period of giving gifts to loved ones, along with many promotions and greater optimism associated with the end of the year, drives consumers to stores, which positively impacts the results of retailers.

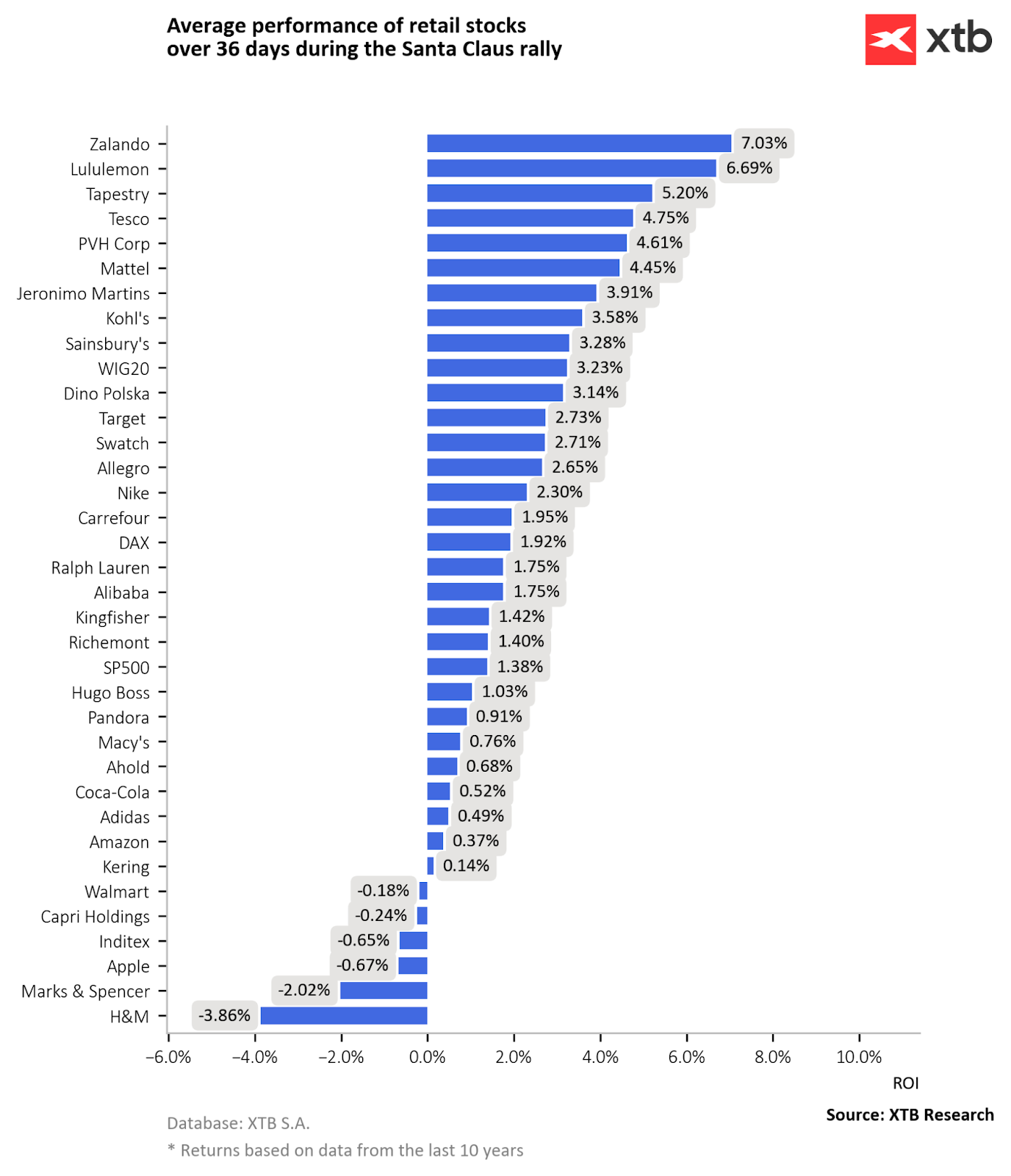

Although the broader American market does not show a strong Santa Claus Rally effect, the last decade indicates elevated growth for retail companies during the last days of December and the first days of January.

Average returns of retail sector companies during the Santa Claus Rally period over the last 10 years. Source: XTB Research

The best-performing company is Europe's Zalando. As one of the leaders in the e-commerce clothing market, it particularly benefits from increased consumer shopping activity. Globally, there is a growing trend of customers using online sales channels. Over the past 10 years, strong performance during the rally period has also been shown by Lululemon, Tapestry, and Tesco.

In terms of the annualized return during the Santa Claus Rally period, these companies show a significantly greater tendency for growth during the December rally compared to other months. This difference is particularly noticeable for Tapestry, Tesco, as well as PVH Corp and Mattel.

What about this year’s rally?

Historical data indicates a tendency for the market to be more optimistic in the last days of the year. However, several obstacles could hinder this year's rally. Firstly, this year is characterized by a significantly stronger concentration of capital in the American market. Investors in 2024 are heavily favoring this market over others, which could result in some capital shifting to the American stocks at the end of the year instead of European markets. Historically, the American market does not exhibit sensitivity to the Santa Claus effect. Additionally, the current levels of both concentration and investor optimism regarding next year's growth are at record highs, which is unprecedented. Such high optimism in the American market has only appeared after significant declines, never after such strong increases.

Another risk to the rally is the strong overrepresentation of stocks in the portfolios of both individual and institutional investors. According to a survey conducted by Bank of America, the number of managers overweighting U.S. stocks in their portfolios is currently at an 11-year high. This could lead to pressure to rebalance portfolios before the end of the year, potentially resulting in selling pressure that could dampen the year-end rally effect.

The final factor investors should consider as the year-end approaches is the stretched valuation, which for American companies is at record high levels. Fundamental indicators based on market price (P/BV, P/S, EV/EBITDA, Market cap/GDP) are around the top 1-3% of historical readings for the American market. Such stretched valuations have only occurred in four instances: before the 1929 crisis, in the mid-1960s, during the dot-com bubble, and in 2021. Each time the S&P 500 reached such values, its return was worse than average.

All of this makes the occurrence of a rally in the American market under these conditions seem unlikely. On the other hand, this creates potential for increased attention to European companies, which could strengthen the already existing rally effect in these markets.

Tymoteusz Turski, Stock market analyst XTB

Bartłomiej Mętrak, Financial market analyst XTB

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.