Some stock market years leave a bitter taste, and for the CAC 40, 2024 was one of them. The French stock market distinctly underperformed compared to global markets, posting a 2% decline while the CSI 300 in China rose by 16%, the MSCI World by 17%, the German DAX by 18.7%, the S&P 500 by 25%, and the Nasdaq 100 by 28.5%. However, a few French companies managed to stand out, such as Safran (SAF.FR), which achieved the second-best performance on the CAC 40 with a 33% increase.

In the French aeronautics sector, three players dominate through their scale: Thales, Airbus, and Safran. Yet Safran (SAF) has particularly distinguished itself, with its share price soaring by nearly 100% since January 2019, outpacing its peers and commercial partners.

A Strategic Player : Safran (SAF)

Safran is an international high-technology group, a leader in the fields of aeronautics, space, and defense. With a market capitalization of €91 billion, it ranks among the largest market caps on the Paris Stock Exchange and is an integral part of the CAC 40. The group was formed in 2005 through the merger of Snecma and Sagem, consolidating its positions in propulsion and aeronautical equipment.

Safran plays a strategic role for the French government, with an 11% stake held by the French state. The remaining shares are freely traded on the markets, with no single significant shareholder holding a majority stake.

Its main clients include Airbus, Boeing, Dassault Aviation, Thales, MBDA, and numerous airlines.

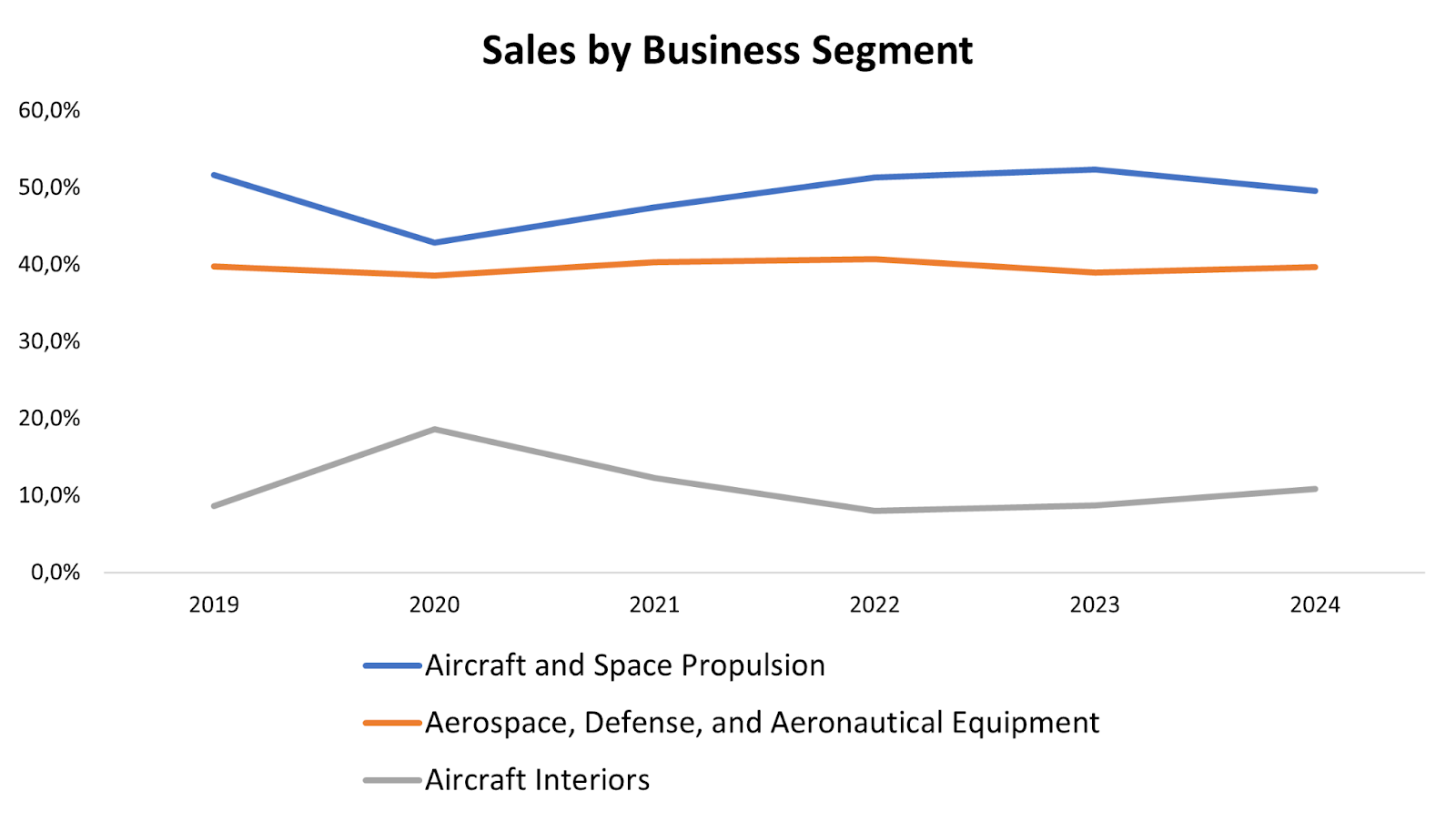

Business Structure and Revenue Breakdown

Safran organizes its activities around three major divisions:

- Aircraft and Space Propulsion (50% of Revenue)

This segment covers the design and production of engines for civil and military aircraft, helicopters, space launchers, and missiles. Safran is notably renowned for the LEAP engine, developed in collaboration with General Electric within the CFM International joint venture, powering aircraft such as the Airbus A320neo and the Boeing 737 MAX.

- Aerospace, Defense, and Aeronautical Equipment (40% of Revenue)

This division encompasses the manufacture of landing gear, avionics systems, airplane seats, as well as optronics and navigation solutions for defense. Safran supplies essential equipment to many aircraft manufacturers and airlines worldwide.

- Aircraft Interiors (10% of Revenue)

This division specializes in the design and production of cabin interiors for aircraft, including seats, in-flight entertainment systems, and connectivity solutions.

Source : XTB Research

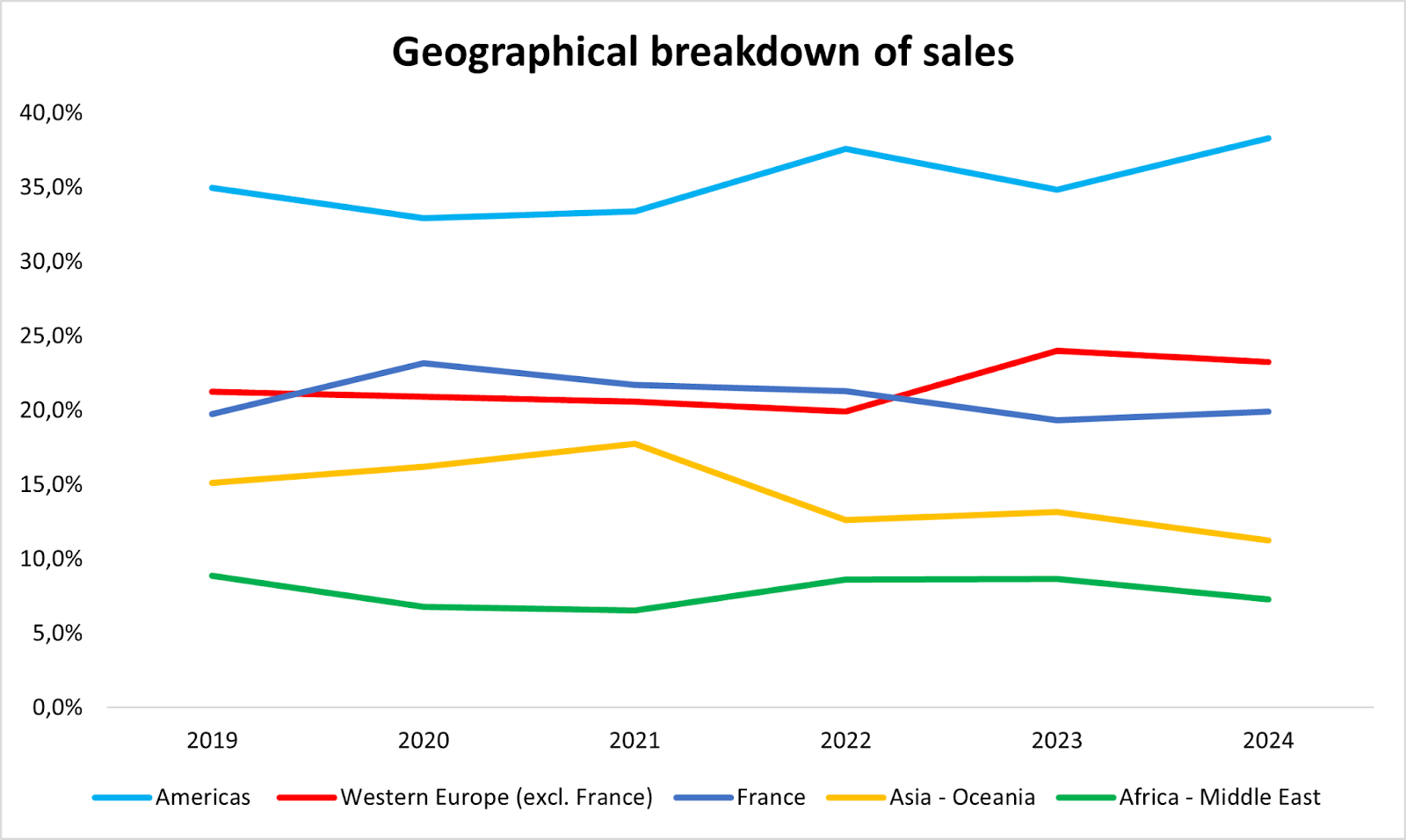

During the first half of 2024, the American and European continents generated 80% of revenue. However, there was a decline in the Asia-Pacific region, due to the Chinese slowdown. This downturn was largely offset by a strong and growing economic momentum on the American continent.

Source : XTB Research

Recurring Revenues: The Strength of Safran’s Economic Model

The appeal of Safran to investors lies in the predictability of its future revenues. Except for the exceptional disruption caused by the COVID-19 crisis in the aircraft industry, analysts’ revenue forecasts typically align very closely with the group’s published results. This visibility stems primarily from Safran’s economic model.

A key driver of Safran’s growth is the LEAP engines, which are often sold with low margins—or even at a loss—upon initial delivery. Profitability is then ensured by after-sales services, including maintenance, repair, and overhaul (MRO). These activities generate recurring revenues over an average lifespan of 25 years, corresponding to the operational life of the engines.

To support this strategy, Safran announced in October 2024 an investment plan exceeding one billion euros to expand its global LEAP engine maintenance network. The group anticipates a 15% to 20% increase in LEAP engine deliveries in 2025 compared to 2024, reflecting consistently robust demand for this flagship product.

Safran: Far Superior to Its Peers

The COVID-19 crisis caused lasting disruptions in the production and supply chain of the aircraft sector. However, these challenges are gradually subsiding, enabling Safran to record the Group's best ever performance in 2024. Expected sales for the past year amount to €27.18 billion, surpassing the €24.6 billion recorded in 2019 and showing a 17% increase compared to 2023. The market anticipates double-digit annual growth in revenue at least through 2026.

Net margins are also rising, reaching 10.5% in 2024 (compared to 10% in 2019), with a target of 11.5% by 2026. By comparison, net margins stand at 5.87% for Airbus and 6.69% for Thales. Furthermore, Safran’s return on equity has improved by 1.5 points, hitting 23.5% in 2024 versus 2019.

Financially, the group’s debt-to-equity ratio is extremely low at 0.37, and all debt is fully covered by available liquidity. This virtually eliminates default risk, making Safran a secure and reassuring investment option for investors.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source : XTB Research

Clouds on the Horizon?

Despite solid fundamentals that could have made Safran the best CAC 40 stock in 2024, the share price fell by more than 7% on December 5, 2024. This drop followed the Investor Day held the previous day, during which the group presented its 2024-2028 Strategic Plan, deemed disappointing by the market.

Safran projects revenue growth of 10% for 2025, below the 14% consensus, and a current operating result estimated between €4.7 billion and €4.8 billion—also under the €4.9 billion consensus. Free cash flow forecasts range from €2.8 to €3 billion, or 11% below expectations, mainly due to increased capital expenditures and the French surtax. Moreover, spare parts revenue will see only modest growth, driven primarily by price increases rather than higher volumes.

Looking ahead to 2028, Safran remains just as cautious, forecasting an average annual revenue growth rate between 7% and 9%, and an annual increase of around 10% for equipment and defense. Although Safran’s management typically adopts conservative forecasts, these figures surprised observers with their restraint, sharply contrasting with market expectations.

The only positive announcement was the launch of a €5 billion share buyback program between 2025 and 2028, in addition to the €750 million planned for 2024.

Quality Comes at a Price, But Too Expensive Is Still Too Expensive

As is often the case on the stock market, a company’s quality is reflected in its price. For Safran, this translates into a price-to-earnings ratio (P/E) of 26.4 for 2025, well above that of Airbus (22) and Thales (17). The EV/Sales and EV/EBITDA ratios are also significantly higher than those of its peers, highlighting how strongly the market values Safran’s robust business model.

It is precisely because the valuation is quite high that even a small hiccup—such as the Investor Day—can severely affect the share price. Although Safran’s fundamentals remain strong, a marked growth slowdown, as projected by management, makes it challenging to justify a purchase at current levels.

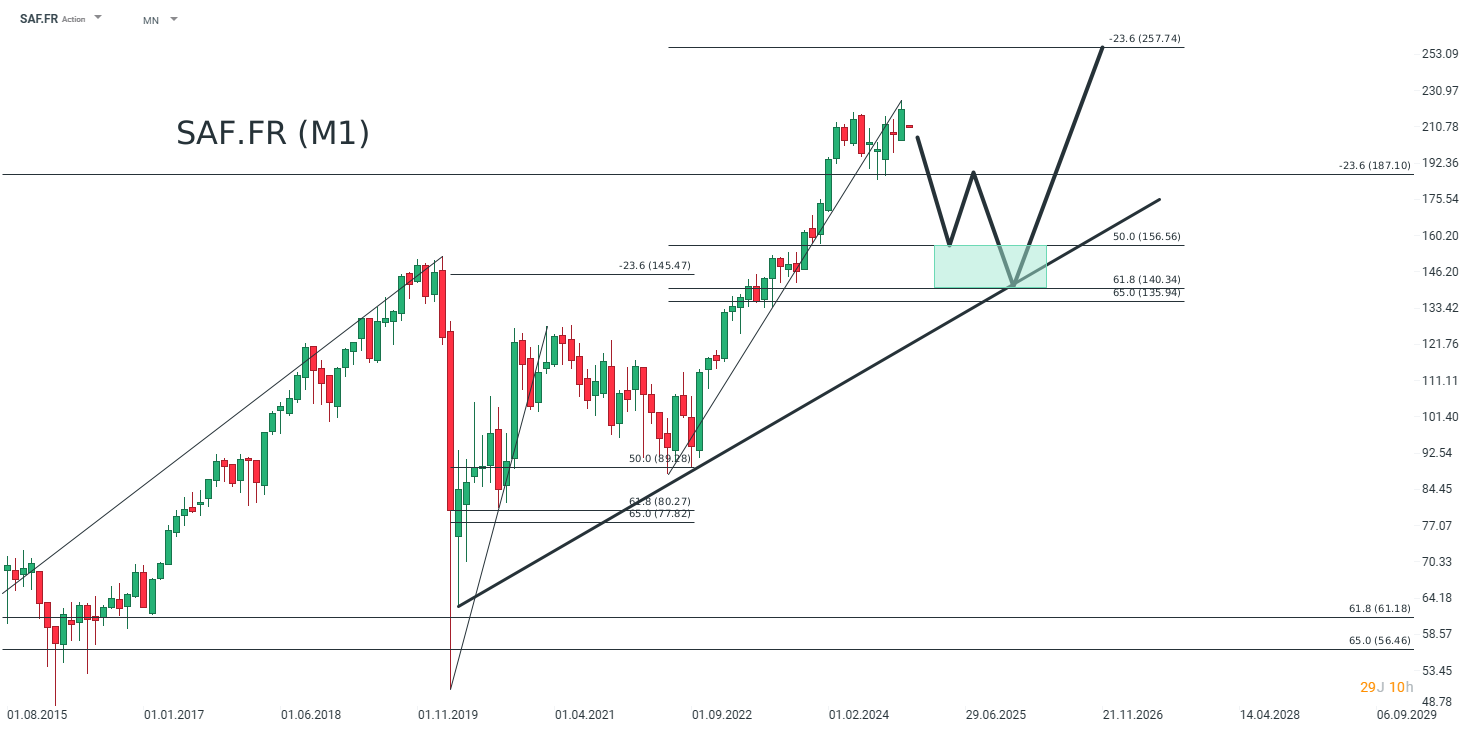

From a long-term investment perspective, it may be wise to wait for a correction before taking a position in Safran. According to technical analysis, investors could consider buying in the zone between €156.56 and €140.34 (green box). This area corresponds to the 50% and 61.8% Fibonacci retracements of a measured upward move (#2). They could then aim for a target of €257 by 2026. However, if this support zone were to break, the share price could retreat to €118.

Source : XTB Research

Matéis Mouflet, XTB France, Markets Analyst

Arista Networks closes 2025 with record results!

AI scare trade broadens out as we wait for key inflation update

Daily summary: Silver plunges 9% 🚨Indices, crypto and precious metals under pressure

Does the current sell-off signal the end of quantum companies?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.