JP Morgan and Citigroup are some of the worst performers on the S&P 500 today, yet both US banks delivered Q2 earnings results that beat forecasts. Citi delivered revenues of $20.13bn, beating estimates of $20.11bn, while net income was $3.03bn, 11% higher than estimates of $2.72bn. JP Morgan’s results were even better. Revenues were $50.99bn, better than the $50.2bn expected, and net income was 8% higher than expected. This was a record profit for JPM; however, its stock price is down more than 2% today.

The question for investors now is whether this sell-off is part of the rotation out of the higher performing stocks towards value investing, or is there something within these results that are unsettling investors? Both JPM and Citi have seen large gains for their share prices this year. JPM’s share price is up more than 19% YTD, while Citi’s share price is higher by nearly a fifth.

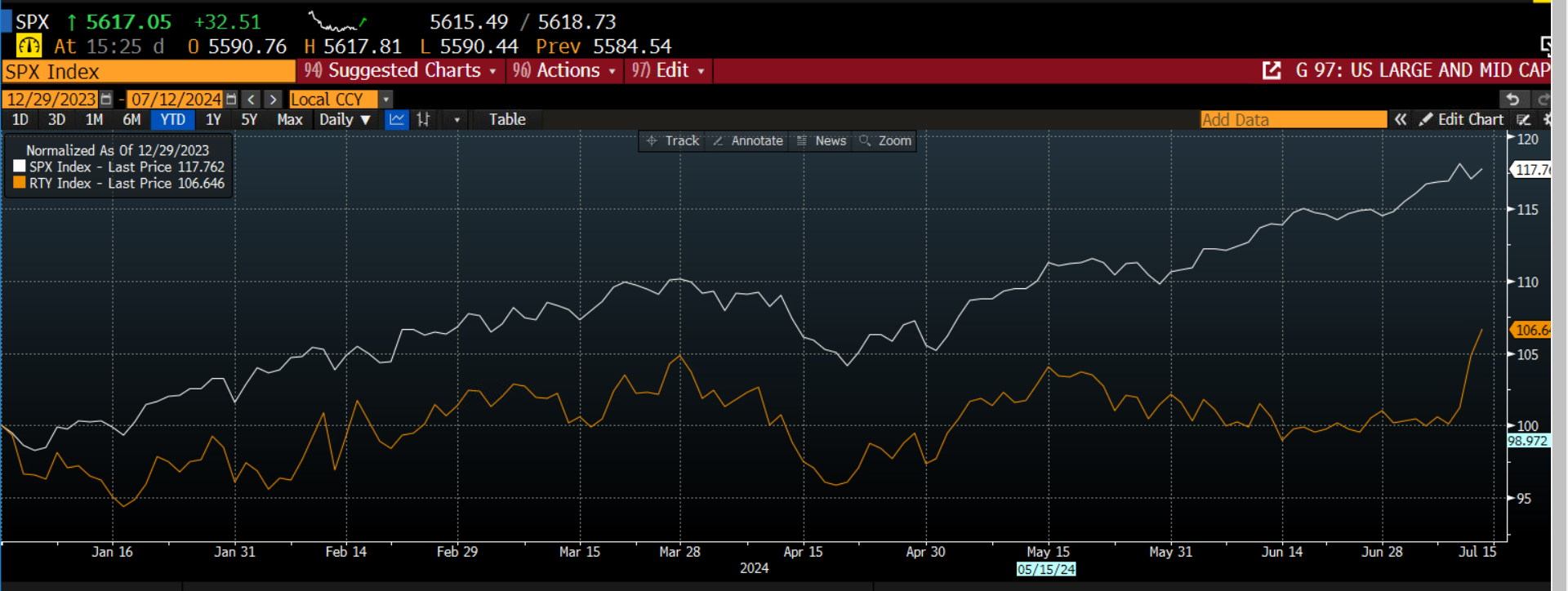

Market breadth improves as the stock market rally broadens out

Interestingly, the sell off in the banks is not part of a broader decline in the market. More than 400 stocks in the US blue chip index are higher on Friday, with only 20% of stocks declining. Market breadth is improving and this is why the Russell 2000, the US mid cap index, has surged this week and is currently at its highest level since early 2022. This suggests that for the second day, the stock market rally is broadening out, at the same time as expectations for interest rate cuts are surging in the US.

The market expects the Fed to cut rates in September, and there is now a 95% probability of a rate cut, even though producer prices were stronger than expected. However, this stage of the monetary policy cycle could be tricky for the banks, which may explain why they are selling off at the end of the week.

Chart 1: S&P 500 and Russell 2000, the mid-caps play catch up

Source: XTB and Bloomberg

Wells Fargo takes the brunt of investor ire

The current stage of the monetary policy cycle is not kind to banks. Wells Fargo’s stock price is down more than 6% on poor YoY earnings, although earnings per share were higher than analyst estimates. However, the big concern for investors was Wells Fargo’s forward guidance about a decline in net interest income. The market is focusing on this, although the bank expects an increase in fee-based income, i.e., investment banking revenues, and it plans to boost its dividend by 14% this year. Is the market over-reacting to the potential for a decline in net interest income? The answer is both yes and no. A shrinking revenue stream is not good news for any business. Added to this, fee-based income can be highly uncertain. Thus, some caution in bank share prices is to be expected, especially since the US banks have had a strong run so far this year.

Why the sell off for bank shares?

Overall, the headline figures for both JPM and Citi were strong, although Citi sounded cautious about costs for 2024 being at the higher end of estimates, added to this, fixed income trading was a touch weaker than expected at $3.56bn vs. $3.61bn expected. Usually, growth in return on average equity of 6.3% vs. 5.6% YoY would be enough to override some of the weaker news, but not in the current environment. Likewise at JP Morgan, although the bank pointed to signs of strong fee-based income as dealmaking makes a comeback, the 4% increase in net interest income last quarter was slightly weaker than estimates and this has hurt sentiment towards the stock. Jamie Dimon, as he usually does during earnings announcements, sounded concerned about geopolitics and he voiced concerns that inflation could make a comeback due to global fiscal deficits and the shifts in global trade. These are valid concerns that the market should take seriously, but we do not think that they are causing bank stocks to decline.

What next for bank share prices?

We believe that the decline in bank share prices after today’s earnings report is part of a bigger shift in market sentiment. As mentioned above, there is good market breadth today, with mid-caps outperforming large caps, for the second consecutive session. Banking shares have seen large price gains this year, now it’s the time for value stocks to shine, which means some mild losses for the big banks, in our view.

Politics batter the UK bond market once more, as Starmer remains under pressure

STM is growing stronger thanks to a new partnership with AWS!

The Week Ahead

Market update: recovery takes hold, but investors remain on edge

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.