LVMH : a buying opportunity despite deteriorating fundamentals

Two weeks ago, French luxury companies found themselves in the crosshairs of investors' appetite as the bell announcing the much-anticipated earnings season rang. Leading the way, the market giant LVMH set the tone by weighing down the entire sector, with its stock price plunging to around €588 per share at the open—a drop of about 6% compared to its previous close.

At the same time, Hermès was swept up in the downward trend, falling by 3%, while L’Oréal emerged as the biggest loser, opening the session with an 8% loss. Although some of these declines have since been recouped, thanks in part to Hermès' results, which were more optimistic than those of its peers, there remains significant tension regarding the outlook for CAC 40 leaders amid a global economic slowdown.

Lower interest rates, stimulus measures by Chinese authorities, and adjustments in the wine and spirits market—what prospects lie ahead for LVMH as it faces vulnerabilities in a segment of the economy once considered recession-proof?

China: A Double-Edged Sword

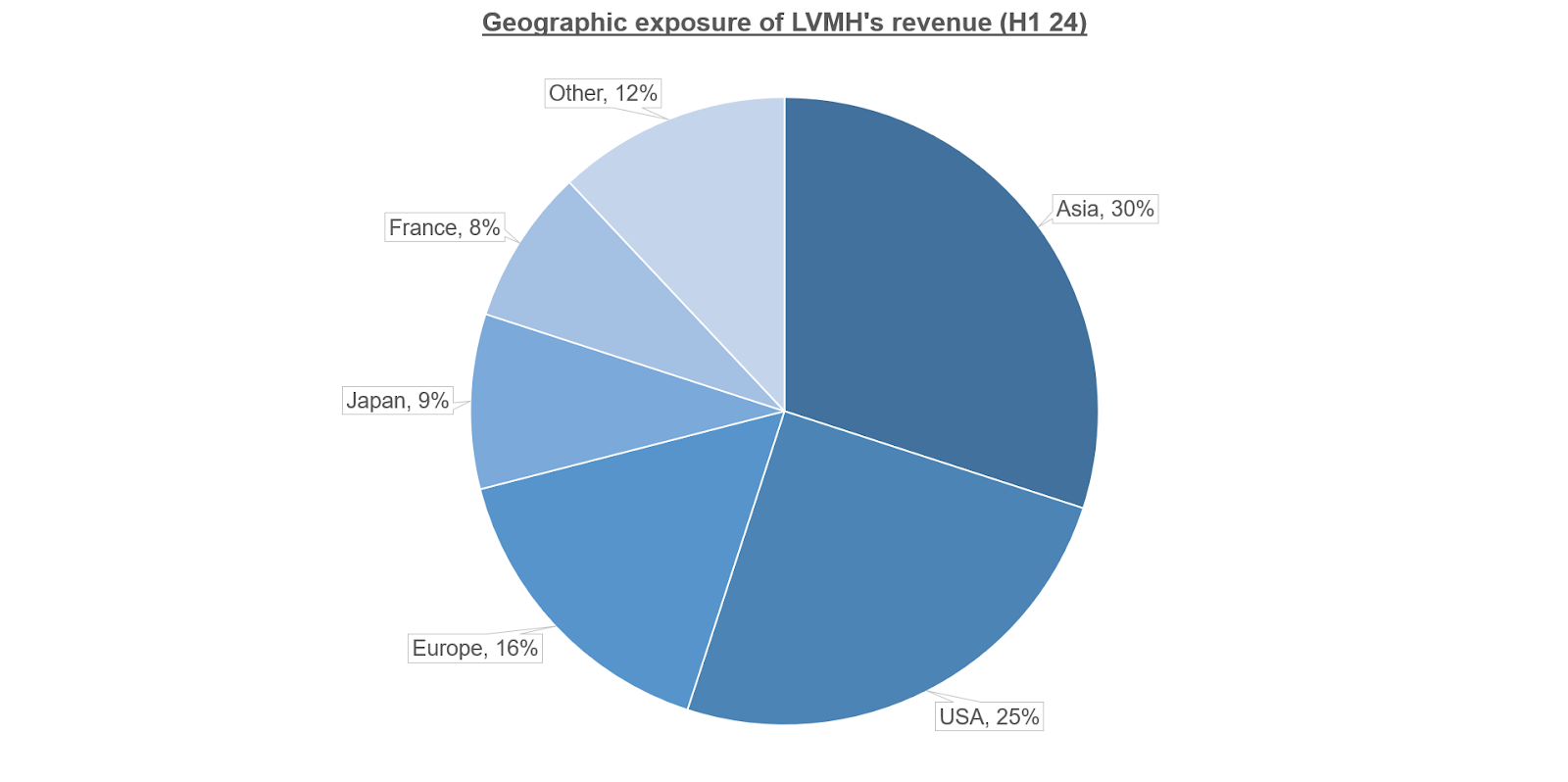

The strategic decision to expand into the Chinese market, starting with the export of Hennessy cognac in 1859 and followed by the opening of the first Louis Vuitton store in 1982, has arguably been one of LVMH's key growth drivers. The Asia-Pacific region rapidly evolved from a negligible portion of its revenue in the 1990s to nearly 17% by 2004. Twenty years later, this figure has grown to almost 30%.

Source : LVMH

Yet, what has been one of the company’s best moves is now also its greatest challenge. With quarterly GDP growth below 1% for both the second and third quarters and year-over-year retail sales growth at two to three times below its ten-year average, China is struggling to reignite its post-COVID economy. The People’s Bank of China (PBOC) has decided to intervene, perhaps spurred by concerns over lagging behind monetary easing already undertaken by the U.S. and European counterparts. In late September, it unveiled a series of measures aimed at sparking growth, including reducing commercial banks' reserve requirements and enhancing access to capital.

However, after an initially strong reaction, markets have tempered their expectations, critically assessing the adequacy of these measures. After all, can liquidity keep flowing into an economy with debt levels nearing 84% of its GDP?

Source : National Bureau of Statistics of China

In the U.S., the concerns are somewhat less pressing, with GDP growth for the second quarter around 3%, above its ten-year average, and investors increasingly confident for a “no landing” scenario—avoiding a recession through timely rate cuts. This is welcomed amid a still-fragile job market, yet rising five-year breakeven inflation rates and bond yields suggest that the Federal Reserve’s maneuvering room may be tighter than anticipated.

On the European side, consumption is decidedly sluggish. Despite wage growth outpacing inflation in the first two quarters of 2024, much of the surplus income seems to have been channeled into savings, reaching a historical rate of around 15.5%. A return to consumer spending may emerge once monetary conditions hit their lowest, although this isn’t expected before at least September 2025.

Disappointing Third-Quarter Sales

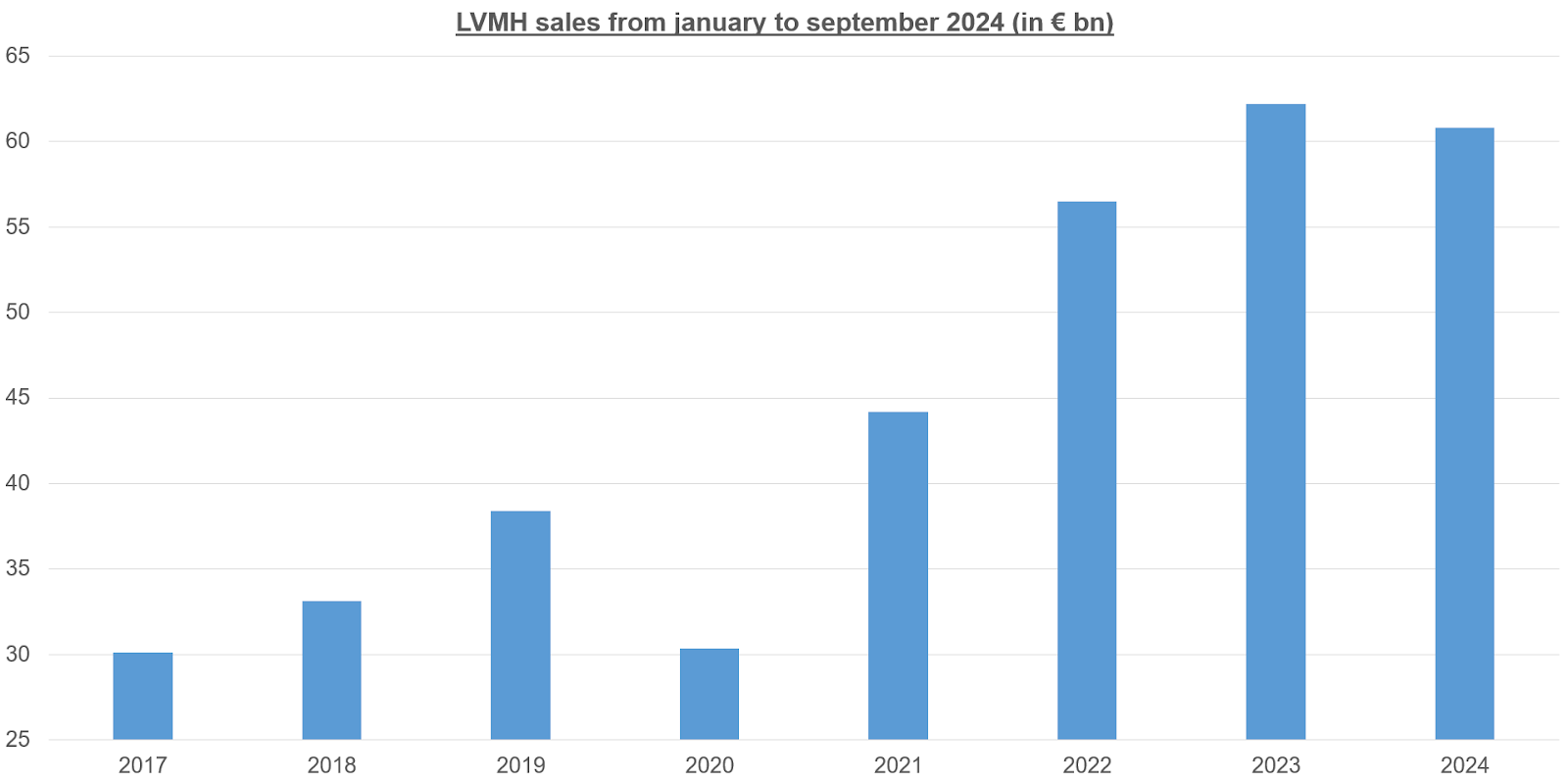

LVMH’s recently released quarterly results offer only partial insights, as they only include revenue for this period. Nonetheless, the numbers reflect the previously discussed economic trends, revealing that LVMH has borne the brunt of the slowdown. With revenue estimated at €19.08 billion—a 4.44% decrease from the third quarter of 2023—the group is experiencing its first decline in nine-month performance since the COVID crisis in 2020.

Source : LVMH

The “Fashion & Leather Goods” division is mainly to blame, representing nearly half of the sales, with a 5% drop in revenue. The “Watches & Jewelry” and “Wines & Spirits” segments also underperformed, accounting for 12.8% and 7.5% of the group's sales, respectively. Meanwhile, the “Selective Retailing” and “Perfumes & Cosmetics” sectors performed slightly better, with growth rates of around 2-3%.

Assuming sales stabilize in the fourth quarter and the net profit margin for the semester (17.44%) remains steady, LVMH could report earnings of approximately €14.7 billion next year, down from €15.17 billion in 2023.

Uneven Economic Impact in the Luxury Sector

Currently, almost all French luxury companies have published their quarterly sales, allowing for a peer comparison based on revenue.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source : XTB Research

This comparison highlights disparities among these companies, demonstrating that not all are equally affected by economic fluctuations. LVMH ranks as the third worst performer in terms of market share acquisition, partly due to its high sales volume, which brings it closer to a critical size. Additionally, the brands in its portfolio seem less resilient to the economic slowdown due to a heavier reliance on a client base with moderate incomes.

An Appetite for Risk that Led to Consolidation

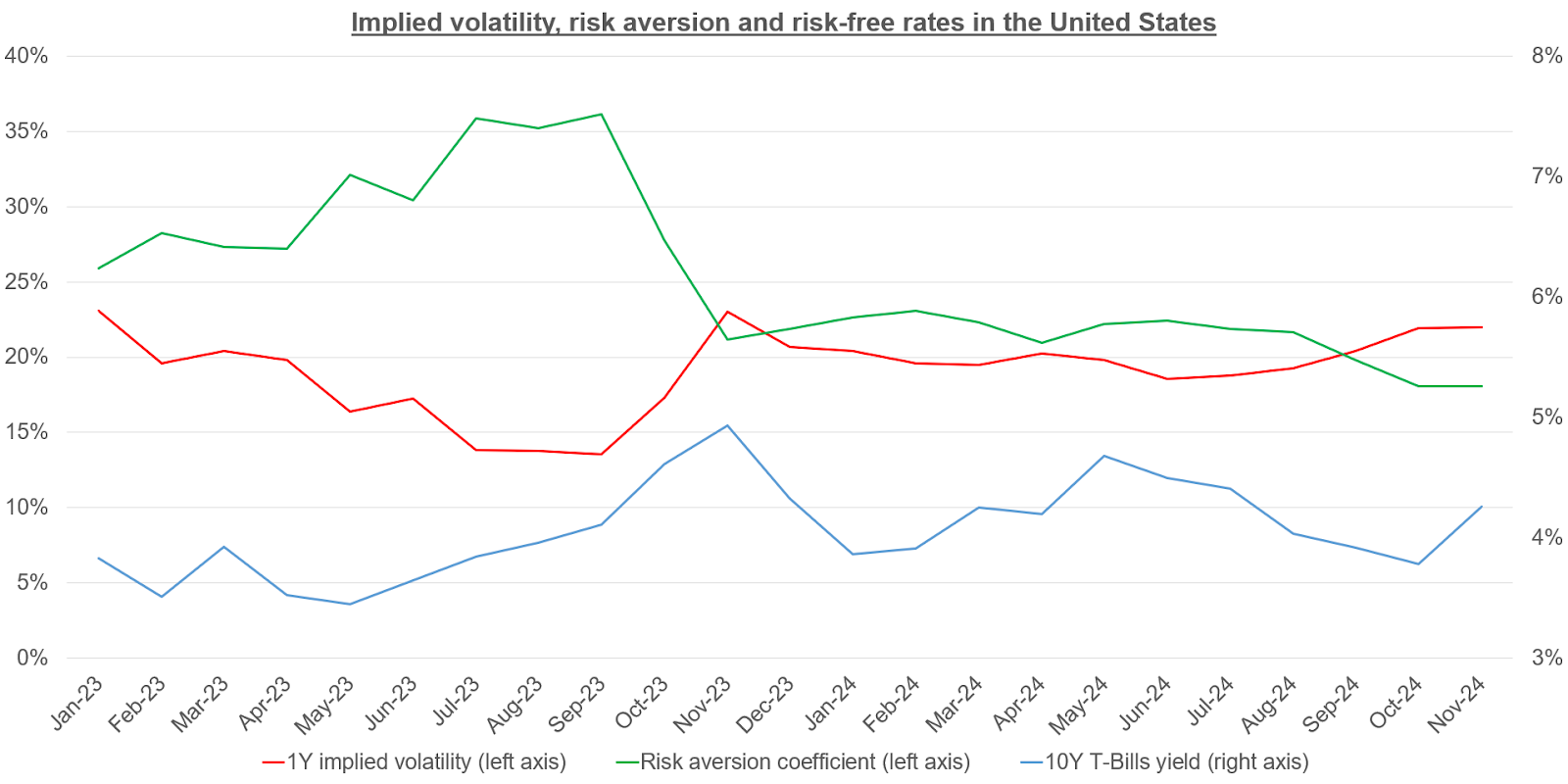

Since its all-time high of nearly €905 in April 2023, LVMH’s stock has undergone a significant correction, currently hovering around €630. An initial consolidation and encouraging results had prompted a strong rebound, but a renewed decline began in March 2024, just as U.S. indices were booming.

Source : XTB Research

These trends indicate that LVMH’s downward trajectory unfolded in two phases. The first phase resulted from a growing risk aversion among investors in 2023, peaking in October, when the stock experienced its first consolidation. By March 2024, however, the continued decline was not driven by increased risk aversion or expected volatility, as both variables had stagnated. LVMH’s underperformance relative to the S&P 500 is likely explained by its strong exposure to the Chinese economy.

Interestingly, the risk aversion and volatility curves crossed in August/September, aligning with the current phase of consolidation. This suggests that anticipated market risk is higher, but investors are more willing to embrace it for the potential of higher returns. Options pricing further underscore that LVMH's risk premium is approximately 70% higher than that of the S&P 500.

Source : XTB Research

With French government bonds yielding 3.017% and a risk aversion coefficient around 18.07%, short-term investors should expect a return of around 9% to invest in LVMH stock, while long-term investors hold a target of 7.7%.

Long-Term Growth Fully Priced In

Recent growth forecasts from the IMF provide additional insights into the market’s long-term expectations. These projections have been revised upward for Asia, Europe, and Japan. However, it is essential to adjust this real growth rate by factoring in expected inflation over the next decade and weighting these projections based on LVMH's respective activity exposure in each region.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source : IMF

Thus, LVMH’s anticipated long-term earnings growth is estimated at 4.523%. Incorporating the short-term risk premium into the Gordon growth model (which assumes the growth rate is the difference between the risk premium and the return rate), and with a trailing twelve-month net yield of approximately 4.48%, the market seems to have fully integrated this rate into the current stock price, and is now looking to price shorter-term results as new data becomes available.

Potential Entry Signals for LVMH Stock

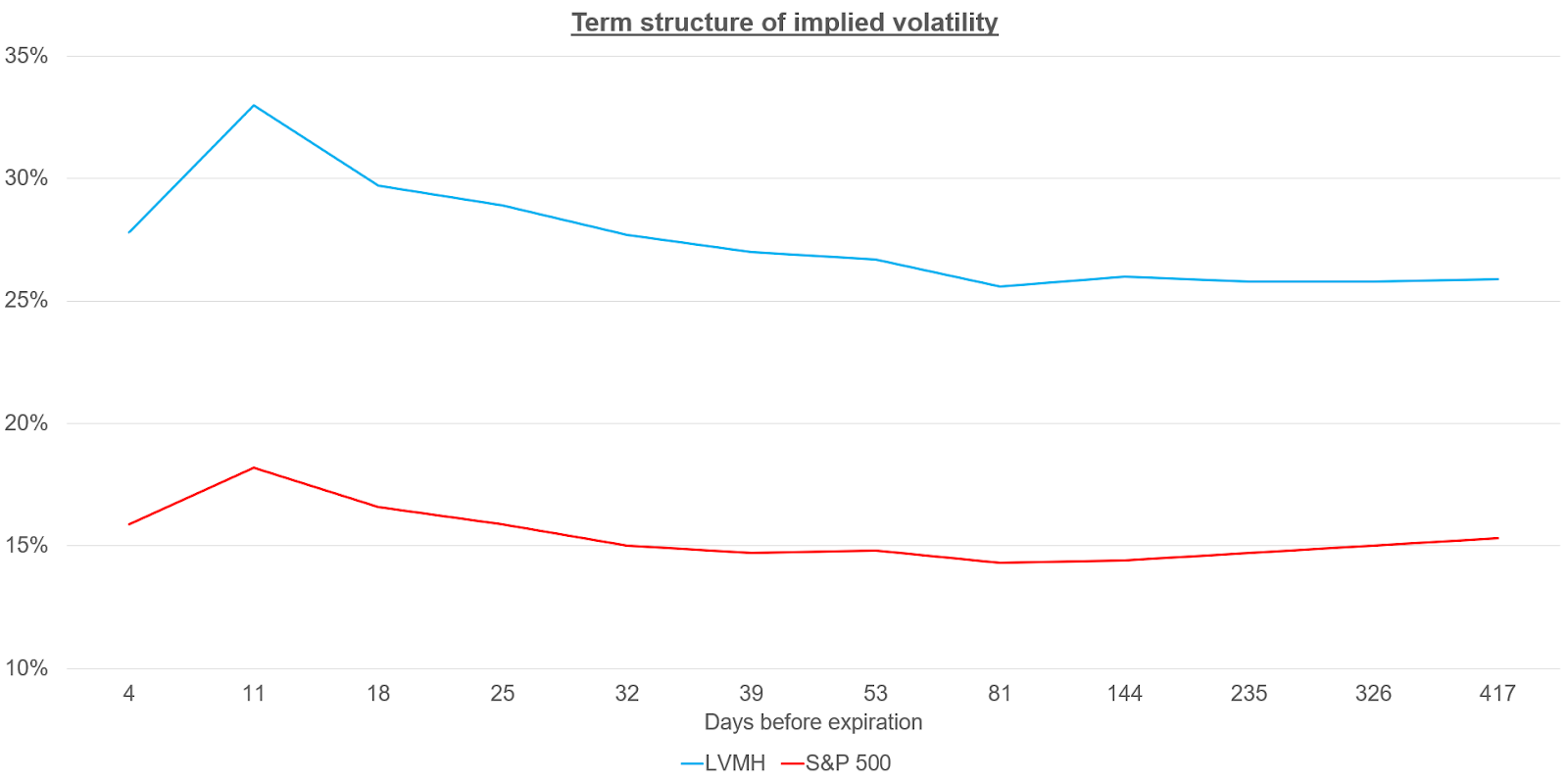

LVMH’s current price is influenced by the prevailing level of expected market volatility and rising bond yields, driven by concerns over a potential return of inflation. However, with falling interest rates and increased coverage by fund managers in the thick of earnings season, operators may soon revert to more flexible valuation assumptions, incorporating a longer-term expected volatility of 26%. In such a scenario, and assuming steady bond yields (around 3%), risk aversion (18.07%), and growth expectations (4.523%), the stock could reach its historical highs above €900.

On a technical note, the price is currently below the fifty-two-week moving average adjusted by one standard deviation, a level generally favored by operators as a statistical undervaluation and entry signal in the long-term trend. The RSI has found support around 30% and showed an upward impulse, while the stock price continued to depreciate simultaneously. This suggests that the current price might represent a potential entry opportunity before a gradual revaluation of the stock’s associated volatility.

Source : xStation5

Maxime Raturat, XTB Research France

Daily summary: Weak US data drags markets down, precious metals under pressure again!

Datadog in Top Form: Record Q4 and Strong Outlook for 2026

US Open: Wall Street rises despite weak retail sales

Coca-Cola Earnings: Will the New CEO Withstand the Pressure?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.