Bond yields are higher across the curve on Tuesday, however, there is a notable shift out of long-term bonds. There has been heavy selling pressure in 30-year bonds, with the UK 30-year yield rising to its highest level since 1998 and is above 5%, after climbing by 10 basis points so far this year. US long term yields have also been climbing, and the 30-year yield is above 4.85% and is at its highest level since October 2023.

What is interesting about this move, is that the market is selling long term bonds at the same time as the market expects the Federal Reserve to cut rates by 56bps in the coming year, along with 64bps of cuts currently priced in for the Bank of England. There are three considerations when it comes to the weakness in the bond market: 1, the yield curves in the UK and the US are normalizing and steepening, after a long period of inversion, which is the sign of a healthy bond market. 2, The UK and US bond markets are moving together. 3, will there be a tipping point, where rising long-term yields cause issues for the wider financial system?

European yields suggest budget deficits matter

European yields can give us some clues about what investors are thinking about long term debt. The chart below shows UK, US, French, German and Spanish 30-year yields, which have been normalized to show how they move together over the last 6 months. As you can see, all yields have picked up since the start of December, however, yields in France, the UK and the US have been moving at a faster pace than German and Spanish yields. This is significant since the UK, the US and France have far higher budget deficits than Germany and Spain, which could be why long-term bonds are selling off. Investors may be using the bond market to express displeasure at the high levels of government debt. This could force a rethink from governments and ultimately a scaling back of public spending or tax increases that could hinder growth.

Chart 1: 30-year bond yields

Source: XTB and Bloomberg

Bond vigilantes are watching from the sidelines

We are not at worrying levels for 30-year yields yet, instead, this is a sign that budget deficits could be a trigger point for financial markets in 2025. The risk is that public finance data in the coming months will be scrutinized by investors and if they don’t like what they see then it may trigger a bond market sell off. Bond vigilantes are not stalking the market yet, but they are watching from the sidelines.

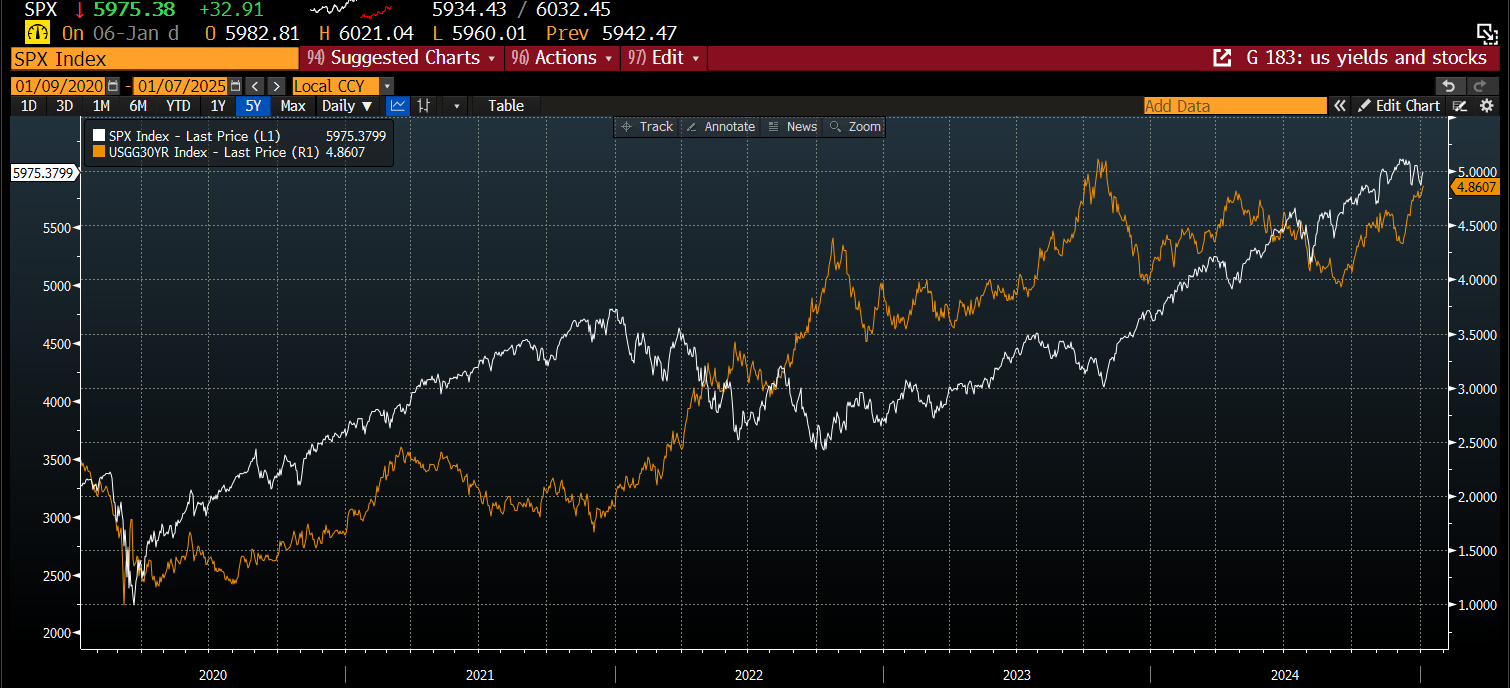

Today and tomorrow’s debt auctions in the US are also worth watching closely, in case there are signs of a buyer’s strike. There is also a risk that rapidly rising bond yields could knock equities, and this is seen as one of the key risks for the stock market this year. As you can see below, US stocks and the 30-year Treasury bond yield tends to move in the same direction, however, with bond yields at multi year highs, stocks and bond yields could be at an inflexion point. The question now is, will US stocks start to struggle if yields continue to move higher.

Chart 2: S&P 500 and the 30-year US bond yield

Source: XTB and Bloomberg

If yields continue to move higher, then central banks could ease pressure on long term yields. We doubt that they will want to speed up the pace of rate cuts, particularly in the UK and the US where inflation pressures remain. However, they could slow down the pace of quantitative tightening if yields continue their rapid ascent.

NFP preview

Economic calendar: NFP data and US oil inventory report 💡

Daily summary: Weak US data drags markets down, precious metals under pressure again!

Datadog in Top Form: Record Q4 and Strong Outlook for 2026

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.