Analysis of Hermès: The Undisputed Master of Luxury

The accommodative announcements by the People's Bank of China (PBOC) and the Chinese government initially provided significant benefits to the French luxury sector, only to be tempered by the reality of corporate performance. Indeed, LVMH and Kering weighed down the entire sector by reporting results far below their standards of recent years. LVMH’s revenue declined by 3% in the third quarter, impacted by China, while Kering delivered an even more disappointing performance, with a 16% drop in revenue, including a 25% decline for its flagship brand Gucci. Moncler was not immune to the trend, recording a 3% decrease in revenue. Yet, amidst this torrent of bad news, one company continues to stand resilient: Hermès.

Hermès: Nearly Two Centuries of Excellence

Founded in 1837 as a luxury equestrian goods manufacturer, Hermès has since diversified its portfolio to include handbags, apparel, and fragrances. The brand is renowned for the exceptional quality of its products, designed to last and often produced in limited quantities, enhancing their exclusivity.

As the fourth-largest French luxury group by revenue, trailing LVMH, Chanel, and Kering, Hermès generated €13.43 billion in sales and a profit of €4.31 billion in 2023. Valued at approximately €210 billion on the Paris Stock Exchange, the group is 66.6% family-owned, with the Hermès family also holding 75.9% of voting rights. The Arnault family owns 1.87% of shares, and no institutional investor holds more than 1.5%. This governance structure makes the leading family virtually unassailable, especially since Hermès is not a standard joint-stock company but a limited partnership with shares, granting the CEO veto power over any decision that could alter its statutes.

Despite this, investors rarely push for change, as Hermès’ leadership has consistently created value for shareholders. Its stock price has risen over 700% in ten years and by 180% since pre-COVID levels.

Beyond Luxury: Hermès and Ultra-Luxury

Hermès sets itself apart with its unique positioning in the ultra-luxury segment, surpassing traditional luxury offerings from houses like LVMH, Chanel, or Gucci. Hermès products—more expensive, rarer, and sometimes exclusive to specific boutiques—justify their prices through the unique story attached to each item, shared with every customer. Each of the brand's 294 stores carefully curates its collection to suit the local clientele, allowing a Chinese customer to purchase a unique item in Shanghai and discover another, unavailable at home, during a visit to Paris.

This philosophy explains why Hermès refuses to acquire competitors, unlike LVMH or Kering, preferring to preserve its exclusivity and prestige. It also justifies the company’s refusal to split its shares to make them more accessible to smaller investors. At nearly €2,000 per share, Hermès’ stock is as much a luxury product as its iconic Birkin bags.

This strategy creates an unparalleled aura for Hermès, enabling it to raise prices without affecting sales—a pricing power unmatched in the sector. Remarkably, higher prices often lead to increased sales.

Exceptional Results

Hermès’ growth, sustained despite price increases, is the strongest in the sector, with a 47.4% revenue increase between 2021 and 2023. By comparison, LVMH grew by 34.1%, Chanel by 25.9%, and Kering by 10.9% over the same period. In the first half of 2024, Hermès achieved 15% growth, far outperforming LVMH (-1%) and Kering (-11%). This growth was partly fueled by the doubling of Chinese millionaires between 2010 and 2022.

Strong growth is not enough on its own—a solid balance sheet is essential for navigating economic uncertainties. On this front, Hermès outshines its competitors. Not only is its balance sheet the strongest in the sector, but it is also the most robust in the CAC 40 and possibly across the Paris Stock Exchange. Hermès’ debt-to-equity ratio is just 13%, compared to 64% for LVMH and 113% for Kering. Even more impressively, Hermès holds twice as much cash as debt, virtually eliminating bankruptcy risk—unlike Kering.

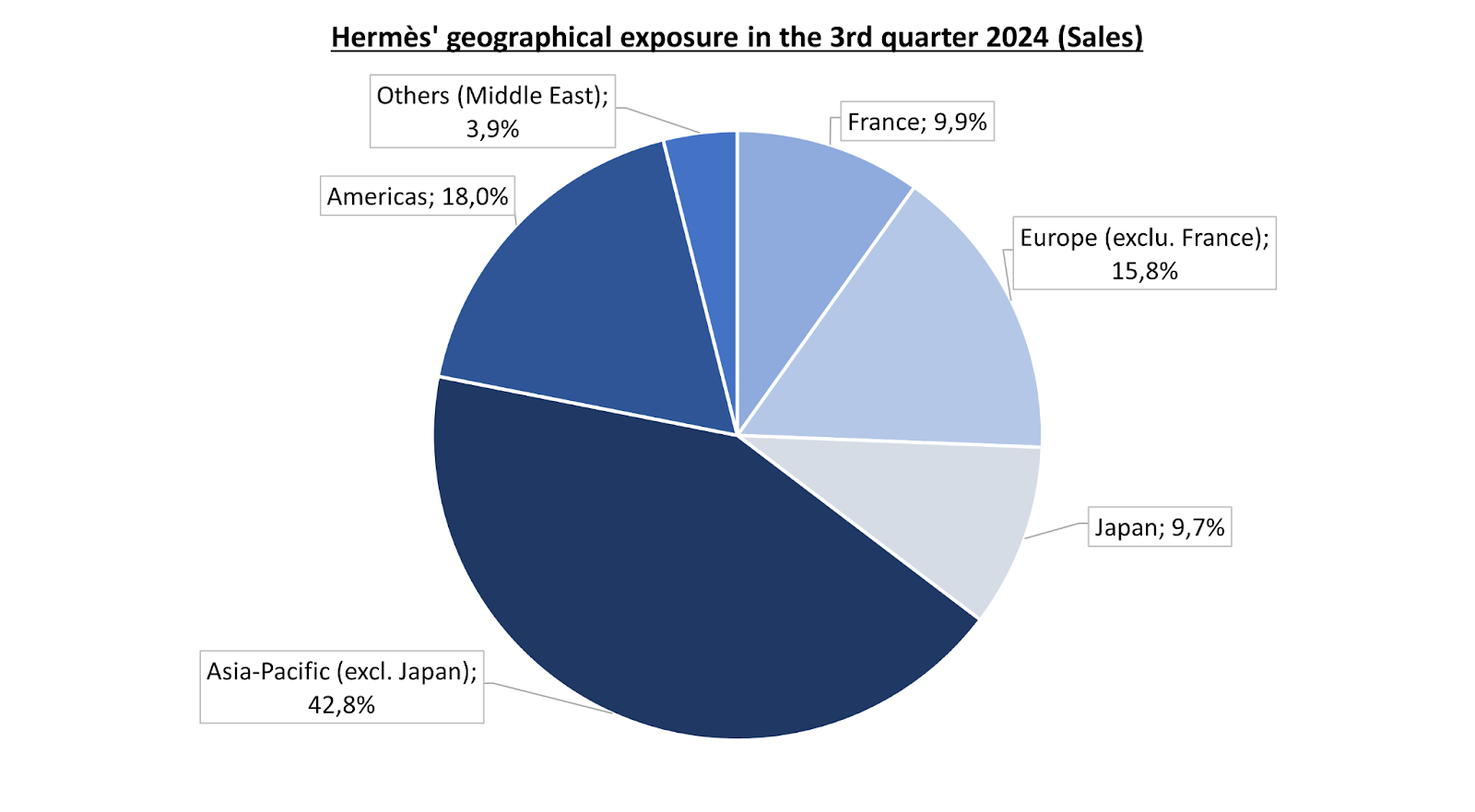

China: A Double-Edged Sword

However, Hermès faces a notable vulnerability: its heavy reliance on the Chinese market. While 31% of LVMH's and 35% of Kering's revenues come from the Asia-Pacific region, this figure rises to 43% for Hermès, with much of it stemming from China. This high exposure contributed to the sector's slowdown in 2023 and the first half of 2024. Asian revenues for LVMH declined by 13%, and those of Kering fell by 20% in H1 2024. This slowdown is attributed to China’s economic contraction since 2023, rising youth unemployment, and the onset of demographic decline.

Nevertheless, Hermès’ revenue grew by 11% in the third quarter, including a 4.6% increase in the Asia-Pacific region. This performance is attributed to Hermès’ clientele, which is the wealthiest. As such, they are less sensitive to economic cycles compared to the upper-middle-class focus of its competitors. This advantage proves crucial during economic slowdowns, but it could limit growth potential when the economy accelerates, as is currently the case with the extensive stimulus measures announced by the Chinese government and the People’s Bank of China (PBOC).

These measures include a 0.10% reduction in the interest rates at which commercial banks borrow from the central bank and a 0.50% cut to the reserve requirement ratio (RRR) for banks, freeing up over $100 billion for new loans. Additionally, the PBOC has indicated it may reduce the RRR further later this year. Simultaneously, the Chinese government has unveiled further stimulus initiatives, including the recapitalization of major state-owned banks with $142 billion, bolstering their capacity to support the domestic economy.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source : XTB Research

Hermès Stock: What is Rare is Valuable

Hermès (RMS) is undeniably a stock of exceptional quality. Its revenue growth, impressive margins, and solid balance sheet make it highly coveted by investors. The low liquidity of the stock, due to its high price and the limited 31.85% of shares available on the market, further enhances its status as an elite investment. These factors contribute to a high valuation: Hermès’ price-to-earnings ratio (P/E) stands at 49, compared to 23 for LVMH and 19 for Kering. Meanwhile, its dividend yield is 0.79%, lower than 1.99% for LVMH and 3.27% for Kering.

Hermès’ valuation significantly exceeds that of its competitors, justified by the brand's excellence. While this valuation premium may have seemed difficult to sustain a few weeks ago due to Hermès' high exposure to a slowing Chinese market, the recent economic stimulus measures and the resilience of its business model could serve as fundamental catalysts for the stock’s performance.

Technically, RMS has been trading within a bullish channel since March 2022. Recently, the stock broke its horizontal support at €2,000, which could lead to a decline toward the lower boundary of the green box at €1,500. Such a drop would represent a major buying opportunity, with a target retracement at the -23.6% Fibonacci level of €2,785 by the end of 2025 (red path).

Conversely, if RMS manages to quickly reclaim the €2,000 support level, potentially boosted by new announcements of Chinese economic stimulus, the stock could rebound and reach €2,340 (green path).

Matéis Mouflet, XTB France Markets Analyst

Daily summary: Weak US data drags markets down, precious metals under pressure again!

Datadog in Top Form: Record Q4 and Strong Outlook for 2026

US Open: Wall Street rises despite weak retail sales

Coca-Cola Earnings: Will the New CEO Withstand the Pressure?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.