GBP: The star of the FX show

The pound has been a big winner this week and is now less than 75 points away from $1.30, a key psychological level. The pound has been one of the best performers since the start of this year, however, the gains have been turbo charged this month, and GBP/USD has gained 1.22% since the UK election on 4th July, and EUR/GBP has dropped nearly 0.6%.

There are multiple drivers of the stronger pound right now, and these factors may continue to keep upward pressure on the pound in the medium term.

Start investing today or test a free demo

Open account Try demo Download mobile app Download mobile app1, Interest rate differentials:

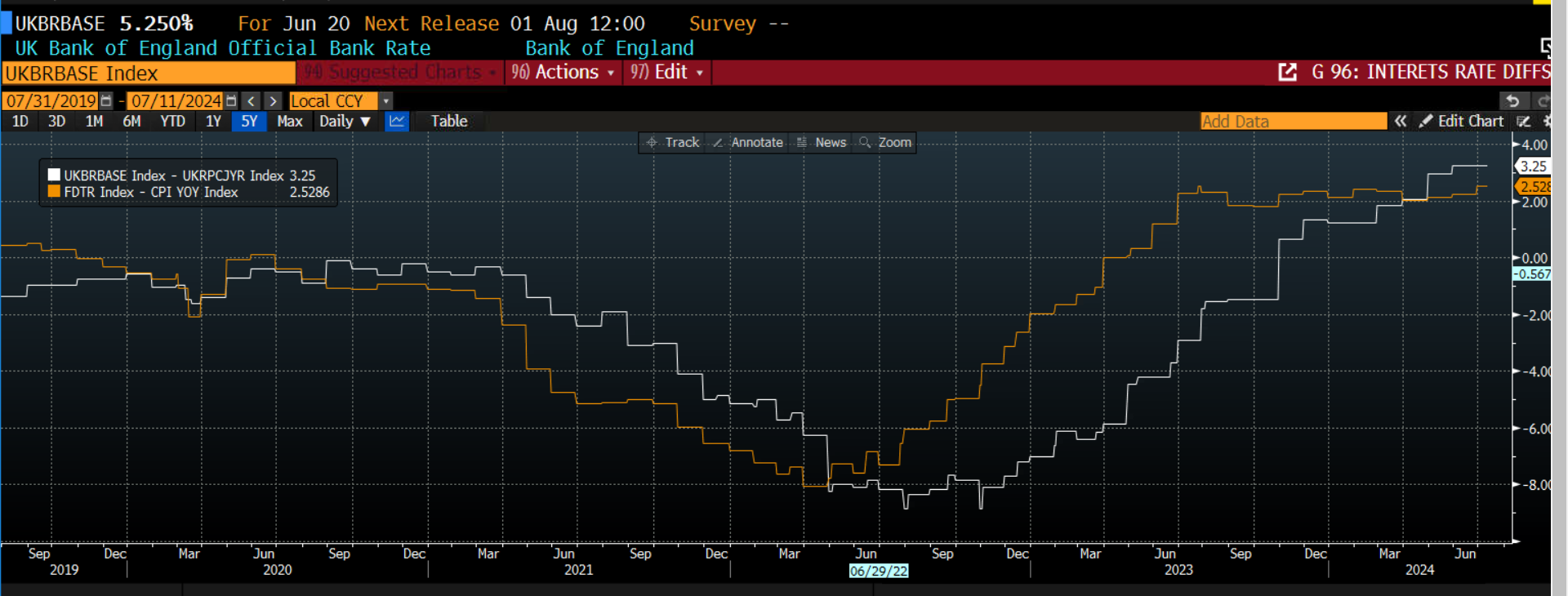

Interest rate differentials are a key fundamental driver of currencies, and right now they are supportive of the pound. The real interest rate in the UK is 3.25%, this compares with 2.5% for the US. The larger real interest rate in the UK vs. the US is driving the GBP/USD right now, and it may only get larger. There is now a 90% chance of a Fed rate cut in September, and the market is currently expecting more than 2 rate cuts from the US Fed this year. This compares with a 57% chance of a rate cut from the BOE in August, and less than 2 rate cuts priced in for the UK this year.

Chart: UK and US real interest rates, the pound is benefitting from a larger real yield differential than the USD right now.

Source: XTB and Bloomberg

2, Growth and inflation forecast

The UK’s growth outlook has improved in recent weeks. After flat monthly GDP growth in April, the May rate of GDP growth was 0.4%, defying expectations of a 0.2% increase. The Bank of England predicted a 0.2% rate of growth for Q2 in their May Monetary Policy Report; however, this looks out of date after the stronger than expected boost to growth in May. GDP was boosted by stronger construction output and a slight upgrade to the index of services, which rose by 1.1% on a 3-month-on-month basis. Thus, we could see the BOE upgrade their growth forecasts when they next meet in August. This also makes a rate cut less likely from the BOE, as it would be unusual for the bank to cut rates at the same time as it upgrades its near-term GDP forecast.

There is also a chance that the UK’s inflation forecast could be revised higher. CPI is expected to be 2% this year and 2.6% next year, however, the rise in the living wage in April could still feed through to core inflation later this year, and the new Labour government may want to extend the living wage further, however, we may not find out there plans for this until the Budget later this Autumn. There is a decent case for the BOE to wait until we get the new government’s first budget before cutting interest rates, which may also help the pound, particularly since high interest rates do not seem to be hampering the UK’s continued recovery from last year’s recession.

3, Political risk premium

We would note that the political risk premium, which had limited GBP upside in recent years, may fall away as the Labour government enacts growth friendly policies and builds closer relationships with the EU. This is not something that will boost the pound in the near term, and its effect on sterling is hard to measure. However, now that the UK looks politically stable, especially compared to France and the US, the pound could attract ‘safe haven’ flows in the coming months, as the UK attracts more foreign investment, and as UK stocks start to look attractive again to foreign investors.

From a trading perspective, if GBP/USD can break above $1.30 in the coming days, then we believe that this pair could move up a level and trade back towards $1.40, the highest level since 2021.

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.