The European Central Bank is set to announce its sixth cut in this monetary normalization cycle today, bringing the deposit rate down to 2.5% from its current level of 2.75%. While today’s cut is almost fully priced in, investors remain uncertain about the path of interest rates, particularly at a time of uncertainty over tariffs, continued subdued economic growth, and plans for a significant expansion of defense spending in Germany and across the European Union.

German Fiscal Expansion and What It Means

Germany has announced an ambitious plan to boost government spending, including an easing of fiscal rules for defense and a €500 billion infrastructure fund. The bond market saw a historic move, with the yield on the 10-year German bond jumping around 30 basis points in a single session, the biggest increase since German reunification. Yields remain below 3%, and at current interest rates, it is difficult to see them rising further. On the other hand, expectations of a large bond issuance in the entire eurozone could also affect the overall price increase, which could be seen by the ECB as a factor limiting the potential for further cuts. At the same time, it is indicated that the potential neutral interest rate in the eurozone has recently increased from 1.8% to almost 2% and is now also indicating possible increases from 2026!

How many more times can the ECB cut rates?

After Thursday's cut to 2.5%, the ECB will approach the upper limit of the neutral interest rate estimate (1.5-2.5%), a level that neither stimulates nor inhibits the economy. The debate within the ECB is very loud:

- Hawkish positions (e.g. Isabel Schnabel) suggest that the neutral rate could be higher (e.g. 2.5% or more), pointing to growing climate investment and a shift from excess savings to excess bonds.

- Dovish policymakers (e.g. Piero Cipollone) argue that quantitative easing (QE) tightens financial conditions, justifying deeper cuts, potentially below 2%.

- Centrists in the Governing Council seem happy with a target rate of around 2%.

Assuming a neutral rate of 2%, after a cut to 2.5%, the ECB would have room for two more 25bp cuts, which would bring rates to 2%. However, in the face of geopolitical and economic uncertainties – including US tariff policy and German fiscal expansion – the scenario could change:

- Baseline:If economic growth remains weak and inflation falls below 2%, the ECB could cut rates further, even to 1%, which would mean six additional 25bp cuts from 2.5%.

- Alternative scenario: If German expansion stimulates growth and inflation, the ECB may suspend cuts at 2-2.5% and consider hikes in the longer term (e.g. from 2026).

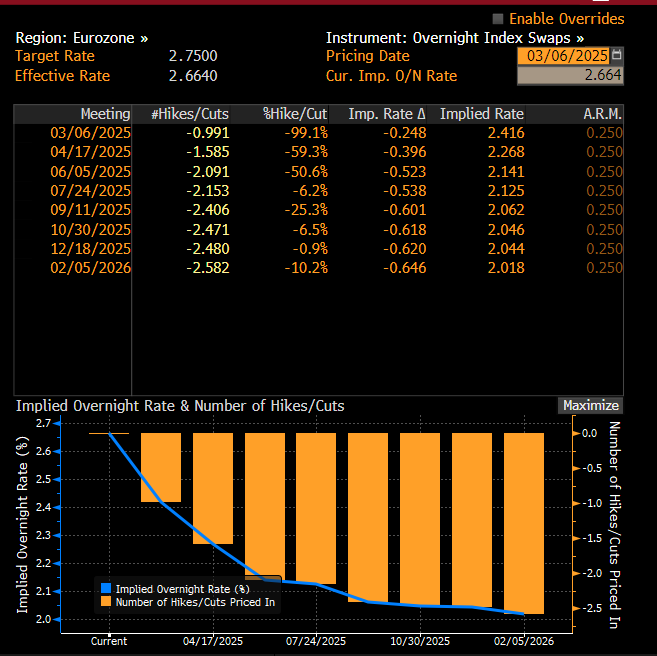

The market is currently pricing in less aggressive easing, and the chances of a cut in April have fallen quite significantly, with a 60% chance of a cut in April currently being priced in. Many commercial banks indicate that the current and April cuts will be the last in the cycle.

Interest rate expectations in the eurozone. Source: Bloomberg Finance LP, XTB

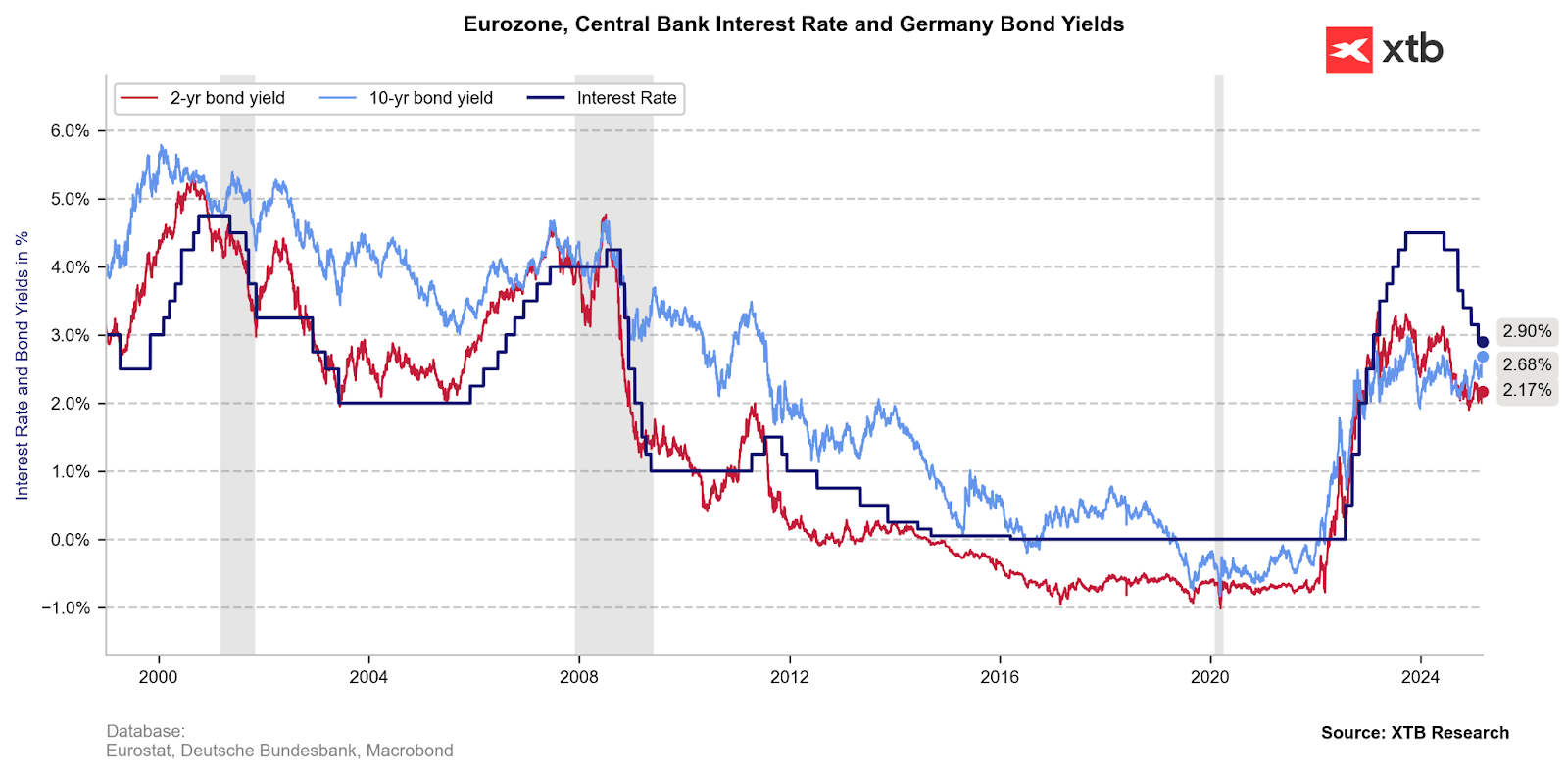

Yields, especially the 10-year ones, no longer suggest strong interest rate cuts. It is also worth noting that in the past, yields were characterized by a risk premium in relation to the level of interest rates. This potentially means that there is room for further yield increases, even with expectations of two cuts this year. Source: Macrobond, XTB

What next for the euro?

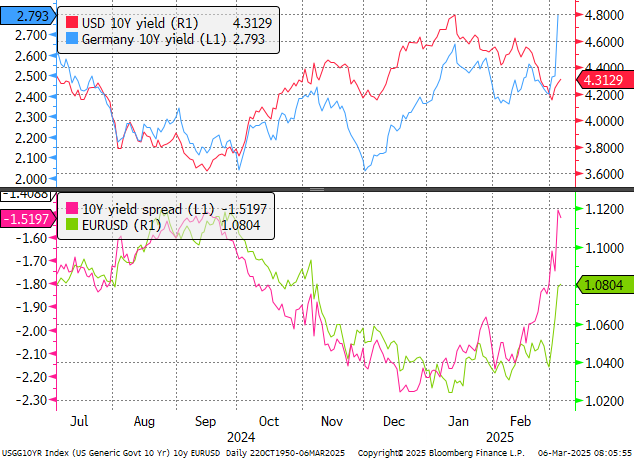

If Europe's economic plan succeeds, economic growth should accelerate, which will reduce the pressure for further interest rate cuts and also lead to a better performance of the euro on international markets. Additionally, the issuance of a large amount of high-yield bonds will encourage investors to leave their capital in Europe, which may also have a positive impact on the euro. Of course, tariffs and the war in Ukraine remain a risk for European assets. Although the recent movements seem excessive, it cannot be ruled out that on the wave of optimism, EURUSD will have a pretext for further growth, as indicated by the yield spread.

Currently, the yield spread is at its highest level since September 2024, when EURUSD was quoted at 1.1200. Source: Bloomberg Finance LP, XTB

Of course, if the United States were to decide on an open trade war with Europe, this could have a negative impact on the euro and return the EURUSD pair to the 1.02-1.05 range. However, a solid break of the 61.8 retracement of the last downward impulse could lead to an attempt to increase the pair to the area of 1.0950-1.10. In the context of today's movement, communication regarding further plans for interest rates in the eurozone will be key. Christine Lagarde will speak during the conference at 01:45 pm GMT.

Source: xStation5

NFP preview

Daily summary: Weak US data drags markets down, precious metals under pressure again!

BREAKING: US RETAIL SALES BELOW EXPECTATIONS

Politics batter the UK bond market once more, as Starmer remains under pressure

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.