The U.S. dollar strengthens while the US100 recovers early-week losses ahead of today’s Federal Reserve interest rate decision. Pressured by the US dollar, EURUSD pair loses almost 0.3%, dropping below 1.04 level ahead of US Federal Reserve decision scheduled at 7 PM GMT, and Powell speech at 7:30 PM GMT.

First Fed Decision of the Year Approaches

The Federal Reserve’s first rate decision of the year is in focus! While the market is almost 100% certain that rates will remain unchanged, the communication regarding future policy shifts could be crucial. Will the Fed maintain its stance on rate cuts, or will inflation risks take precedence, signaling a longer pause than initially expected?

Although today’s announcement may shift some focus away from the recent volatility in tech stocks and uncertainty surrounding Donald Trump, Fed Chair Jerome Powell might still face questions on these topics during the press conference.

What to Expect from the Fed?

The Federal Reserve has cut interest rates in its last three meetings, reducing rates by a total of 100 basis points. However, the December meeting marked a shift in tone, as uncertainty about inflation trends emerged. The Fed acknowledges a solid labor market and continued economic recovery, suggesting that further rate cuts could be delayed for a longer period.

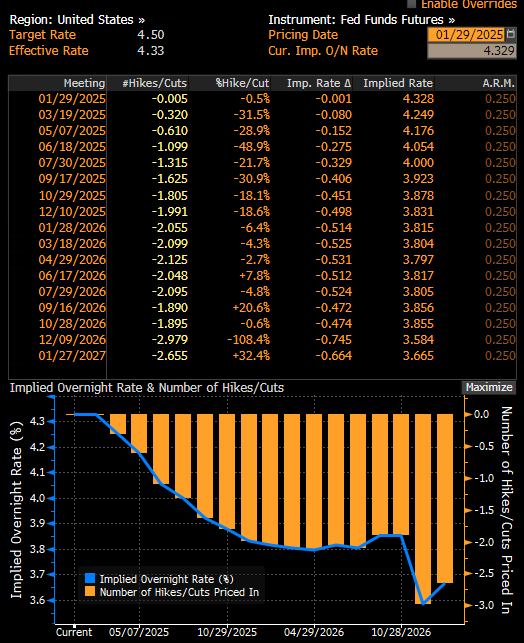

Thus, the Fed is expected to keep its benchmark rate unchanged at 4.5%, a move that has been clearly signaled in prior communications. Despite recent dovish remarks from Fed officials and mild pressure from Trump, the likelihood of imminent rate cuts remains low. Bloomberg's data suggests that the first full rate cut this year is currently priced in for June.

At present, no rate cut is expected in the near term, with the first cut priced in for June. Softer Fed communication has led to expectations of nearly two full rate cuts in 2024, aligning with the Fed’s December dot plot projection. If today's Fed statement is more hawkish than expected, the dollar could fully recover recent losses.

Currently, there is virtually no chance of a rate cut, with the first one this year priced in for June. Due to the softening of communication, nearly two full rate cuts are now being priced in for this year, aligning with the dot chart published in December. Source: Bloomberg Finance LP, XTB

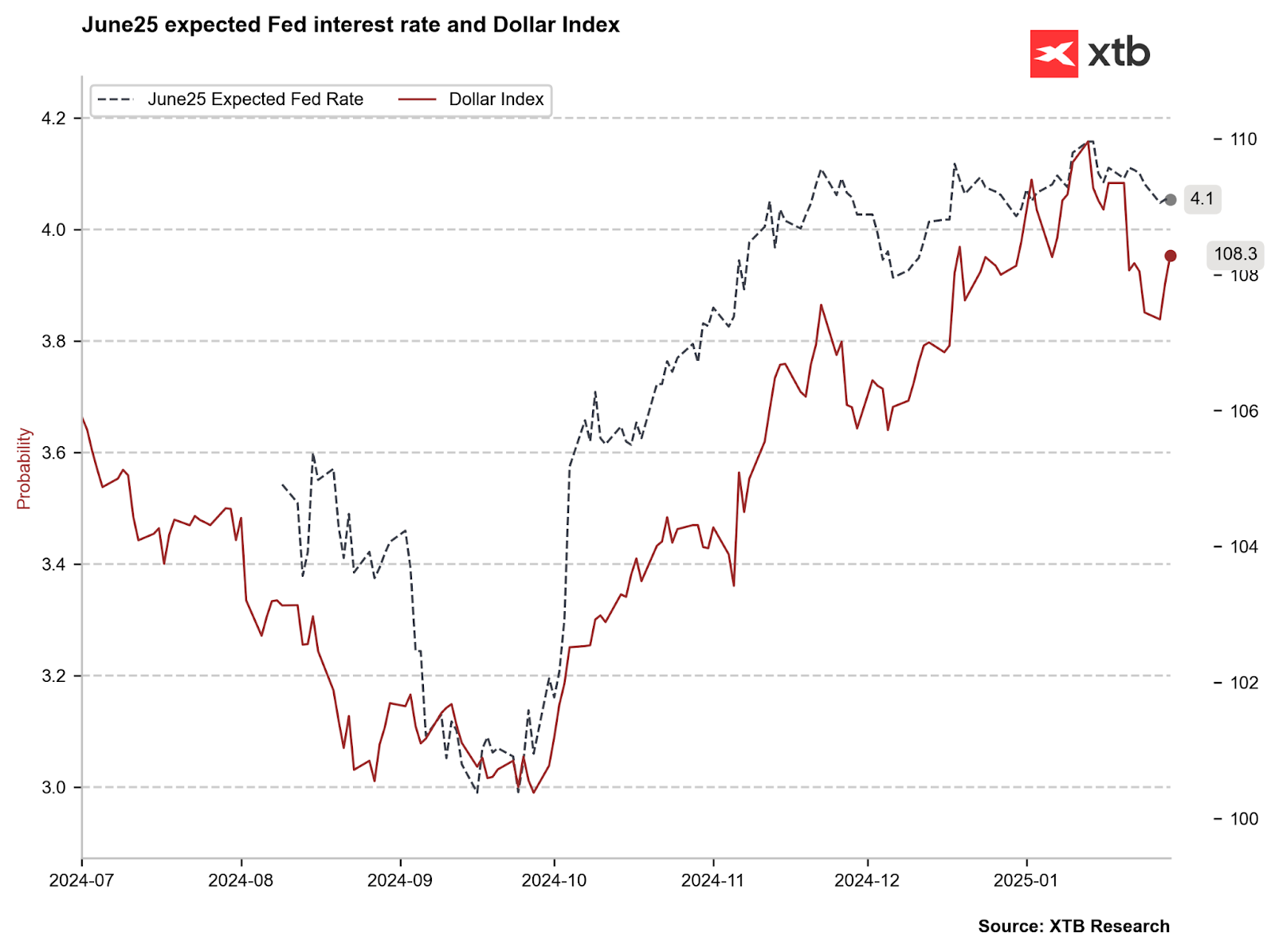

Rate expectations are stabilizing, while the dollar has weakened recently. If today's meeting carries an even more hawkish tone than the last one, there is a chance for the dollar to fully recover its losses. Source: Bloomberg Finance LP, XTB

Recent U.S. Economic Data Insights

-

Labor Market Strength:

December Nonfarm Payrolls (NFP) came in much stronger than expected at 265K vs. 165K expected (227K in November). The unemployment rate fell to 4.1% from 4.2%, though wage growth was slightly below expectations at 3.9% YoY (vs. 4.0% expected). -

Inflation Data:

- CPI: Headline inflation met expectations at 2.9% YoY, while monthly CPI held steady at 0.4% MoM.

- Core CPI: Monthly core inflation cooled to 0.3% (vs. 0.4% expected).

- Producer Prices (PPI): Core PPI flat MoM (0%), with headline PPI at 0.2% MoM (vs. 0.4% expected). Both YoY core and headline figures were lower than forecasts.

-

Business & Consumer Sentiment:

- PMI Data: January's preliminary services PMI fell sharply to 52.4 from 55.4 (vs. expectations for no change), while manufacturing PMI slightly improved (50.1 vs. 49.4).

- Industrial Production: Unexpectedly strong at +0.9% MoM in December (vs. -0.1% in November).

- ISM Services: Robust 54.1 (vs. 52.1 in November), with a sharp rise in prices subindex to 64.4 (from 58.2).

- Retail Sales: December sales were weaker than expected (+0.4% MoM vs. +0.7% expected), though still positive. Core retail sales were also slightly below forecasts (+0.4% MoM vs. +0.5% expected).

-

Consumer Confidence Weakens:

- University of Michigan Sentiment dipped slightly, with one-year inflation expectations marginally higher.

- Conference Board Consumer Confidence saw a notable decline, with a worsening labor market outlook – the first such drop since September.

-

Durable Goods Orders Decline for Two Consecutive Months:

- -2.2% in December and -2.0% in November, primarily due to weaker transportation sector demand.

Powell’s Likely Remarks and Market Reaction

Powell’s statement is expected to contain only minor wording changes compared to December. While he might highlight continued uncertainty regarding inflation, a significant shift in policy stance is unlikely.

It is also worth noting that the composition of voting members in the FOMC is changing this year. The 2024 committee was dominated by centrists, whereas 2025 will see a higher proportion of dovish members. This suggests that rate cuts remain on the table, and Powell is unlikely to adopt a significantly more hawkish tone today.

Will Powell Address Political or Tech-Related Market Issues?

- On Trump & Trade Tariffs: Powell is likely to avoid direct responses regarding Trump’s calls for lower rates or potential trade tariffs.

- On the AI Market Shock (DeepSeek): The recent sell-off in tech stocks due to China's AI launch is unlikely to prompt a strong response from Powell.

Market Impact: What’s Next for EUR/USD and US100?

EUR/USD Nears 1.0400 Before Fed Decision

The dollar has been strengthening this week due to capital outflows from equities and concerns over potential 2.5% trade tariffs.

- A Hawkish Fed Statement → EUR/USD may test 1.0350 support.

- A More Dovish Tone → EUR/USD could rise above 1.0460, potentially targeting 1.0500.

Source: xStation5

US100 Bounces After AI Sell-Off

The US100 index suffered a sharp decline on Monday, following the debut of China’s DeepSeek AI model. However, the index has since rebounded significantly.

Today’s Fed decision is unlikely to disrupt this recovery, but a clear signal that rates will stay higher for longer could reignite selling pressure.

- Key focus for US100 traders today:

- Post-market earnings reports from Microsoft, Meta, Tesla, and IBM will provide crucial insight into whether high equity valuations remain justified.

Source: xStation5

Daily Summary - Powerful NFP report could delay Fed rate cuts

BREAKING: US100 jumps amid stronger than expected US NFP report

Economic calendar: NFP data and US oil inventory report 💡

Morning Wrap: Dollar in a trap, all eyes on NFP 🏛️(February 11, 2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.