The US dollar is slightly strengthening ahead of the publication of November’s CPI inflation data from the US. The market expects CPI inflation to slightly rise compared to the previous month, while core CPI is anticipated to remain unchanged.

-

The market forecasts that the November CPI in the US will increase to 2.7% after 2.6% in October and 0.3% month-over-month, compared to 0.2% previously. Core CPI is expected to remain unchanged at 3.3%, with a 0.3% monthly growth rate.

-

Investors are pricing in an 85% probability of a Fed rate cut on December 18. On this basis, we can assume that a CPI reading above forecasts could lead to a drastic decrease in the implied chances of monetary easing in December.

-

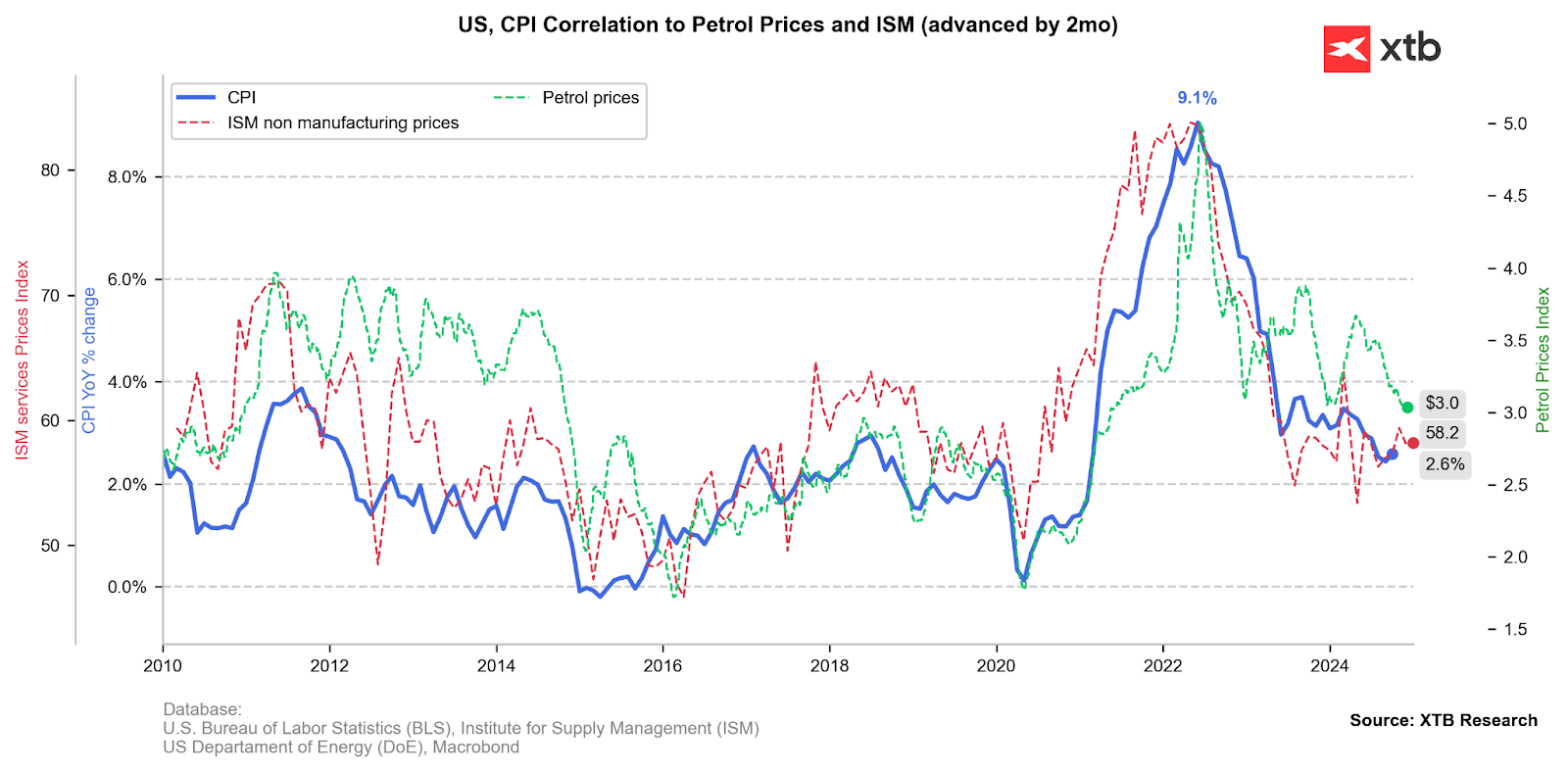

The price component in the latest November ISM services report indicated much stronger-than-expected price pressures. Meanwhile, short-term inflation expectations according to the University of Michigan survey increased; US consumers fear rising prices in light of potential new tariffs from the Trump administration in 2025.

-

Global oil prices remain low, and combined with slightly weaker data from the US labor market, they provide the Federal Reserve with room to extend the "window" for easing monetary policy through another rate cut.

Regardless of today’s CPI release, we believe that in the first half of 2025, the Federal Reserve will remain cautious regarding further rate cuts and will first want to assess how the new US administration’s policies impact price dynamics, consumer behavior, and the labor market. We also do not see cyclical weakness in the US economy, and if this situation persists in the coming months, the Fed may be inclined to maintain its policy unchanged. Consequently, the dollar and yields may remain strong in the medium term, even if the CPI comes in lower or aligns with expectations.

Recent publications and statements from Fed members suggest that the Federal Reserve is likely to remain cautious in signalling a looser monetary policy for the time being. On the other hand,

Contributions Indicate Less Deflationary Components

In recent months, many components have exhausted their deflationary potential. Energy prices, used cars, and food have been key factors supporting the continued decline in prices. However, the scale of these declines was so significant that the potential to maintain such dynamics has been diminishing month by month. Let’s take a closer look at the individual contributions and what we can expect from today’s reading.

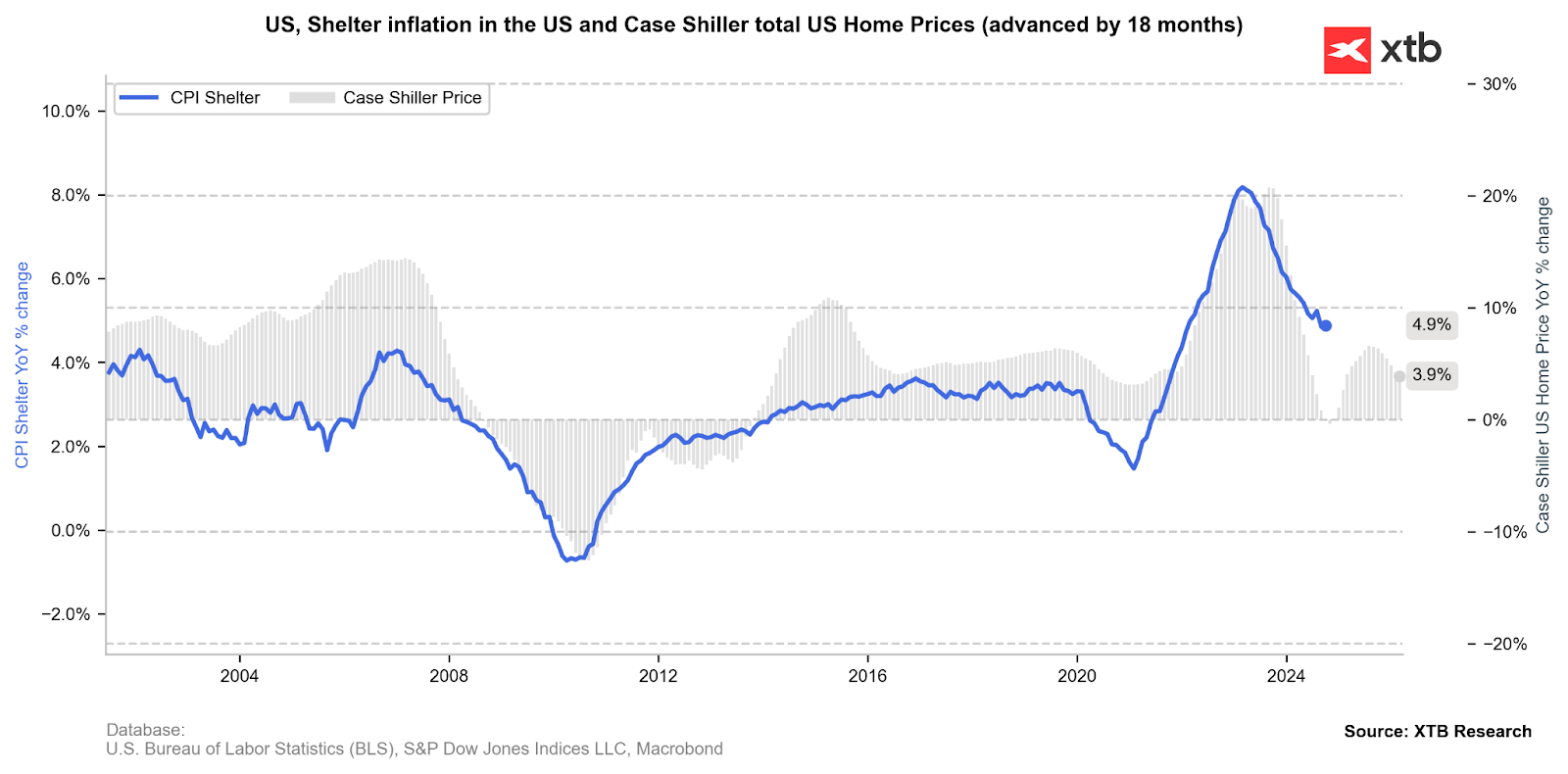

The Case-Shiller Home Price Index, with an approximately 18-month lead, suggests the price levels in the rental sector. This is the largest component of inflation, accounting for over 36% of the total inflation measure. The end of this year and the beginning of the next indicate that, in the short term, we may experience a slight increase in price pressure. However, in the longer term, housing prices have returned to a downward trend, suggesting potential short-term fluctuations.

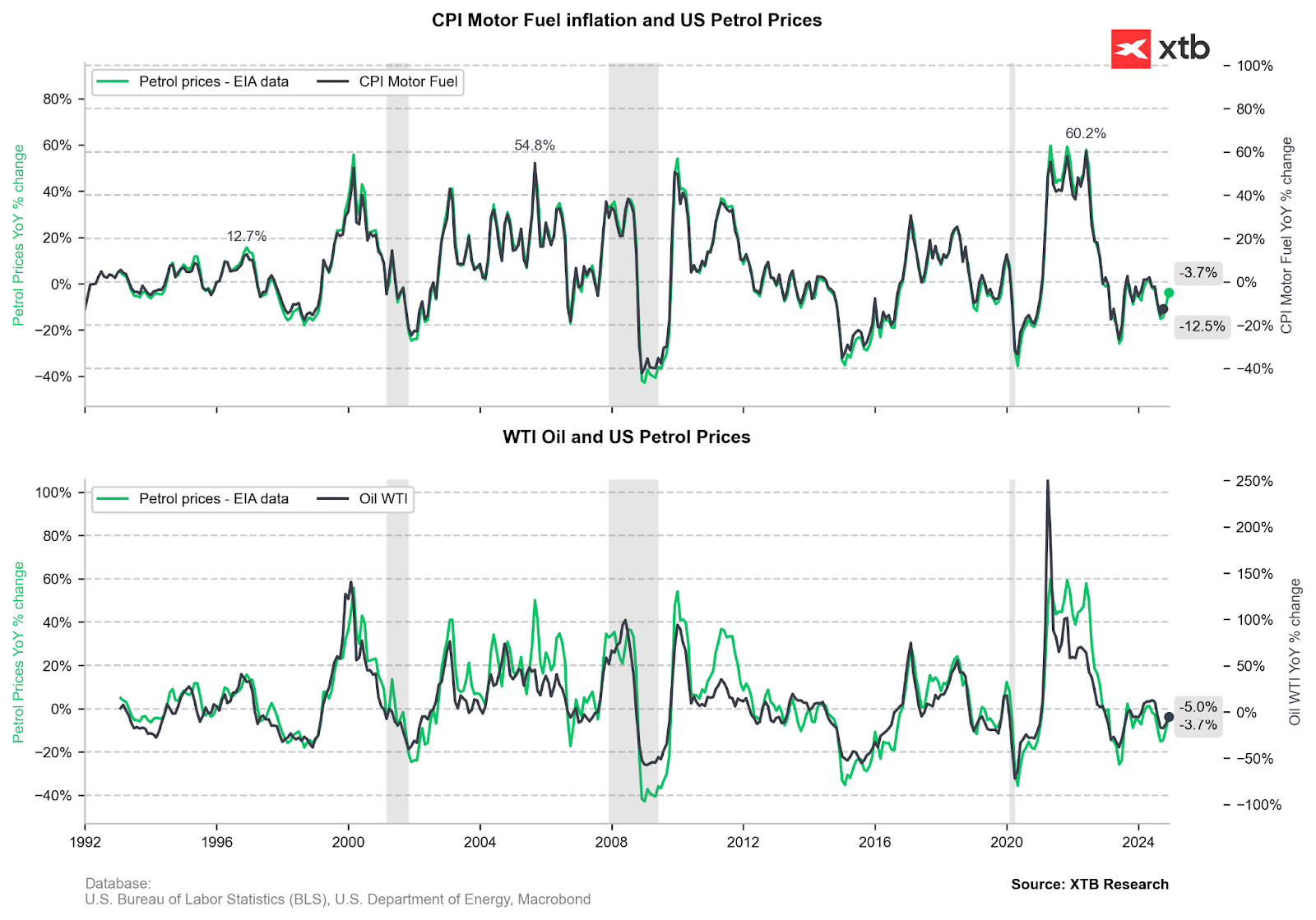

Energy prices, particularly oil, have risen over the past month. As a result, the negative impact of energy prices observed in recent months is unlikely to persist.

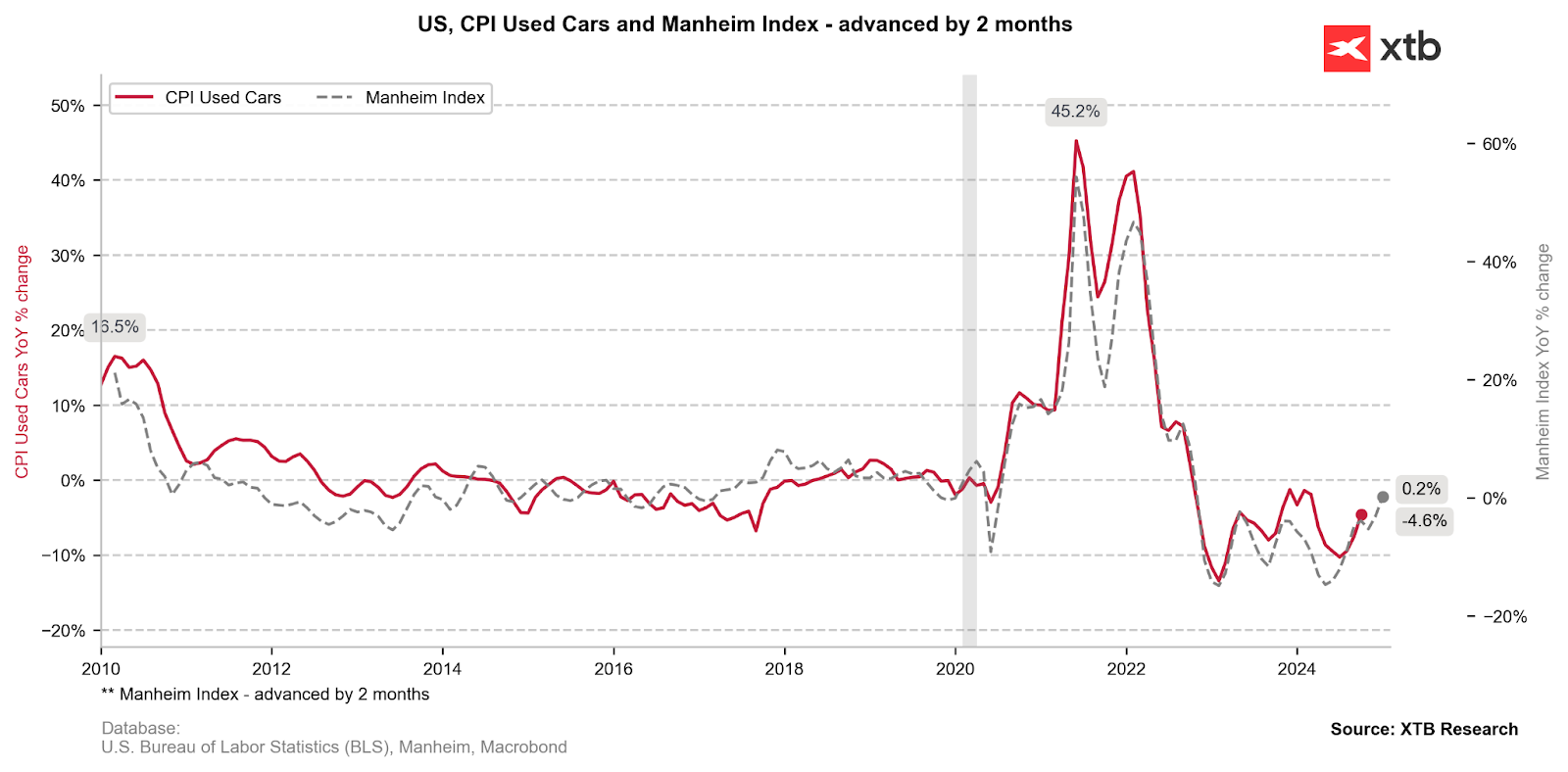

A similar situation is evident in the used car sector. Price dynamics have declined to such low levels that the potential for continued movement has been exhausted, and we are now observing a rebound from the deflationary zone.

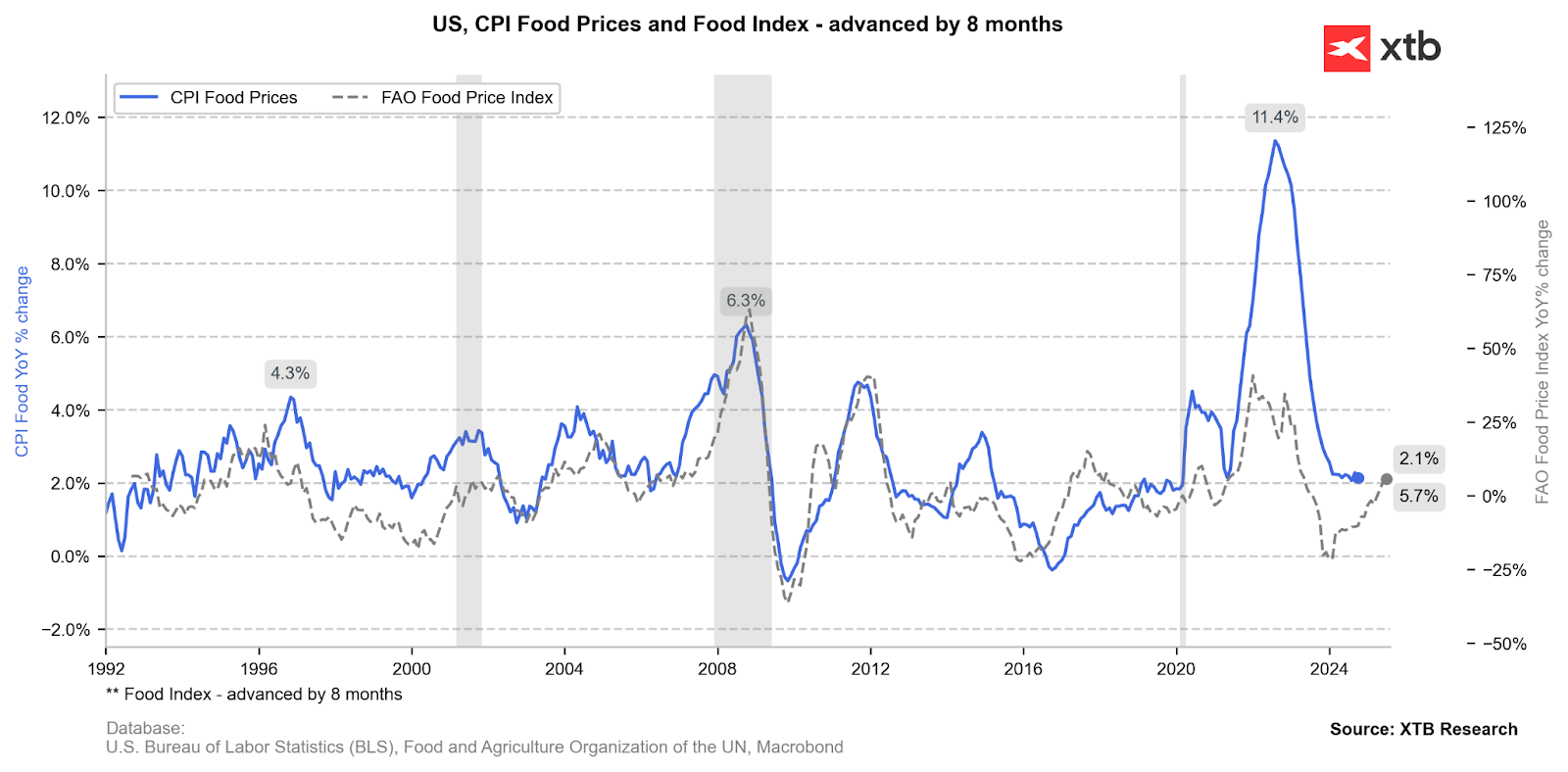

The situation is very similar for food prices. After temporarily remaining in the negative dynamics zone, prices are rebounding to the average levels of previous years. This does not necessarily indicate a return of inflation but rather a market normalization and the absence of a deflationary factor, as seen in previous months.

EURUSD Chart (D1 Interval)

Looking at the EURUSD pair on a broader daily interval, we see that the double-top pattern has played out at levels close to 1.11. If the 1:1 correction scenario does not materialize and the pair falls below 1.04 again, we could expect long-term pressure to test parity. Supporting this scenario is the dovish policy of the ECB, where bankers have not ruled out returning rates “below neutral.” Meanwhile, in the US, 2025 under the new Trump administration is shaping up to be quite hawkish. The yield differential may favor the dollar.

Source: xStation5

Daily summary: Weak US data drags markets down, precious metals under pressure again!

US Open: Wall Street rises despite weak retail sales

BREAKING: US RETAIL SALES BELOW EXPECTATIONS

US2000 near record levels 🗽 What does NFIB data show?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.