China's economic indicators show persistent deflationary pressures, with consumer prices rising less than expected and producer prices continuing to fall. Despite attempts to stimulate growth, the world's second-largest economy faces challenges in reviving domestic demand and combating overcapacity issues.

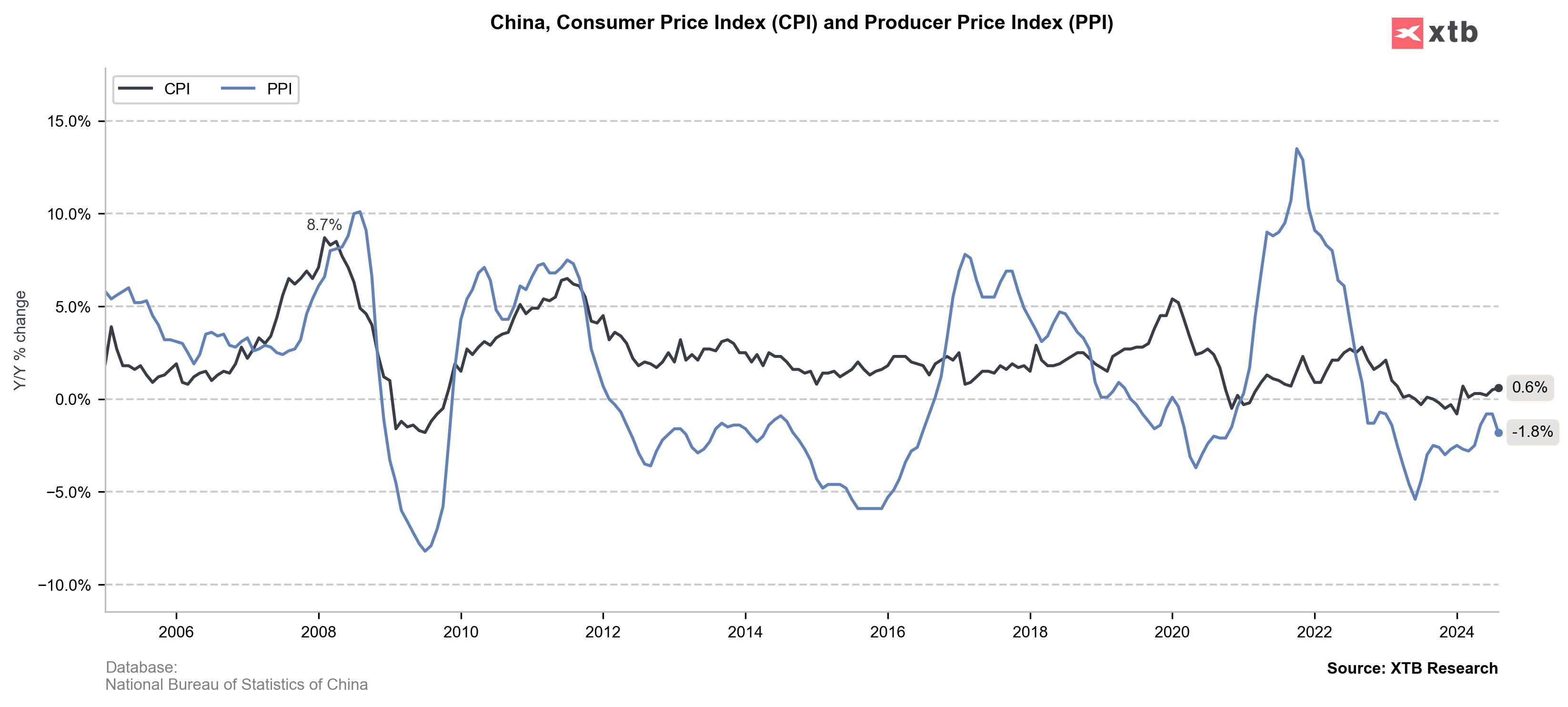

China's consumer price index (CPI) rose by 0.6% year-on-year in August, falling short of the expected 0.7% increase. This modest growth extends a period of economic weakness that has lasted over a year. Meanwhile, the producer price index (PPI) declined by 1.8% year-on-year, marking the 23rd consecutive month of contraction and exceeding the anticipated 1.4% decrease. These figures underscore the ongoing struggle with weak domestic demand and overcapacity in various sectors.

A key factor in the slight CPI increase was the rise in food prices, which climbed 2.8% year-on-year in August, the first positive print since June 2023. Pork prices, a significant component of China's CPI, surged by 16.1%. However, core inflation, which excludes volatile food and energy prices, rose by only 0.3%, indicating persistent weakness in underlying demand.

China's economic challenges persist

The inflation data stand in stark contrast to the government's efforts to stimulate economic growth. Retail sales rose by just 2.7% in July from a year earlier, reflecting subdued consumer spending. The real estate sector, a traditional driver of economic growth, remains in a prolonged downturn, further dampening domestic demand.

China's former central bank governor, Yi Gang, recently emphasized the need to focus on "fighting the deflationary pressure," calling for more proactive fiscal policies and accommodative monetary measures. The government has already launched a $41 billion campaign to support equipment upgrades and consumer goods trade-ins, but the impact has been limited so far.

The ongoing deflationary pressures are symptomatic of a broader issue of production surplus outstripping demand. This overcapacity problem, particularly evident in industries like steel and manufacturing, continues to weigh on producer prices and overall economic growth.

Despite these challenges, some analysts expect a "moderate rebound" in CPI in the second half of the year, driven by growing consumption demand and higher food prices. However, the persistence of deflationary forces has prompted global brokerages to scale back their 2024 growth forecasts for China to below the official target of around 5%.

Source: xStation

Source: xStation

CH50 (D1 interval)

The Chinese Index has started to decline based on the weaker than expected data. Only today it is down around 1%. It is also slowly approaching key support at 78.6% Fibonacci retracement at 11099. Currently it has also broken through the lower Bollinger band, which has previously been an opportunity for a reversal. RSI is in a downtrend and entering oversold territory. MACD also confirms bearish sentiment with space for further downside. For bulls to regain momentum the weekly close at 11306 must be broken. It would later on act as support while trying to break resistance at 61.8% Fibonacci retracement, which has previously been a strong support level in downtrend.

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

US jobs data surprises to the upside, and boosts stocks and pushes back Fed rate cut expectations

BREAKING: US100 jumps amid stronger than expected US NFP report

Market wrap: Oil gains amid US - Iran tensions 📈 European indices muted before US NFP report

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.