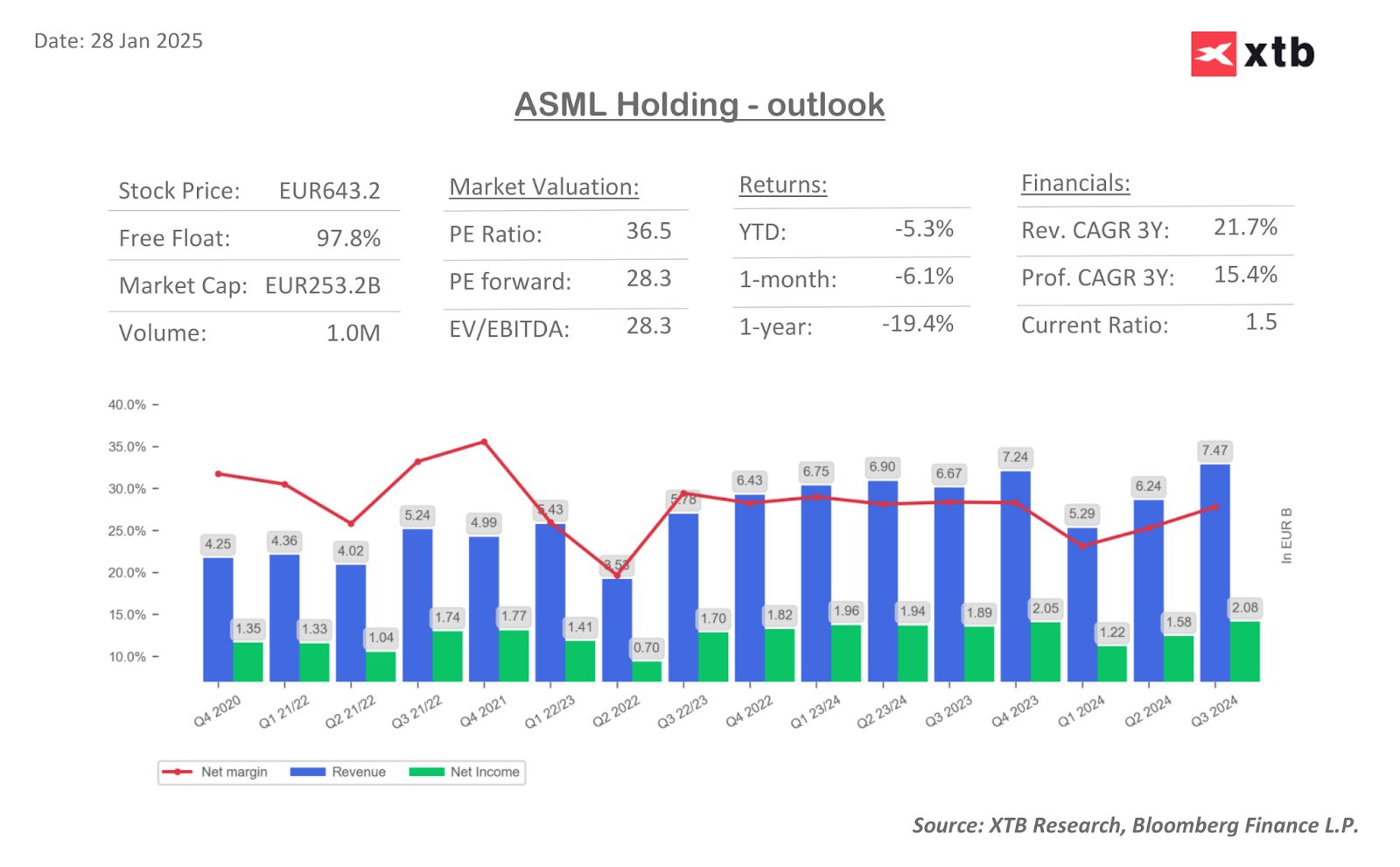

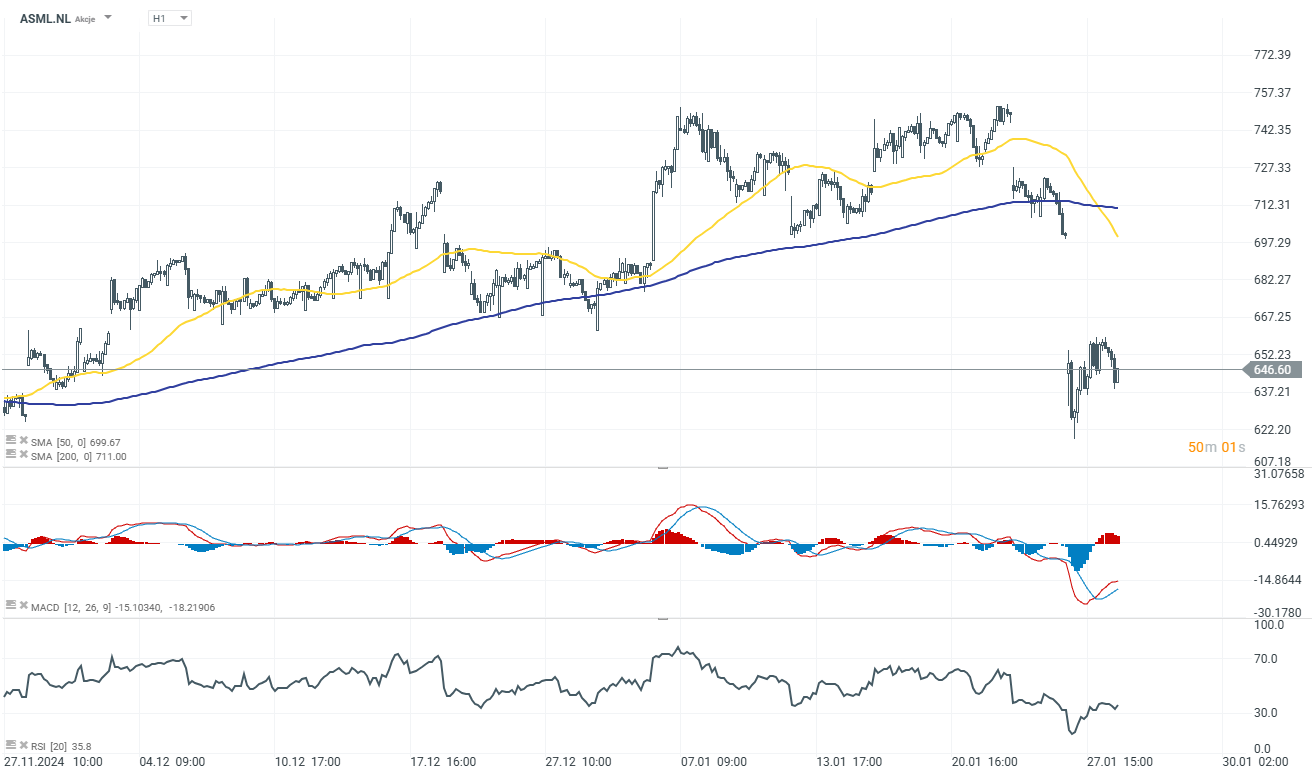

ASML Holding (ASML.NL) declines in today's session, further extending yesterday's losses. A global leader in semiconductor equipment, is set to release its Q4 2024 earnings on January 29, 2025 before market open. This report comes at a critical time as the company faces both opportunities and headwinds, including the emergence of China’s AI disruptor DeepSeek and ongoing geopolitical challenges. Below is a concise summary of what investors should watch for.

Key Points

- Revenue & Earnings Projections

- Q4 Revenue: Estimated at €9.02 billion, a 26.6% year-on-year increase.

- Net Income: Forecasted at €2.62 billion, reflecting robust demand for lithography systems.

- Gross Margins: Expected at 49.6%, slightly lower due to High-NA EUV system costs.

- Earnings Per Share (EPS): Projected at €6.68.

- Order Bookings & Systems Sold

- Q4 bookings are estimated at €3.53 billion, with 121 lithography systems shipped.

- EUV orders remain subdued, with analysts anticipating a €1 billion contribution.

- DeepSeek’s Impact

- The rise of DeepSeek, a Chinese AI startup using less advanced, cost-efficient chips, could reshape demand for high-performance semiconductors.

- DeepSeek’s approach raises concerns about long-term EUV sales, a key driver for ASML.

- 2025 Guidance

- ASML maintains its 2025 revenue guidance at €30–35 billion, though expectations lean toward the lower end due to geopolitical uncertainties and customer delays.

- Geopolitical and Customer Risks

- Ongoing U.S. export restrictions limit ASML’s sales to China, its third-largest market.

- Dependency on major clients like TSMC, Samsung, and Intel makes the company sensitive to spending cutbacks.

Analyst Commentary

- Citi: Highlights a lower hurdle for ASML following its recent share price drop, with expectations for bookings as low as €2 billion.

- JPMorgan: Expects ASML to meet 2025 guidance unless Intel/Samsung make drastic cuts. Sees 2026 orders from TSMC in H1 2024.

- Barclays: Does not anticipate significant near-term recovery in EUV orders, given lingering uncertainties.

- ING: Optimistic about strong order momentum, despite limited surprises expected for the full-year update.

ASML’s Q4 results will be crucial in understanding its strategy to address evolving challenges:

- AI Demand & DeepSeek’s Impact: Will ASML address risks of cheaper AI models reducing reliance on cutting-edge chips?

- China Exposure: 15–20% of 2023 sales came from China; updates on export controls and domestic competition (e.g., SMEE’s lithography tools).

- 2025 Guidance Confidence: Any revisions to €30B–€35B sales target amid geopolitical and demand risks?

ASML’s monopoly in EUV lithography (critical for AI/advanced chips) and €6.17B cash cushion provide resilience. However, DeepSeek’s rise, China risks, and customer concentration (TSMC, Samsung, Intel) pose challenges. The earnings call’s tone on 2024 order visibility and AI-driven demand shifts will be pivotal for sentiment. Watch bookings data and management’s 2025 confidence – a beat on €4B+ orders or upbeat EUV commentary could catalyze a rebound.

Source: xStation 5

Palo Alto acquires CyberArk. A new leader in cybersecurity!

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

US jobs data surprises to the upside, and boosts stocks and pushes back Fed rate cut expectations

Market wrap: Oil gains amid US - Iran tensions 📈 European indices muted before US NFP report

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.