Countries and regions around the world are now developing emissions carbon trading schemes as a way to put a price on greenhouse gas emissions. Such emission trading systems are currently operating in Europe, North America, and parts of Asia, and are being considered for eventual introduction worldwide.

Given the difficulty of reaching agreement on climate change mitigation measures in international negotiations, it is clear that the momentum has shifted from the international level to the level of nation states and smaller regions.

Particularly strong dynamics are evident in rapidly developing economies where new emissions trading schemes are being discussed or have already been established in China, India, South Korea and even Brazil. Globally, 39 national jurisdictions and 23 subnational jurisdictions have implemented or plan to implement carbon pricing instruments, including emissions trading schemes and taxes.

The world's largest carbon emissions market is the European Emissions Trading System (EU ETS), and this article outlines what the EU ETS is and what emissions carbon trading looks like.

What is EU ETS?

The European Union Emissions Trading System, or EU ETS for short, is an instrument to reduce greenhouse gas emissions.

The European Union Emissions Trading Scheme (EU ETS) is the world's first and so far largest "cap-and-trade" system for reducing CO2 emissions into the atmosphere. The system is designed to help the European Union meet its CO2 reduction goals by promoting emission reductions in a cost-effective and economically efficient manner for businesses, states, and other economic entities. EU ETS is one of the tools of decarbonisation and fight against climate changes.

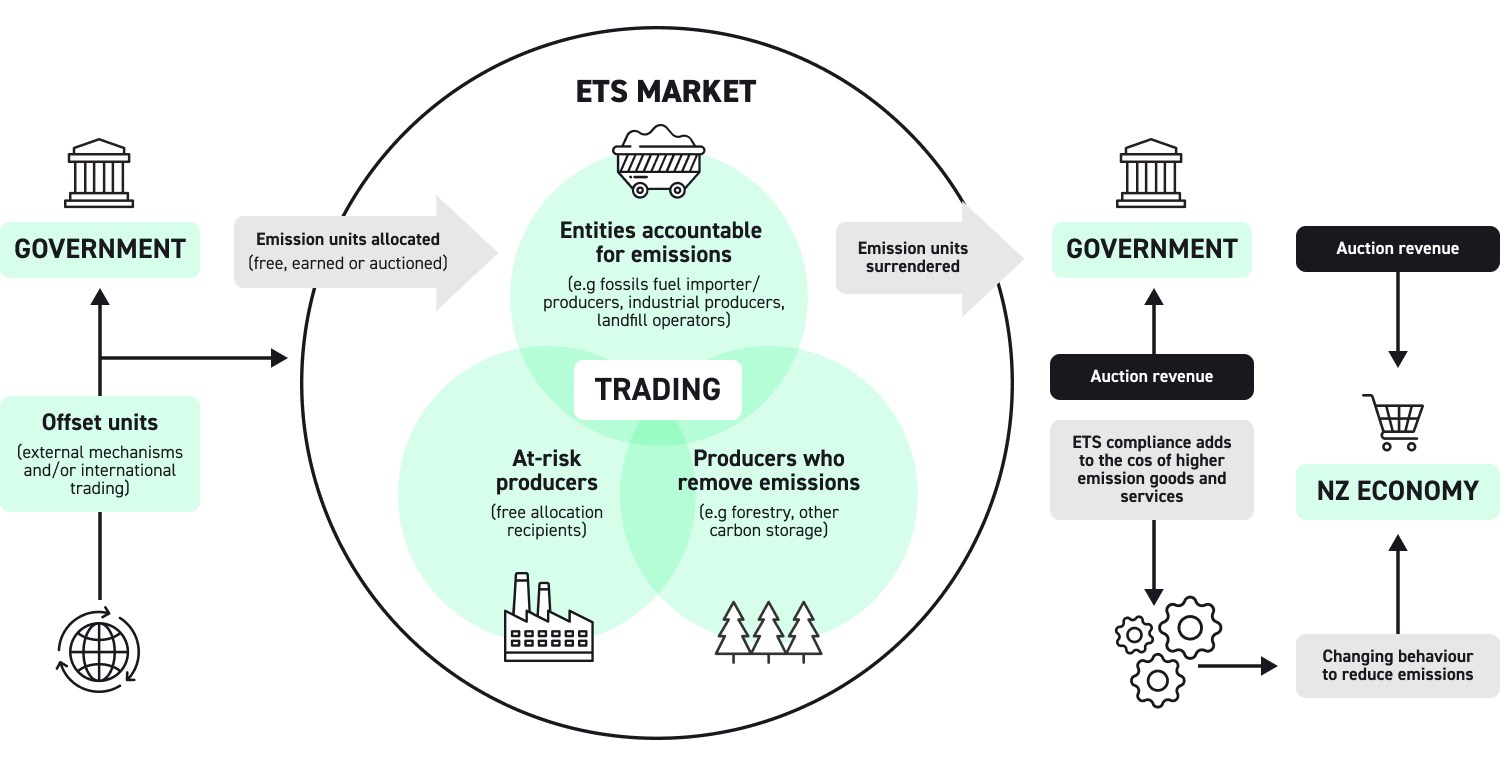

The main features of the EU ETS are the emission cap, i.e. the maximum quantity cap, and trade in EU emission allowances (EUAs). The cap guarantees that total emissions are kept at a predetermined level (they cannot increase as long as the cap is valid). Installations subject to the cap must surrender EUAs (European Union Allowances) for each tonne of CO2 equivalent emitted into the atmosphere during the year.

EUAs are allocated for free or auctioned. The trading system offers flexibility to covered companies as they can choose to take action or buy EUAs depending on the EUA price, which provides an opportunity to trade

In this way, those emitting CO2 whose abatement costs are lower than the price are encouraged to take action. On the other hand, those emitting CO2 at high abatement costs can buy EUAs and postpone their own actions, thereby meeting the European Union's GHG requirements more cheaply than they would be able to do if all emitters had the same constraints.

In order to accurately track EUAs, EU ETS participants must open a special account with the European Union. Any holder of such an account can buy and sell EUAs regardless of whether they are covered by the EU ETS or not. Trading does not require intermediaries and can be carried out directly by buyers and sellers through organised exchanges or through intermediaries.

We analyse and understand the latest trends in the economy and that is why we provide leveraged trading of EUA CFDs on our proprietary xStation platform.

Fit for 55

The tightening of the EU's overall emissions target to -55% reduction relative to 1990 under the European Green Deal requires tightening the current EU ETS reduction target for 2030 to -43% relative to 2005.

The EU Commission proposes in its "Fit for 55" package to increase the EU ETS reduction target for 2030 to -61% relative to 2005.

Such a restrictive EU ETS target will further increase the EUA shortage and thus EUA prices. Modelling studies estimate coal prices in the range of 90-130 euros/tCO2 for 2030.

The EU Commission also proposes to include emissions from maritime transport in the EU ETS. New Emissions Trading Scheme for the Transport Sector; in its Fit for 55 package, the European Commission has proposed an entirely new emissions trading scheme for fuel distribution in road transport and buildings.

This system will operate independently of the EU ETS and is expected to start operating in 2025, with an emissions cap to be set from 2026. This new upstream system will regulate fuel suppliers.

The cap in the new ETS will be lowered annually to achieve a 43% reduction in emissions in 2030 compared to 2005. 25% of the revenue from the new trading system will go to the Social Climate Fund, where it is to be invested in energy efficiency in buildings, clean transportation, and can also be used to directly help households struggling with higher gasoline or heating costs.

Some EU members are concerned that full implementation of the FIT to 55 program could result in higher prices for emission allowances, airline tickets, electricity, heating (gas, coal), fuels (gasoline, oil), and transport. Price increases in these sectors could affect many industries.

Measuring the total carbon emission doesn’t alway paint the most accurate picture of a country’s contribution when its population isn’t taken into account.

For example, even though China is the highest emitter of CO2, the average American is responsible for producing more tonnes of CO2 per person compared to a Chinese citizen.

A brief history of EU ETS

The origins of the EU ETS date back to 1992, when 180 countries agreed to avoid dangerous levels of man-made global warming and signed the United Nations Framework Convention on Climate Change (UNFCCC). In 1997, the Kyoto Protocol was established, which introduced two principles necessary for the establishment of the EU ETS.

The protocol included absolute quantitative emission targets for industrialised countries and a set of so-called flexible mechanisms that allowed emission credits to be exchanged between countries under the international emissions trading scheme.

Several countries were introducing national emission reduction policies (such as support for renewable energy), but others were waiting for common and coordinated policies and measures to be introduced across the EU. The European Commission then began work on a proposal for an EU emissions trading scheme to deal with emissions from key sectors of the economy - energy and industry.

As a result of these considerations, the EU ETS was established as one of the key policy measures to achieve the climate goals set by the Kyoto Protocol. It now covers 28 Member States, as well as Iceland, Liechtenstein and Norway who joined in 2008.

The EU ETS is organised into trading periods, of which four are currently fixed and others will follow.

2005-2007

The European Parliament adopted the law establishing the EU ETS in October 2003. The first phase of the EU ETS was an initial phase designed to test the system. Member states were free to decide how many European Union Allowances ( EUAs ) to allocate in total and to each installation in their territory by preparing national allocation plans. Almost all EUAs were allocated for free and were based on historical emissions. In this phase, CO2 emissions from installations for electricity and heat production and in energy-intensive industrial sectors such as iron, steel, cement, oil refining, etc. were covered. The penalty imposed on companies for non-compliance with the restrictions was €40 per tonne of CO2.

This initial phase succeeded in establishing a price for EUAs, free trading across the EU, and an infrastructure for monitoring, reporting and verification (MRV) of actual emissions from covered installations. The ETS reduced about 200 million tonnes of CO2, or 3% of total verified emissions, at nominal transaction costs. In the first year of the system's operation, regulators concluded that too many EUAs had been allocated to companies, which led to an oversupply of EUAs. The consequence was a drop in their price, which eventually fell to zero.

2008-2012

This period was directly related to the earlier commitment period under the Kyoto Protocol. The EU imposed a strict emissions cap by reducing the total amount of EUAs by almost 7% compared to 2005. The scope was amended to include nitrous oxide from nitric acid production in member countries. From 2012, the scheme also covered flights within EU ETS countries. Up to 10% of allowances could be auctioned by member states instead of free allocation. The penalty for non-compliance increased to €100 per one tonne of CO2. Companies were allowed to use credits from the Clean Development Mechanism and Joint Implementation of the Kyoto Protocol, which led to a total of nearly 1.5 billion tonnes of CO2-equivalent credits in the market. The move was designed to offer companies cost-effective mitigation options and made the EU ETS a major driver of the international emissions market.

The economic crisis of 2008 caused companies in the EU to reduce their emissions, which once again led to a large surplus of EUA allowances and once again resulted in the price falling from €30 to less than €7.

2013-2020

The European Commission revised the EU ETS for the implementation of the third phase. There were many reasons for the changes.

The fall in EUA prices in the second phase significantly undermined the credibility of the EU ETS. Second, the EU ETS did not lead to significant transformations or shifts towards renewable energy sectors or low-carbon technologies to the extent expected.

Third, the system has proven to be cost inefficient. The system has also been subject to fraud on several occasions. To address the weaknesses of the system, the changes introduced in this phase include, in particular, an emissions cap applied uniformly across the EU to achieve the GHG reduction target more effectively. The cap is decreasing by 1.74% per year, in 2020 it reduced emissions by 21% compared to 2005.

The main allocation method has been changed to market sales. Trading platforms for the EU ETS are available to every country that participates in the system. The auctioning process is overseen by the EU ETS Auctioning Regulation to ensure that they are conducted in a transparent and regulated manner. The revised EU ETS Directive states that auctions must meet criteria such as predictability, cost-effectiveness and fair access to the auctions and simultaneous access to relevant information for all operators.

Free allocation applies to industrial installations other than for electricity generation based on benchmarks (BM). The BM index determines the number of free EUA allowances based on the production (or input) of the installation. There is a BM for each product, e.g. for steel, cement and lime. This level will be reduced annually. Industries at risk of carbon leakage receive 100% allocation throughout the trading period.

The main challenge in the last trading period was the surplus of EUA allowances carried over from 2008-2012, which led to falling EUA prices. For this reason, the European Union decided to postpone the auction of 900 million EUAs to the end of the trading period (the so-called controversial backloading). The European Commission proposed the introduction of a market stability reserve in the next trading period, which should balance supply and demand by adjusting the auction size.

How to start emissions CFD trading

Carbon trading is available on our xStation trading platform. You can start your carbon emission trading by entering into CFD (contract for differences) transactions on the EMISS instrument and use the leverage.

By trading emission contracts you can take advantage of market volatility and open positions during very fast price movements. Leverage can multiply a day trader's profits, but please bear in mind it can also easily multiply your losses. Trading CFDs on EMISS is dedicated to active traders who are prone to risk and look for price volatility.

Thanks to the 1:5 leverage, you only need a 20 % margin to open a position. For example, by using 1000 USD you can open a contract which is worth 5,000 USD. Because of leveraged CFD instruments, the high risk level potential revenue of the position also can be high, but the potential loss can also be higher as a result.

You can learn more about CFDs and financial leverage from this article on CFD trading.

CFD trading on VOLX is speculative and for suitable active traders only, as the price fluctuations matter on this instrument. This type of contract is a financial agreement which pays out the difference in settlement price between open and closed transaction without any physical delivery of the traded instrument.

VIX trading on VOLX gives traders the opportunity to open short and long positions. Short positions give traders the opportunity to make profits when the VOLX price is falling.

Online trading allows you to trade VOLX without leaving home, with zero commissions and low spreads. Also due to the liquidity of the VOLX market you can close your position with one mouse click at any time when the market is open.

This is why VOLX contracts trading has some advantages. Trading VOLX CFD gives traders the opportunity to open short and long positions. Short positions give traders the opportunity to make profits when prices of contracts are falling. However, please bear in mind that as always when trading leveraged instruments, both your profits and losses can be multiplied when trading VOLX CFD.

The only fees you incur in this case are the spread (the difference between the ASK buy price and the BID sell price) and swap points. The spread is very small and costs cents depending on the size of the position. Swap points are the costs that the broker incurs when financing leveraged positions; swaps are charged daily to the open position on the EMISS instrument.

Best time to start trading

Carbon dioxide, often abbreviated CO2, is a colourless greenhouse gas created by the burning of fossil fuels. Carbon dioxide is a natural and important part of the atmosphere, yet levels are higher today than at any point in at least the last 800,000 years, according to the U.S. National Oceanic and Atmospheric Association.

Increased CO2 emissions have trapped heat in the atmosphere, thus raising the Earth's average temperature and causing extreme, historically rare weather events and very rapid, dangerous climate change that can lead to disasters but also famine or crop destruction.

The global reduction in transport and human movement caused by the COVID 19 pandemic was expected to significantly reduce global CO2 emissions, but they have fallen by only a few percent and are rising again despite decarbonisation, green policies restrictions and lockdowns in some parts of the world.

Halving greenhouse gas emissions by 2030 and achieving carbon neutrality by 2050 are the two goals on which European Union policy is currently focused. Decarbonisation is one of the most important climate goals for the EU and the world. It is also planned to accelerate the mechanism for adjusting carbon emission limits, for which it is necessary for large emitters to participate in carbon quotas.

Climate change and combating energy insecurity are the main issues under debate in Europe.

The EU institutions will be debating the Fit for 55 program and the European Green Deal in the coming months. Information about possible blackouts and lack of energy security makes fossil fuels such as coal still very popular, despite recommendations from the EU, driving up EMISS prices.

The European Commission will ultimately aim to replace fossil fuels by promoting wood in the building sector and electricity production using bioenergy. Nature-based solutions cannot be scaled up indefinitely, however, and the EU will want to influence the reduction of CO2 emissions with new technologies as well.

Although these technological solutions are still very young and need time, they are nevertheless promising - CO2 removal is sustainable.

By 2030, 5 million tonnes of CO2 should be removed from the atmosphere each year in the EU and permanently stored using modern technological solutions. Another way to reduce emissions is to transform CO2 from a waste product into a resource and use it as a raw material to produce chemicals, plastics or fuels e.g. the production of methanol from CO2 can start the way to green plastics.

By 2030, at least 20% of the carbon used in the chemical and plastics industries should come from non-fossil sources, according to the EU strategy.

Now, however, in times of an energy crisis, the Commission may have a problem enforcing all of the provisions while keeping each member state's energy sector intact.

The price of coal in Europe could reach as high as $113 a tonne by the end of 2022, analysts say, after surging nearly 50% since early November. The energy crisis, rising gas prices and the approach of expiring options could make carbon emissions even higher than now.

The emissions trading system (ETS), which requires manufacturers, energy companies and airlines to pay for every tonne of carbon dioxide they emit, is central to the European Union's efforts to cut greenhouse gas emissions.

Economists surveyed by Reuters conveyed that the system requires prices of about $100 per tonne to encourage companies to switch to cleaner fuels and technologies to reduce emissions in line with the goals of the 2015 Paris climate agreement and the Kyoto Protocol. Green solutions are still relatively expensive and for many companies using them is a major obstacle to optimising profits.

Coal-fired power plants must buy more carbon permits to account for their very high emissions. The more "dirty" fuels like coal are used, the higher EMISS prices investors can expect.

Gas contracts are rising due to forecasts of a cold winter, maintenance of major gas infrastructure and tensions between gas-producing Russia and Western countries and the USA (NordStream 2 pipeline).

The U.K. launched its own national ETS in 2021 after leaving the European Union system after Brexit, where coal is trading just below EU valuations. The U.K. ETS has a cost containment mechanism that allows British regulators to interfere with domestic prices. Britain's actions could prompt European countries to call on the EU to take similar steps, according to investors.

To sum up, the coming years seem to be a great time to actively trade emission contracts EUA due to high price volatility, extraordinary liquidity of this instrument and of numbers of political events, decisions and currently debated energetic problems inside the European Union.

Thanks to regular information and the energy crisis, investors can form their own opinion on the CO2 contract prices and implement their investment strategies.

Carbon contracts are a risky instrument with high price volatility and investors interested in trading them should keep track of the latest news on EU climate and energy policies to adjust their positions to upcoming market events. Our carbon trading offer due to its volatility and popularity also allows active traders who are not interested in reading the news to trade only on instrument price action based on technical analysis indicators we provide in our trading platform, or to look for temporary price advantage to open positions.

EMISS Trading hours

What about available EMISS trading hours? This information is especially important for day traders. Emissions trading is available 5 days per week from 8:05 CET to 18:00 CET from Monday to Friday. Carbon emissions trading is not available during weekends on our platform. EMISS spot price is static when the market is closed. At all other times the prices are constantly fluctuating.

Of course, the best time to trade carbon emissions is during periods of very high liquidity, when market volatility is higher.

When there is a high turnover in the market and trading volume increases, the volatility also increases. This can be influenced by the publication of important news regarding the climate, information from the press or even rumours regarding changes in CO2 emission restrictions.

What Is Leverage in Trading?

Coffee Trading - Investing in Coffee CFDs

Is Gold Becoming the World's New Reserve Currency? | Gold Investing

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.