- European indices showed mixed performance, with key markets under pressure. The UK100 managed a slight gain of 0.39%, while France's FRA40 added 0.45%. Germany's DE40 edged up 0.30%, but Italy's ITA40 declined 0.20% and the Netherlands' NED25 dropped 0.19%.

- US stock market shows strength, with the US30 leading gains (+0.73%). The US500 climbed 0.38% to 6078.2, while the broader US100 advanced 0.19% to 21720.65. The US2000 also participated in the rally, rising 0.49% to 2325.6. Markets anticipate Netflix earnings report after the session on Wall Street

- The US Dollar index (USDIDX) erased early gains, now losing almost 0.15%, while EURUSD rises 0.2% above 1.043 level, trying to reverse the downtrend. The 10-year US treasuries yields are down almost 3.5 p.p today, now at 4.57% as Trump still didn’t announce tariffs decision on Chin and European markets

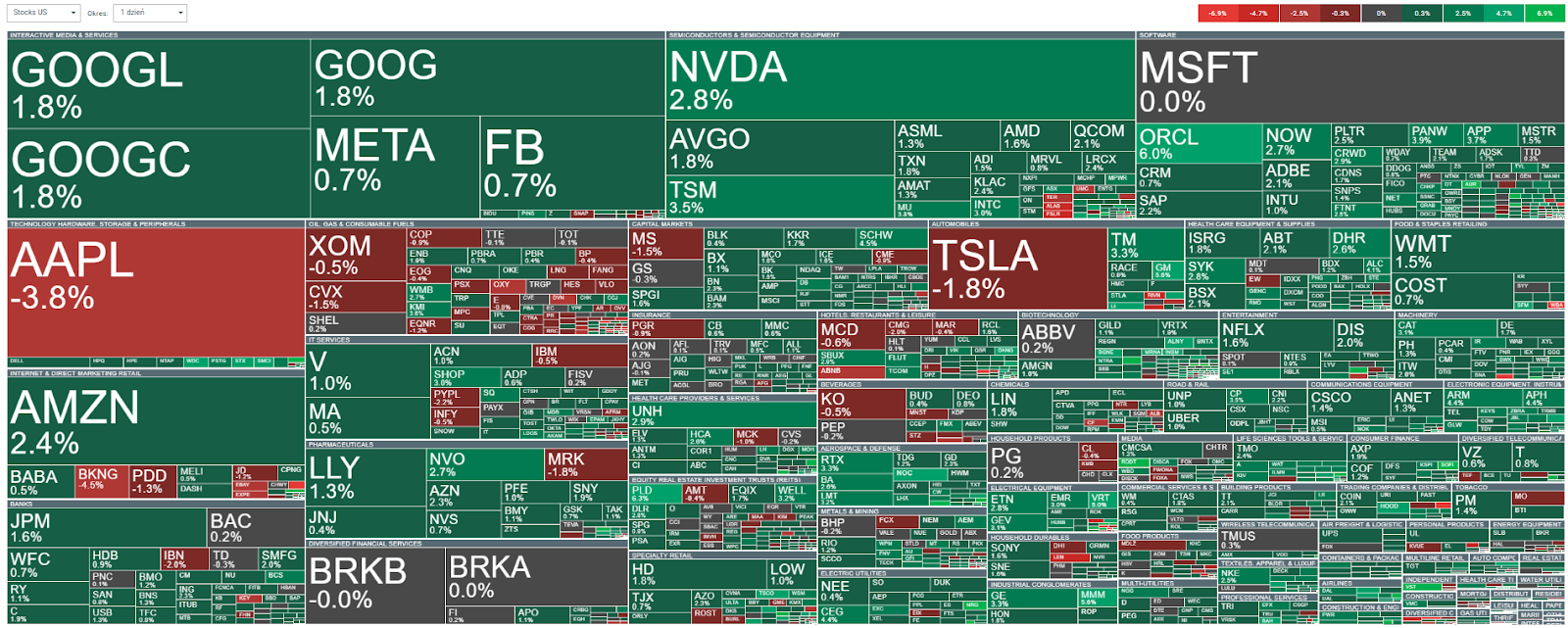

- Apple shares are down 4% today as the company faced headwinds in China with iPhone sales down 18.2% in the latest quarter, contributing to a 5% global decline. The company's challenges stem partly from delayed AI feature rollouts in the Chinese market as it searches for a local AI infrastructure partner. The stock is currently testing critical support at its 200-day exponential moving average.

- Oracle surges 6% after CBS reported that US will invest in AI-private sector, with forming a ‘Stargate’ group by Oracle, Softbank and OpenAI as one of the main beneficiaries

- Charles Schwab delivered strong Q4 2024 results, exceeding expectations across key metrics. The company reported adjusted EPS of $1.01 versus $0.91 forecast, with net revenue hitting $5.33 billion. Trading activity showed particular strength with 6.31 million average daily trades, significantly above the expected 6.04 million, marking the highest activity levels since Q4 2022.

- 3M (MMM.US) shares jumped over 4% after beating Q4 expectations with $6 billion in revenue. The company's security and industrial segment showed particular strength with a 21% operating margin. Looking ahead, 3M provided 2025 guidance for adjusted EPS of $7.60-$7.90, with comparable sales growth projected at 2.5%.

- Space exploration stocks soared following Trump's Mars mission announcement. Redwire Corp led gains with a 37.8% surge, followed by Rocket Lab USA jumping 28.3%. The rally extended across the sector with Planet Labs rising 21.4% and Momentus up 17.6%. Even traditional aerospace giants Boeing and Lockheed Martin saw modest gains of 2.2% and 2.3% respectively. RTX corp rises almost 3% on Trump ‘US Iron Dome’ announcement

- The precious metals sector showed strong performance, with palladium leading gains at +2.69%, followed by gold (+1.24%) and silver (+0.87%). The rally comes despite earlier dollar strength, suggesting underlying safe-haven demand and technical buying.

- Energy markets remained under pressure with natural gas leading declines (-1.96%), followed by LSGAS (-1.62%) and crude oil products. The weakness persists after Trump’s oil proposals. In the effect US Oil&Gas is one of the weakest market sector today

- US wheat futures surged over 3% today, reaching levels unseen since December 2024. The rally comes as Trump signaled a less aggressive approach to tariffs and delayed implementation of trade policies with China. A weakening US dollar provided additional support for agricultural commodities, though CoT data reveals specs are holding substantial short positions of nearly 95k contracts, setting up a potential short squeeze scenario.

- Cryptocurrency markets showed broad strength, with Dogecoin leading major cryptos with a 6.60% gain. AAVE and APECOIN followed with gains of 5.10% and 4.67% respectively, while Bitcoin traded up 3.57% at $107,000. Ethereum gains 0.8% to $3335. The sector's resilience comes despite a dip after Trump inauguration.

Apple is one of the weakest US stocks today, while overall sentiments positive. Source: xStation5

US100 ร่วง 1.5% 📉

ข่าวเด่นวันนี้

🚨 ทองคำร่วง 3% ขณะที่ตลาดเตรียมตัวเข้าสู่ช่วงหยุดตรุษจีน

การขายทำกำไรในปัจจุบันหมายถึงจุดจบของบริษัทควอนตัมหรือไม่?