Markets await key macro report of the week – June CPI inflation data, which will be released tomorrow at 1:30 PM BST. The report will be closely monitored by investors, as inflation is currently a key factor in the Fed's decision-making process. This is confirmed by recent statements from FOMC members, including comments from Chairman Jerome Powell. Let's look at what markets and economists expect from today's release.

What does the market expect?

Market expectations indicate a slowdown in the main inflation measure and the core inflation to remain at the same level as the previous month. Consensus suggests that the headline rate will slow from 3.3% to 3.1% year-on-year, while the core rate will remain unchanged at 3.4%. A decline in headline inflation is obviously an important argument for the Fed, but on the other hand, expectations still indicate persistent core inflation. It is worth noting that readings from the beginning of the year to April were in line with expectations or higher, and the last reading for May showed a reversal of this trend and larger-than-expected declines. Recent weaker data from the labor market, ISM (price sub-index), and housing sector may give investors hope for another weaker reading.

The strength of the American labor market is weakening, along with spending on discretionary goods. Source: Bloomberg Financial LP

However, the range of economists' estimates in the Bloomberg survey does not entirely indicate this. Out of 44 surveyed, 68% of forecasts are in the range of 3.02-3.18% for headline inflation and 3.36-3.48% for core inflation. Expectations suggest a reading around the consensus, with no forecasts indicating a significant drop.

USA, CPI inflation report for June:

- Headline inflation (annual). Expectations: 3.1% y/y. Previously: 3.3% y/y

- Headline inflation (monthly). Expected: 0.1% m/m. Previously: 0.0% m/m

- Core inflation (annual). Expected: 3.4% y/y. Previously: 3.4% y/y

- Core inflation (monthly). Expected: 0.2% m/m. Previously: 0.2% m/m

Money market valuation over the last week has been revised towards faster cuts. Currently, swaps estimate that the FED will reduce interest rates by 25 basis points at the September meeting, with a 79% probability. At the beginning of July, it was 68%. These data will certainly be revised after tomorrow's CPI reading. Source: Bloomberg Financial LP

What is the Fed's stance?

Investors' hopes are supported by Jerome Powell's speech yesterday. Although the overall tone was received neutrally by the markets Powell did not explicitly rule out a September cut. The Fed wants to see confirmation of sustained downward momentum in inflation before making a key decision on a rate cut.

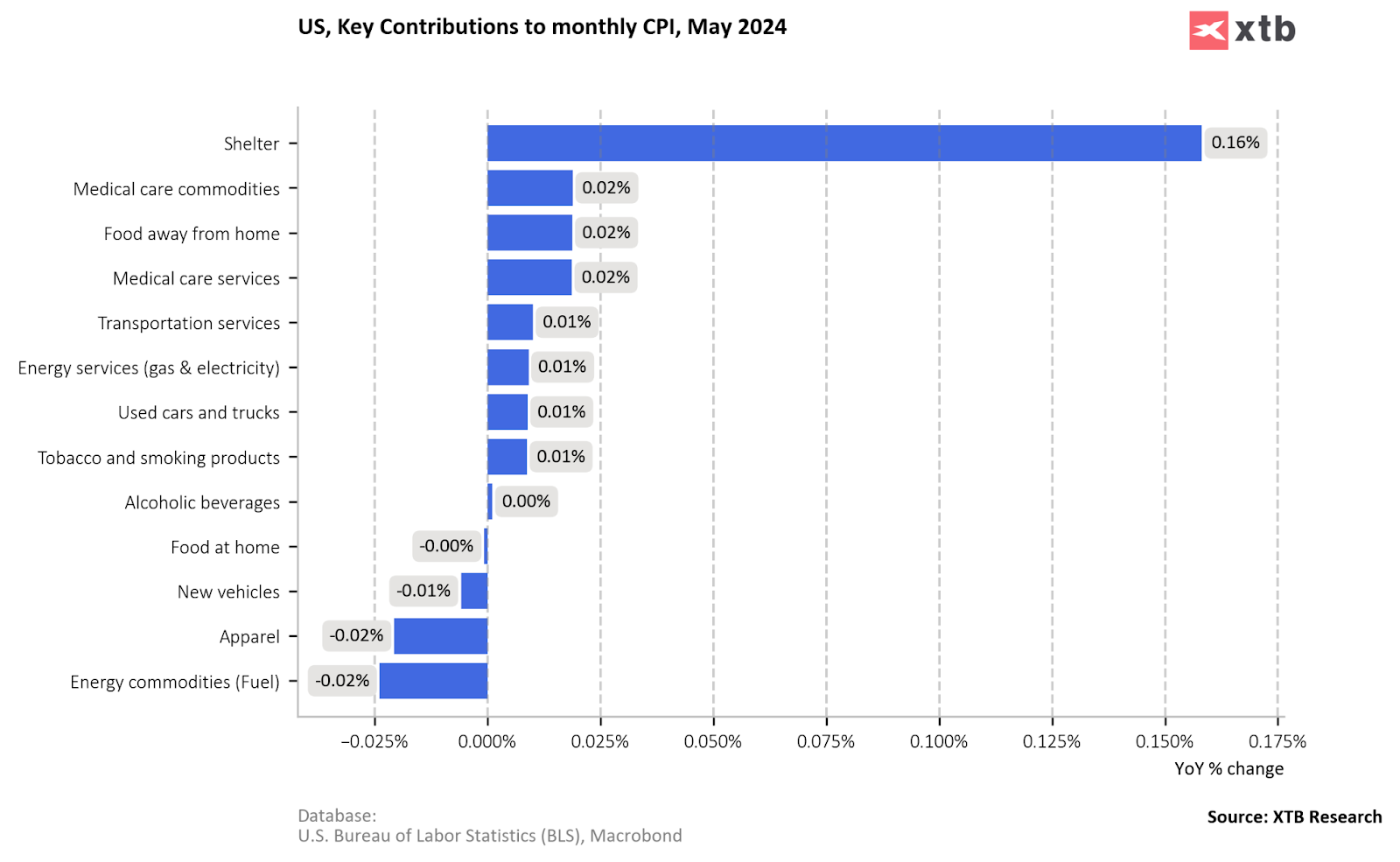

CPI data after a difficult first quarter of 2024 turned out to be exceptionally good in May. Most importantly, the monthly inflation growth rate was 0.0%. The strong decline was mainly driven by clothing, energy, car and food prices. On the other side, we can still see the shelter prices at the top.

What do the leading indicators say?

-

The fall in fuel prices will no longer contribute as much to the disinflationary process as in April and May. The energy sector may be more neutral.

-

Used car prices, after a strong fall in the first half of the year, are now at very low levels, which may limit their positive impact in the following months.

-

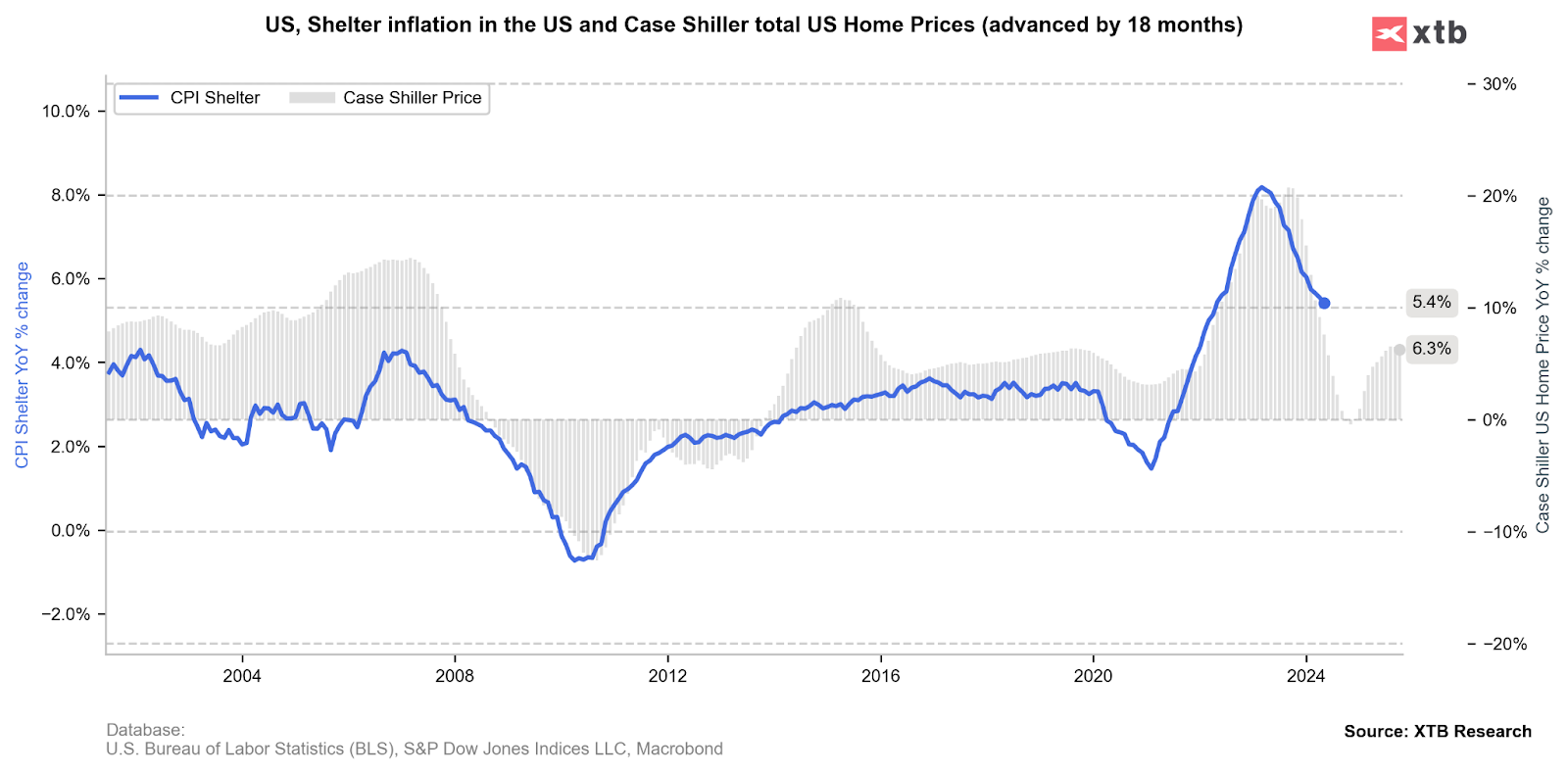

Shelter CPI is currently the largest contributor to CPI readings. In the coming months, we can expect price pressure to fall further before a potential rebound early next year.

It is the potential decline in shelter price in the coming months that could provide the perfect window for the Fed to make its first rate cuts. It may be too late for such a narrative by the end of the year, when rental housing prices will hit again.

EURUSD (D1)

The EURUSD pair broke out above an important resistance structure defined by the 50-, 100- and 200-day EMAs (blue, purple and gold curves on the chart, respectively). At the moment, this zone can be regarded as a major support point as we would observe a rebound in the dollar. The main point of resistance could now be the zone around 1.0863, where the 23.6% Fibo elimination of the upward channel initiated in 2022 runs. Source: xStation

Daily Summary - Powerful NFP report could delay Fed rate cuts

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

BREAKING: US100 jumps amid stronger than expected US NFP report

Market wrap: Oil gains amid US - Iran tensions 📈 European indices muted before US NFP report