-

Bad news is still good news, which means that markets still anticipate a soft landing scenario. After yesterday's worse Job Opening data report markets ended the session with solid gains.

-

The S&P 500 was up by 1,45% and Nasdaq 100 by 2,15% both approaching the crucial support levels.

-

Indices from Asia-Pacific traded mostly higher today. Nikkei gained 0.51%, S&P/ASX 200 added 1.2%, Kospi and Nifty 50 jumped by 0.5%.

-

Indices from China traded 0.2-0.3% higher after yesterday's strong gains, awaiting mortgage rate cuts in China.

-

Beijing reportedly plans to cut interest rates on some ¥38.6 trillion of existing mortgages.

-

US job openings decrease to 8.83 million, a more than two-year low, indicating reduced labor demand.

-

Consumer confidence in the U.S. declines due to worsening job outlooks and persistent inflation.

-

Japanese Consumer Confidence is at 36.2, slightly below the forecast of 37.4.

-

Australian CPI YoY is at 4.9%, lower than the forecast of 5.2% and the previous 5.5%.

-

Toyota is optimistic on economic growth, plans a 10% global output increase and a 26% domestic production increase for Sep-Nov quarter.

-

Bank of Japan board member Naoki Tamura anticipates sustained achievement of the 2% inflation target and advocates for keeping easy policy due to uncertainty. Ending negative rates, yield curve control are options in case BOJ were to exit easy policy but timing of easy policy exit must not be too late, but not too early too.

-

Morgan Stanley’s Analyst expects a strong rally in U.S. stocks, with the S&P 500 approaching 5,000 by year-end.

-

Today, USD is one of the strongest currencies among major economies, while the Japanese Yen is on the other end. USDJPY is trading 0.21% higher today.

-

Cryptocurrency market enjoys gains after US court ruled in favor of Grayscale and reccomended the SEC to reconsider Grayscle BTC spot ETH application again; Grayscale Bitcoin Trust was up by 17%, and Bitcoin was gaining 7%.

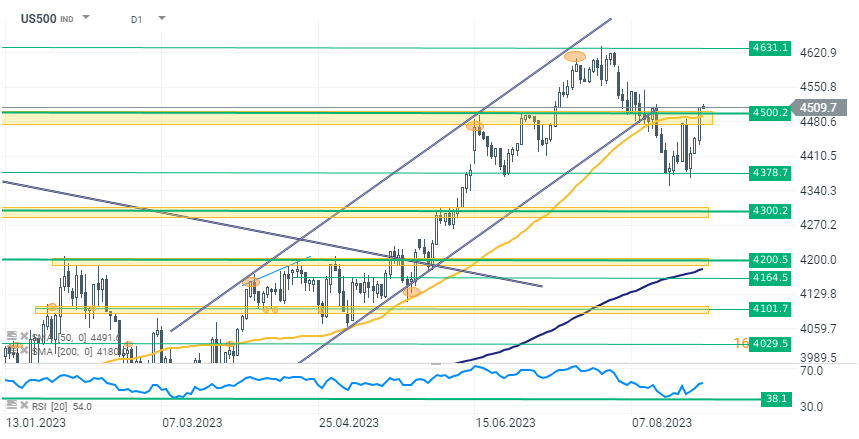

The US500 index has returned above the key support line at 4500 points after yesterday's dynamic increases. The Jolts data on new job openings turned out to be much worse, which led to euphoria in risky assets in anticipation of the end of the rate hike cycle.

The US500 index has returned above the key support line at 4500 points after yesterday's dynamic increases. The Jolts data on new job openings turned out to be much worse, which led to euphoria in risky assets in anticipation of the end of the rate hike cycle.

Daily summary: Silver plunges 9% 🚨Indices, crypto and precious metals under pressure

US100 loses 1.5% 📉

US Open: Cisco Systems slides 10% after earnings 📉 Mixed sentiments on Wall Street

BREAKING: US jobless claims slightly higher than expected