- Thursday's session in APAC markets once again came under pressure from rising US debt yields (currently at 4.6%). Japan's Nikkei lost nearly 1.3%, the Hang Seng is down 1.5% and the Nifty 50 is losing 0.67%.

- The sell-off in Asian markets is also a reaction to the lower close of yesterday's session on Wall Street, which also reacted to changes in debt markets. The S&P500 index lost 0.74% yesterday, the Nasdaq technology index lost 0.58% and the Russell 2000, which depicts the state of smaller-cap stocks, was down by up to 1.7%.

- European equity futures point to a lower opening for the Euro Stoxx 50 benchmark.

- Looking ahead, highlights of the day include: Spanish CPI, Swiss GDP, Eurozone sentiment, Eurozone unemployment rate, second estimate of US GDP, US PCE report (q/q).

- Among others, Best Buy (BBY.US) and Dollar General (DG.US) will present their quarterly results today.

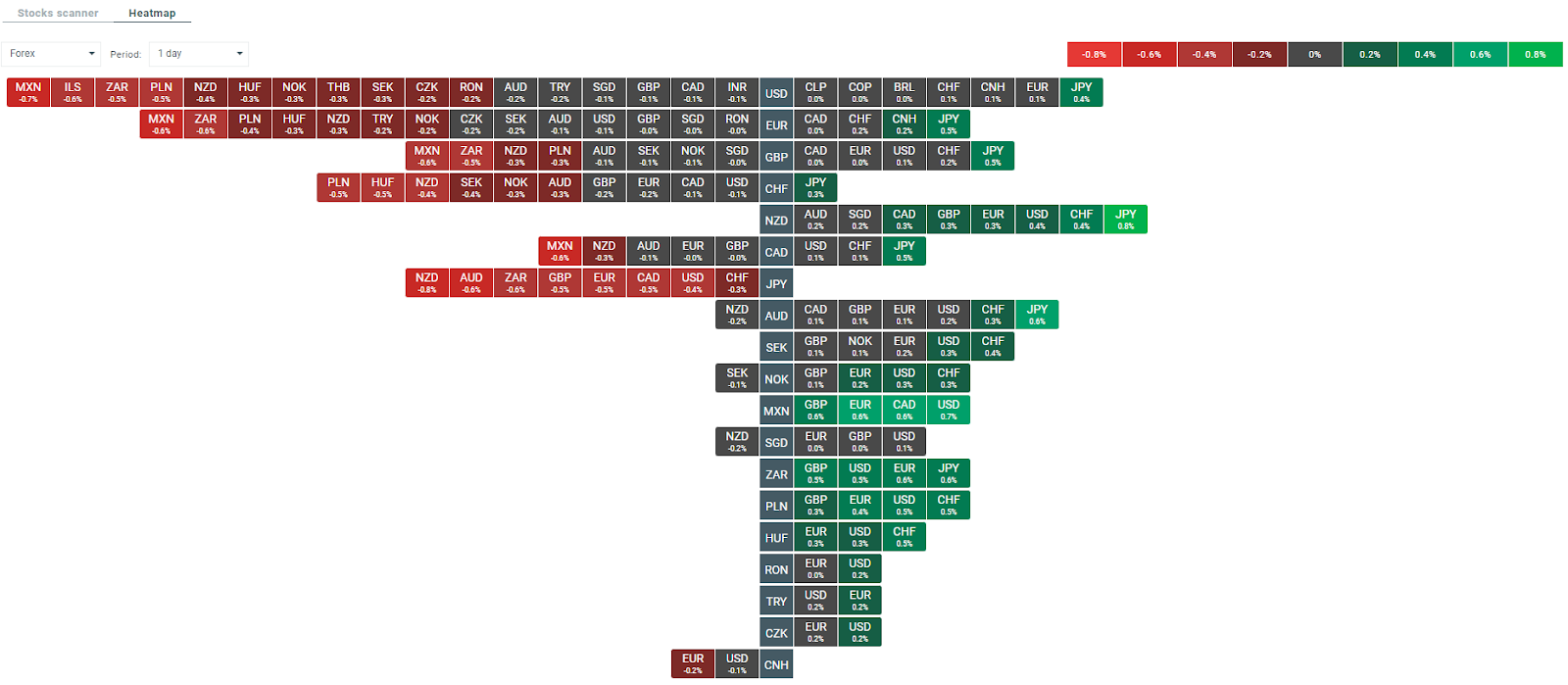

- In the FX market, the Japanese yen is currently performing best. The rest of the currencies are recording mixed levels or losses. The largest of these are currently being seen on Antipodean currencies.

- The SNB's Jordan said that a weaker Swiss franc is now the most likely source of higher Swiss inflation and added that the Bank could counter this by ‘selling foreign currencies’.

- In the precious metals market, we are already seeing increased volatility early in the day in Europe. Silver-based contracts are trading close to 1.75% down, while palladium is already losing close to 2.1%.

- Yesterday, the US private oil inventory survey (API) report came out and showed a huge drop (6.49 million barrels) well above the expected drop of 2 million.

- In the crypto market, sentiment is relatively mixed, with a slight tilt towards the downside. Bitcoin gains 0.3%, while Ethereum retreats 0.5%.

Heatmap of FX market volatility at the moment. Source: xStation

Economic Calendar: All at once! Fed rate decision and Big Tech earnings to stretch investors (29.07.2026)

Chart of the Day: Who suffers from the oil price drop? (28.07.2026)

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)