-

Asia-Pacific indices traded mostly lower during Friday’s trading session. Japan's Nikkei lost close to 0.52%, Australia's S&P/ASX 200 traded 0.20% lower and Chinese futures traded 0.2% higher.

-

Asian markets showed volatility on Friday due to weak US tech earnings, robust labor market signs that could push for another 2023 rate hike.

-

Major Asian indices traded mostly flat, Japan and China stocks fluctuated. MSCI Asia Pacific Index dropped for the fifth consecutive day. US equity contracts traded in a tight range post Nasdaq 100's first drop in over five months on Thursday.

-

US market declines potentially disrupting this year's massive gains with S&P 500 up by 18% and Nasdaq 100 by 41%, amidst a frail economic outlook and Federal Reserve's tough tightening moves.

-

Chinese investors are on the lookout for further government support measures.

-

More cautious and balanced policy actions could extend decision-making timelines, possibly exerting additional pressure on corporate profits for the next two quarters.

-

Offshore yuan saw little change on Friday post a higher-than-expected fixing by PBoC. Yuan rose Thursday after increased central bank support.

-

The AI boom prompts index rebalancing effective July 24, potentially reducing the weights of Amazon, Nvidia, Microsoft stocks, thereby possibly exerting downward pressure due to passive fund adjustments.

-

Japanese CPI Nationwide Actual stands at 3.3%, against the forecast of 3.2% and previous 3.2%.

-

Japanese Core CPI Nationwide YoY Actual remains steady at 3.3%, in line with the forecast, slightly up from the previous 3.2%.

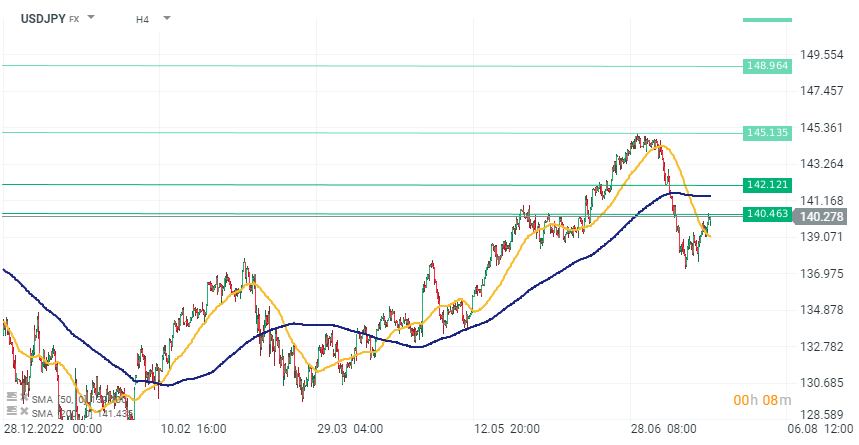

USDJPY is again trading around 140 points. After today's higher inflation reading, the Japanese currency does not seem to react significantly. Despite the higher than expected inflation, which increases the chances of any action from the Bank of Japan (BoJ).

USDJPY is again trading around 140 points. After today's higher inflation reading, the Japanese currency does not seem to react significantly. Despite the higher than expected inflation, which increases the chances of any action from the Bank of Japan (BoJ).

Morning Wrap: Dollar in a trap, all eyes on NFP 🏛️(February 11, 2026)

Daily summary: Weak US data drags markets down, precious metals under pressure again!

BREAKING: US RETAIL SALES BELOW EXPECTATIONS

Economic calendar: Indices and EURUSD await US retail sales report