-

Tuesday's session on Wall Street saw declines in US indices. The Nasdaq lost 1.14% and the S&P500 fell 1.16%, closing the session below its 50-day EMA.

-

Asia-Pacific (APAC) markets traded in a weaker mood today, mimicking the momentum of yesterday's US session. Japan's Nikkei 225 is currently losing nearly 1.22%, the Hang Seng index is subtracting more than 1.36% and Korea's KOSPI is down 1.65%.

-

Futures based on the German DAX and the European benchmark Eurostoxx point to a lower opening in today's European cash session.

-

The RBNZ kept interest rates unchanged as expected and reiterated that the OCR rate will need to remain restrictive for the foreseeable future.

-

Zhongrong International Trust Co. has missed payments on dozens of products and has no immediate plan to repay customers, indicating that the troubles of the US$138 billion-plus Chinese financial giant are more serious than previously expected. The corporation has short-term liquidity problems.

-

Tesla is slashing prices for the Model S and Model X in the Chinese market. Yesterday, a similar decision was made for the Y models.

-

JP Morgan has lowered its forecast for China's 2023 GDP after weak macro data this week. The new expectation is +4.8% compared to the last forecast published in May of 6.4%.

-

Wells Fargo forecasts a rise in US inflation in the second half of 2023, which is expected to encourage the FOMC to raise interest rates further

-

Data from Australia - the twelfth consecutive negative reading of the momentum of the leading indicators index.

-

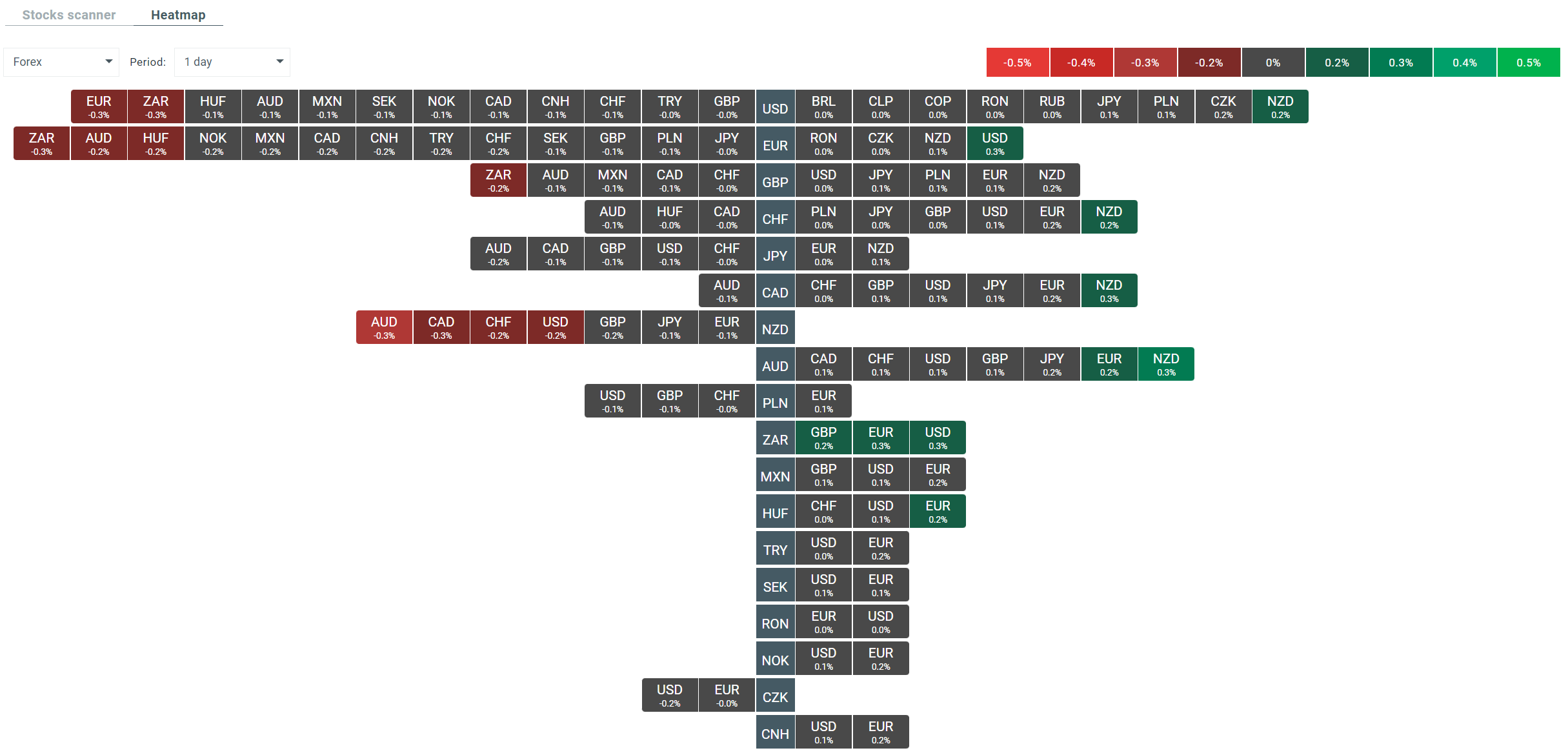

In the FX market, we are currently seeing mild gains in EURUSD, however, the USDIDX index remains above the 103.00 zone. The New Zealand dollar is currently seeing the biggest gains in the broad market, while the Australian dollar is under pressure.

-

Data from the API private oil inventory survey shows a much larger decline in oil stocks than expected. On the other hand, the start of the European session brings declines in energy commodities, with WTI crude oil losing nearly 0.6%.

-

Bitcoin and gold are trading close to important support levels, the $29 000 and $1 900 barriers respectively.

-

The most important macro readings of the day will be the UK inflation report, the GDP and unemployment rate readings in the euro area, as well as the FOMC Minutes

Heatmap showing current volatility in the FX market and specific currency pairs. Source: xStation 5

Economic calendar: NFP data and US oil inventory report 💡

Morning Wrap: Dollar in a trap, all eyes on NFP 🏛️(February 11, 2026)

BREAKING: US RETAIL SALES BELOW EXPECTATIONS

Economic calendar: Indices and EURUSD await US retail sales report