Summary:

-

Consumer and producer inflation gauges in the UK expected to decline

-

Market consensus points for a drop in the oil inventories

-

Central Bank of Brazil viewed to stay on hold

On Wednesday the British pound may attract increased attention. Not only a breakthrough in Brexit talks may be looming but also an inflation report will be released. Moreover, investors will be served the US housing market data that may lift USD after it was hit overnight. It is also worth to mention that the Central Bank of Brazil will announce its interest rate decision at 10:00 pm BST. The Bank is expected to leave the selic (overnight) rate unchanged at 6.50% what would be reasonable given that in two weeks Brazilians will go to polling stations to elect new president. As no candidate is currently viewed as favourite the central bankers may stay on hold until situation is more clear.

Start investing today or test a free demo

Open real account TRY DEMO Download mobile app Download mobile app9:30 am BST - UK, Inflation report for August. The Bank of England has announced earlier that it will stay on hold until the manner in which the United Kingdom will break away from the European Union is more clear. As PM Theresa May said yesterday that the withdrawal deal is “virtually agreed” the economic data from the UK may become more closely watched. Today’s inflation report is expected to show CPI inflation decelerating from 2.5% YoY to 2.4% YoY. The core gauge is seen to move lower to 1.8% YoY (1.9% previously). Apart from that, all PPI inflation gauges are expected to move lower as well.

1:30 pm BST - US, Housing market data for August. The US housing market remains strong. However, the two latest housing starts readings came in noticeably lower than what we saw in the first half of the year. Nevertheless, market consensus points for a rebound in August to 1235k. Moreover, the housing permits data will be released simultaneously. When it comes to this gauge a reading of 1310k is expected what is more or less inline with prints we saw earlier this year. Do notice that as Fed is rising interest rates the mortgages may eventually become more expensive and the growth in the US housing market may slow.

3:30 pm BST - DOE report on oil inventories. Despite API data showing a moderate build in the oil stocks yesterday crude prices moved higher. As a reason behind this one can name comments from one of the major producers. Namely, Saudi Arabia said it is comfortable with Brent prices breaking above the $80 handle what lifted prices of both Brent and WTI yesterday. Today’s DOE report is expected to show 2.4 mb drop in the oil stocks (API showed 1.25 mb build). Apart from that, distillate inventories are seen to rise just 0.2 mb after last week’s 6.2mb build. Gasoline stocks are expected to fall 0.5 mb.

Central bank speakers scheduled for today:

-

9:00 am BST - BoE’s Haldane

-

1:00 pm BST - Riksbank’s Ohlsson

-

2:00 pm BST - ECB President Draghi

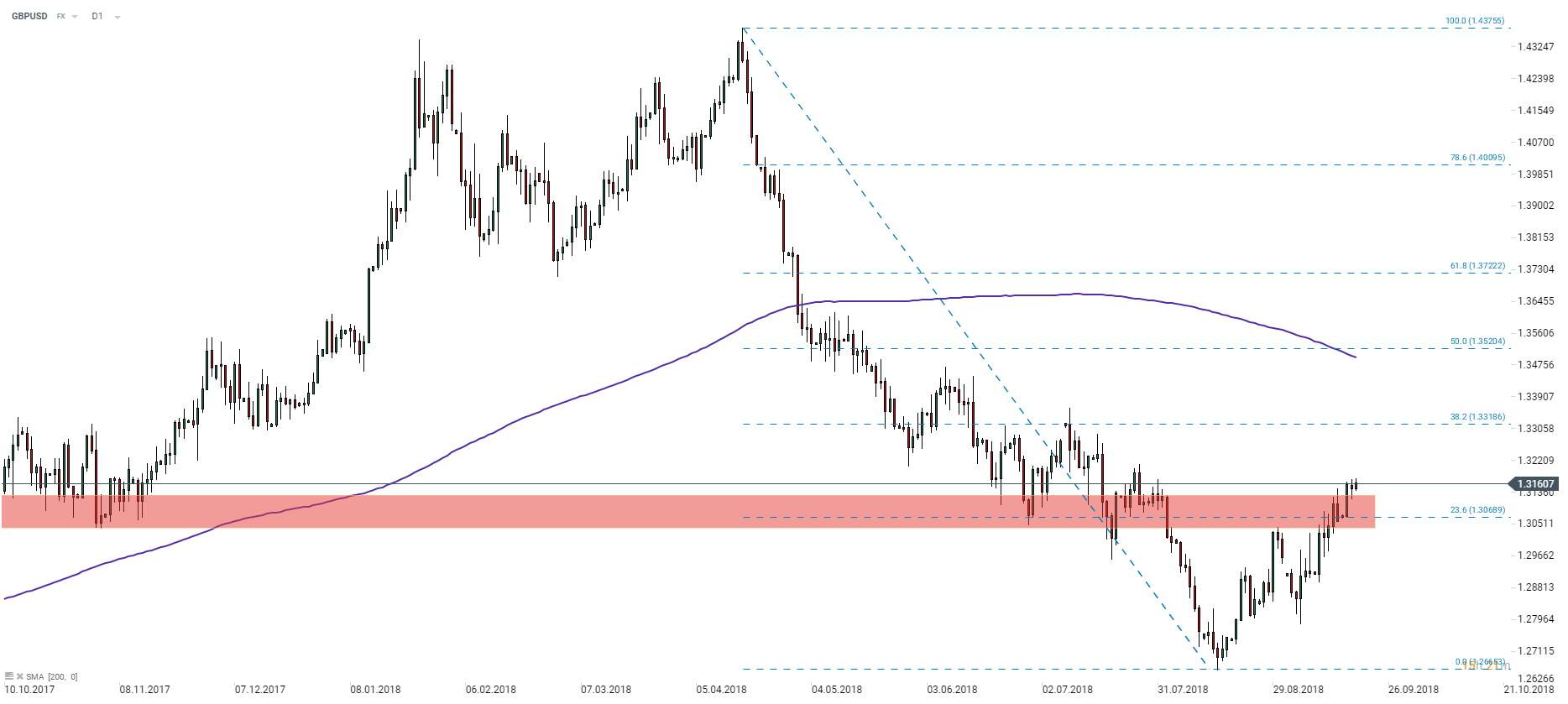

GBPUSD finally managed to break above the resistance zone ranging around the 23.6% Fibo level of the last major downward impulse. However, as the pair stays just a notch above it, a weaker-than-expected inflation report may push the exchange rate back into the zone. Source: xStation5

GBPUSD finally managed to break above the resistance zone ranging around the 23.6% Fibo level of the last major downward impulse. However, as the pair stays just a notch above it, a weaker-than-expected inflation report may push the exchange rate back into the zone. Source: xStation5