In the third quarter of 2024, China has taken center stage among investors due to a significant shift in the economic policy of the Communist Party of China. The announced or already implemented stimulus packages for the world’s second-largest economy have heated up global markets, with local indices and individual companies showing impressive gains.

However, the Chinese economy faces a period of elevated uncertainty. The return of Donald Trump to the White House, combined with the likely Republican majority in Congress, foreshadows an intensified trade war between China and the United States. According to analysts, Trump 2.0 will be particularly unpredictable, along with the potential scale of his protectionist policies.

Relations between the president-elect and Xi Jinping are currently highly ambivalent, with recent exchanges of “courtesies” between the leaders resembling the calm before the storm. China’s economic climate is far less favorable than during Trump’s first term, and the looming threat of 60% tariffs on Chinese exports has raised market expectations for further stimulus packages to help mitigate the effects of an impending trade war.

Can we, however, expect that after years of stagnation in the Chinese market, the Middle Kingdom will stay the course toward its targeted economic growth rate? Will the implemented packages reshape the Chinese market and attract a renewed inflow of foreign capital, or will they merely serve as a cautious response to new risk factors?

Origins of China’s struggles

China’s current economic challenges - stagnation risk, a collapse in the real estate market, and a lack of incentives for discretionary consumption - are largely a consequence of the country’s pandemic-era policies. The strict "zero COVID policy", aimed at drastically halting the spread of the virus, has had a prolonged (and still visible) impact on spending by both Chinese consumers and businesses. This economic slowdown has led to deflationary pressures, creating a cycle of restrained spending and investment, and an overall stagnation in the Chinese economy. The unfavorable economic climate has weakened global capital’s confidence in China, while insufficient risk premiums have fueled an outflow of capital from the country.

What changed over Q3 2024?

At the end of September, China’s central bank announced the most advanced stimulus program since the pandemic, lowering external financing costs to boost the weakening real estate market. The support also included loans for large-scale share buybacks by companies listed on the Chinese stock exchange. This liquidity injection propelled domestic stocks, pushing the CSI 300 and Hong Kong’s Hang Seng indices into bull market territory. Optimism extended to companies with significant exposure to the Chinese market, including major European luxury brands.

Nothing lasts forever

The intense enthusiasm, however, was short-lived, as questions and doubts surfaced regarding the Chinese government’s future plans. Since early October, Chinese stocks have faced significant losses, with the CSI 300 index falling by 7% from its recent peak—the largest single-day drop since 2020. For now, the market remains unconvinced of the long-term impact of the implemented measures. The tangible effects of these solutions will take time to materialize, and investors' attention is focused on macroeconomic data and the evolving trade dynamics with the United States.

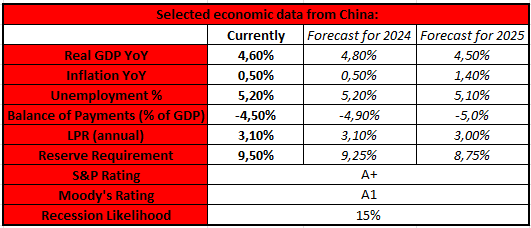

Key economic indicators and their forecasts

Source: XTB Research, Bloomberg Financial LP

Currently, the economic conditions in China are considered mixed. Low inflation points to the weakness of the domestic consumer, despite the local government not holding back on spending to stimulate the economy. China’s credit ratings are classified as positive, although forecasts are already turning negative (mainly due to high debt levels and the weak real estate market). Bloomberg’s forecasting model suggests that there is a 15% probability that China will enter a recession within the next 12 months

Inflation and domestic demand

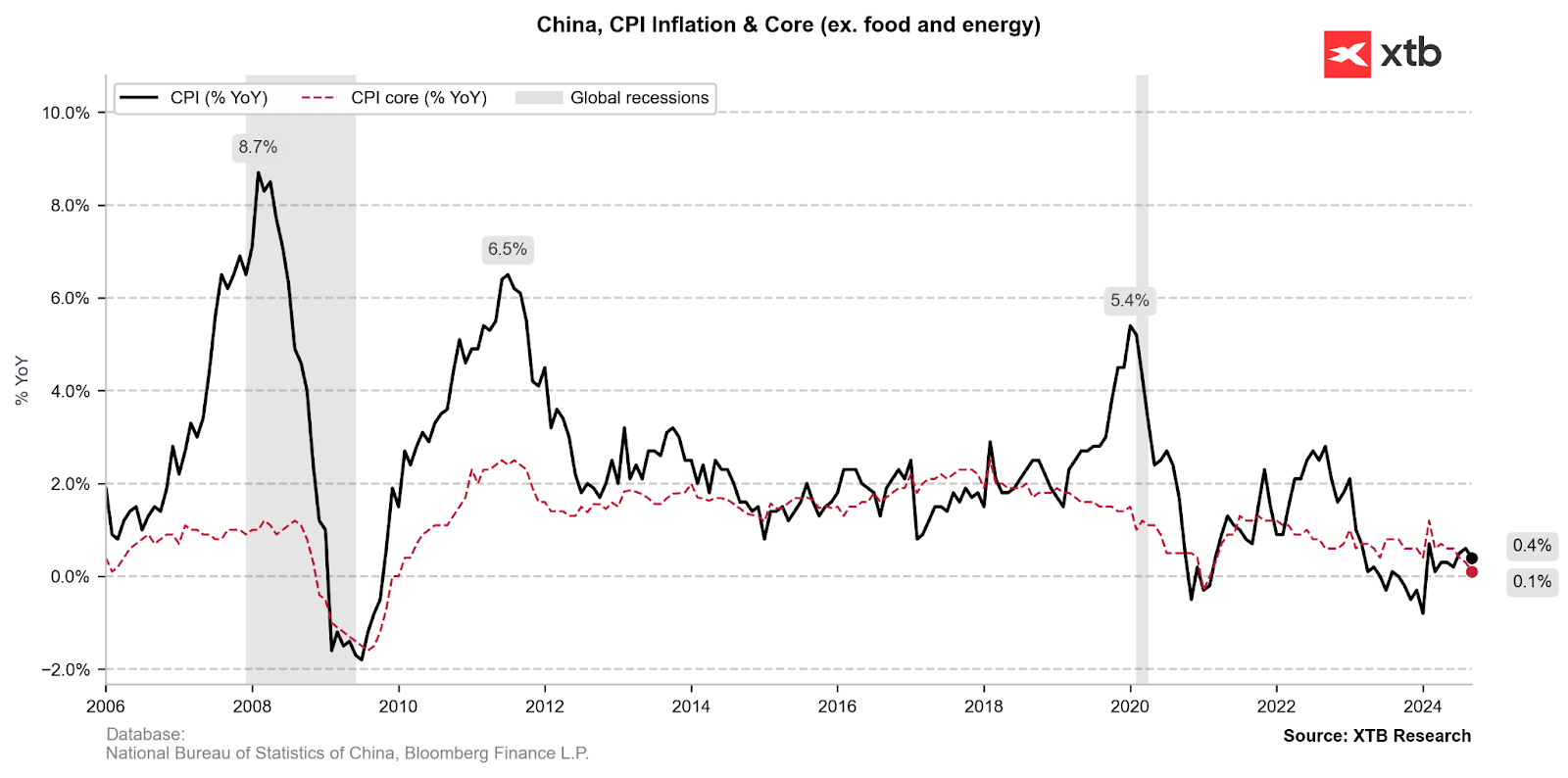

The plans to achieve the set growth targets for the Chinese economy were severely tested in mid-2023, when China entered a period of deflation. For nearly six months, the country faced the pressure of falling prices, which effectively demotivated the already problematic domestic demand. The deflationary period ended at the beginning of 2024, reflecting the delayed effect of the summer interest rate cuts. However, inflation is still far from the target of the People’s Bank of China (PBOC), set around 3%.

Source: XTB Research, Bloomberg Financial LP

Deflationary pressure in China is a consequence of exceptionally weak consumer demand, which has been unable to recover and return to pre-pandemic levels. The Chinese consumer confidence index has been hovering at historically low levels for nearly two years, and the share of consumption in China’s GDP is significantly lower than the global average, according to World Bank data (53% vs. 75%). Yet, the Chinese government has largely excluded consumers from its stimulus packages. China’s transfer policy in the 21st century primarily supports investments in industry and the real estate sector, to the detriment of Chinese households, which are burdened with high housing costs and slow wage growth. The dynamics of food prices remain unfavorable as well: inflation in food products has disproportionately surpassed both the CPI and core inflation (3.3%).

Source: XTB Research, Bloomberg Financial LP

Real estate market

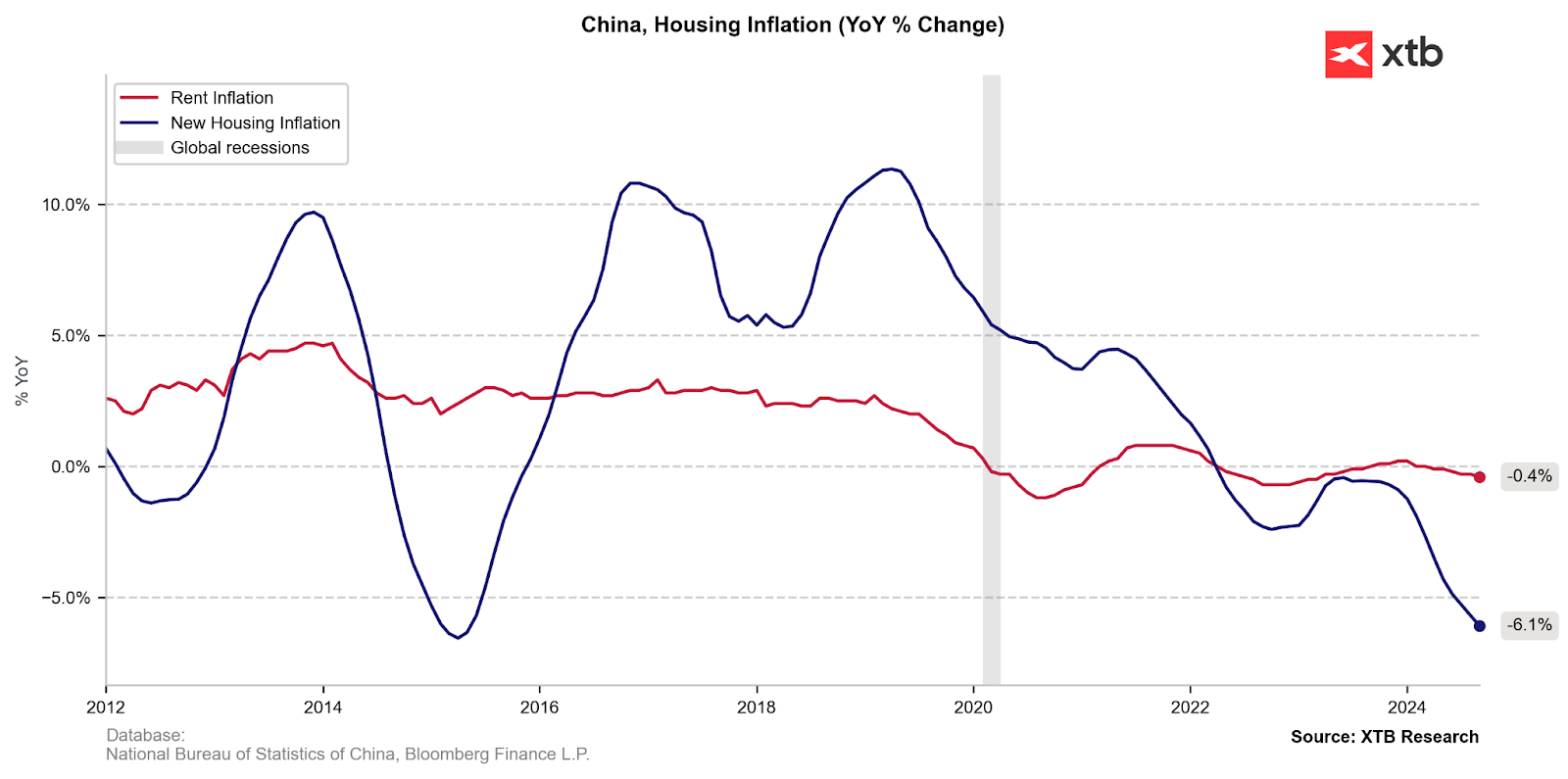

China's economic outlook is currently under pressure due to the weak real estate sector, which reflects broader issues such as unfavorable demographics, high youth unemployment, and weakening demand.

Cheap credit for developers and the requirement of a 100% down payment before starting residential construction projects drove China’s real estate market in the 21st century to the point where its share in GDP began approaching 30%. Fearing the speculative nature of the sector, the Chinese government introduced in 2020 debt criteria for developers wishing to take out further loans. As a result of this new policy, half of China’s developers lost access to liquidity, many projects were halted, and the country’s landscape became filled with ghost cities full of unfinished skyscrapers.

Source: XTB Research, Bloomberg Financial LP

However, the slowdown in supply has not led to further price increases, as the effect of even weaker demand prevailed. The shrinking population since 2022, rising youth unemployment (18.8% in August), and the slowdown in urbanization are among the key reasons for the ongoing collapse in housing prices in China.

The recently announced government support for the sector in the form of 4 trillion yuan to finalize halted projects does little to ease concerns about the future dynamics of the real estate market. The price collapse still hasn’t translated into increased demand but has affected the sentiment of those for whom housing constitutes a significant part of their wealth, thus weakening their willingness to spend money.

Monetary policy

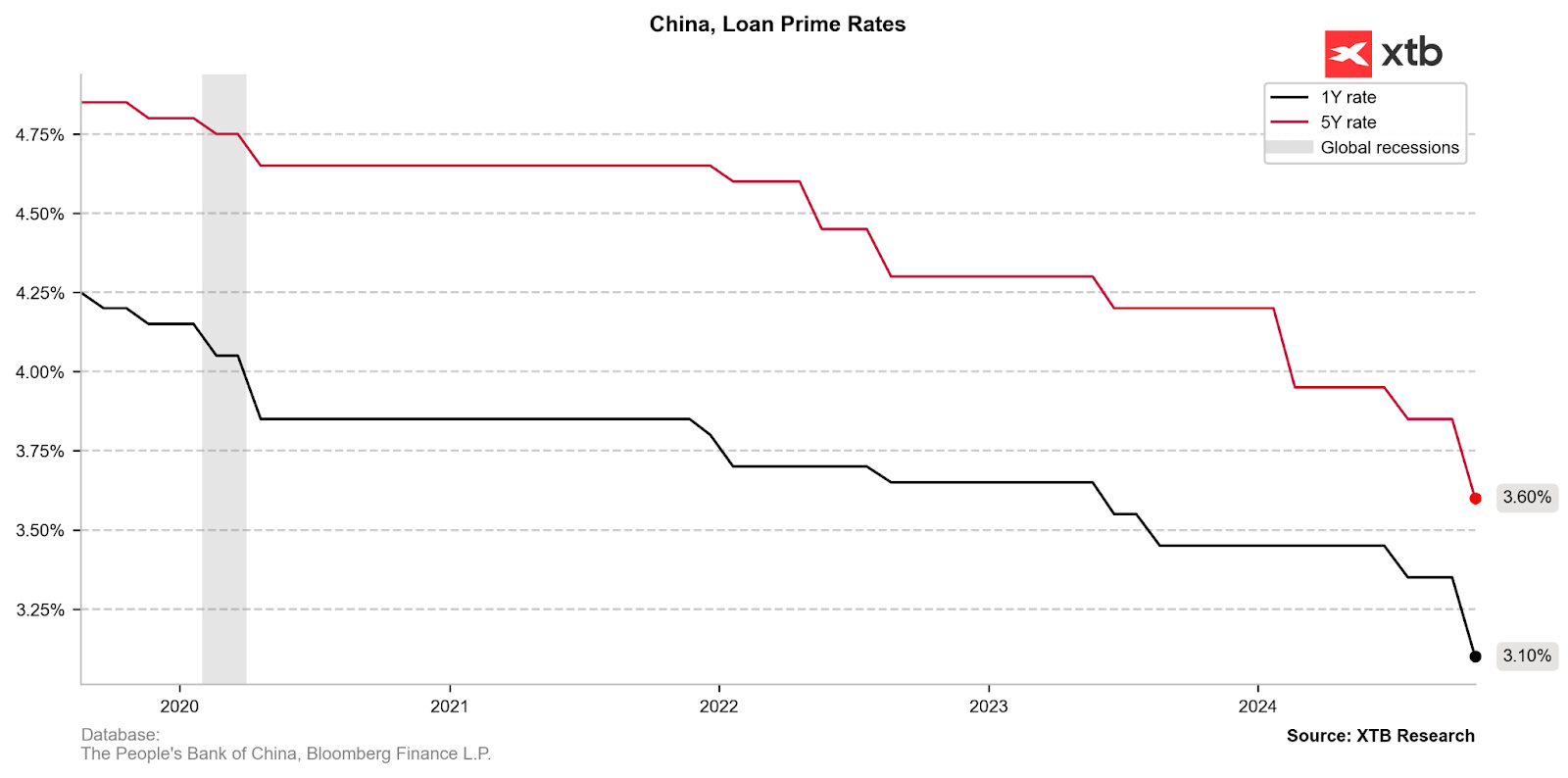

At the September meeting of the Politburo, China’s top leaders called for significant interest rate cuts and measures to prevent further declines in the real estate market, marking their strongest pledge yet to stabilize this key sector. Larger-than-expected cuts in the Loan Prime Rate (LPR) are expected to help stabilize the real estate market in the near term.

What do these rates influence? Most new and outstanding loans in China are based on the one-year LPR, while the five-year rate affects mortgage rates and other long-term loans. Last week, China’s largest state-owned lenders reduced deposit interest rates to offset the impact of lower loan rates on their shrinking margins.

Source: XTB Research, Bloomberg Financial LP

On October 21, the one-year interest rate was reduced to 3.10% from 3.35%, while the five-year LPR was lowered to 3.60% from 3.85%. The People's Bank of China is cutting interest rates to strengthen the weakening economy. However, the actual effect of these changes will still take time to materialize.

Stock market catches the lifebuoy

The Chinese central bank’s program aimed at financing loans for share buybacks has provided immediate support for stock prices, as evidenced by the scale of recent gains in Chinese indices. So far, nearly 50 companies have applied for a special credit line, which could total over $45 billion.

CHN.cash - will it regain its footing?

The picture of the Chinese market has clearly changed from the stagnation observed in 2021-2023. While it might seem that such a large scale of growth is more a result of hedge funds closing short positions, the already implemented stimulus measures have laid the first foundations for a massive economic recovery program in China.

What does this mean for the CHN.cash index? The scale of the implemented measures seems to significantly reduce the scenario of a decline to levels observed before the first reports of economic changes. However, it is also possible that profit-taking could occur after the sharp rally. At this point, it seems that the key factor defining future price movements will be whether: 1) The PBOC introduces new stimulus measures, and 2) These decisions result in Chinese companies generating higher revenues and profits. Currently, the second element remains highly uncertain.

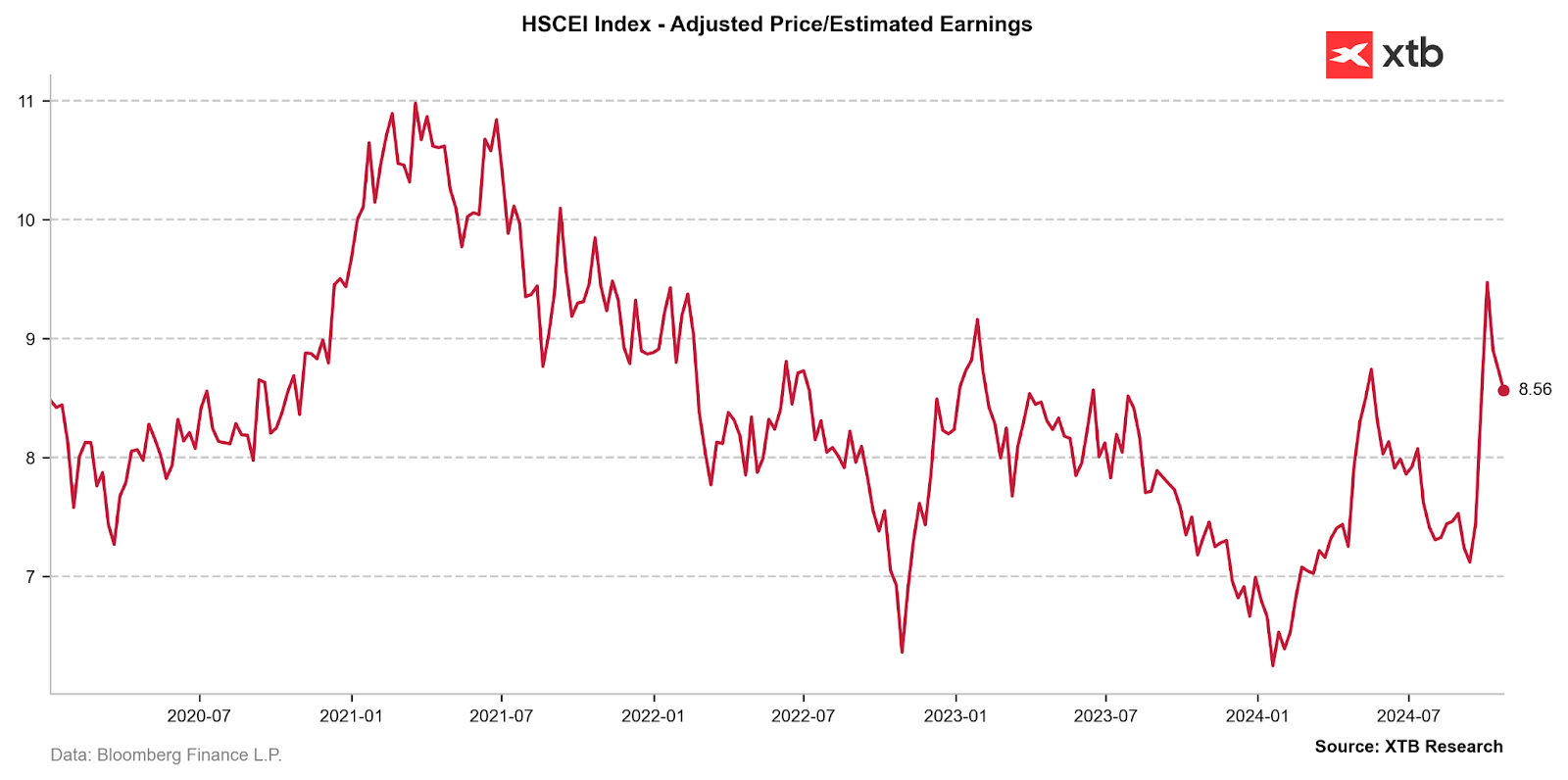

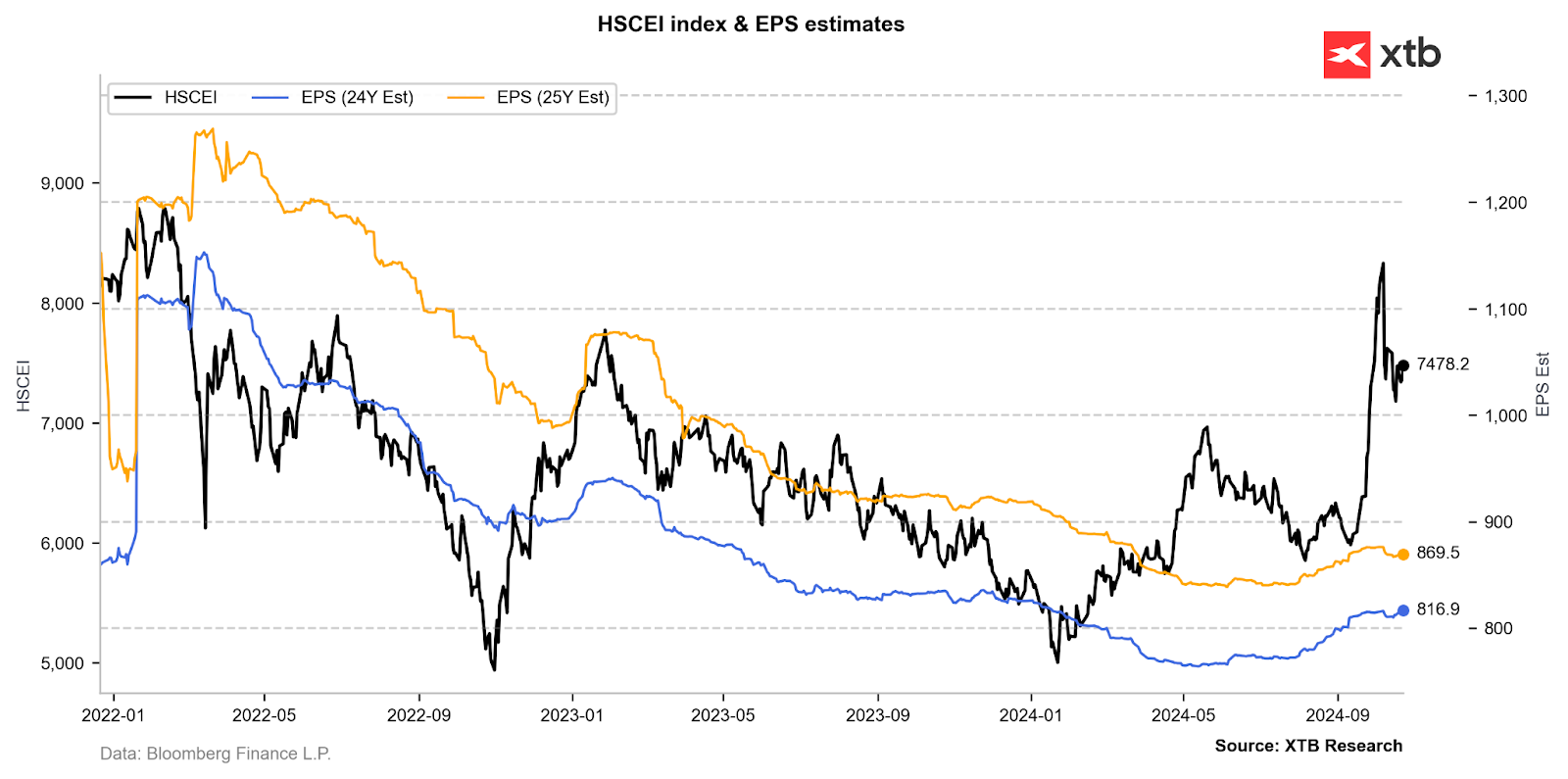

Currently, the valuation of the HSCEI index, represented by the CHN.cash contract, indicates trading at the 5-year average for the price-to-earnings ratio estimated for the next 12 months. Source: XTB Research, Bloomberg Financial LP

However, the aforementioned valuation is largely due to the price jump observed in September. The revision of the average EPS growth for the companies included in the HSCEI index was not large enough to significantly widen the risk premium currently present on the index. Source: XTB Research, Bloomberg Financial LP

CHN.cash halted its gains around the 50% retracement of the downward channel that began in February 2021, after which the distribution phase started. At this point, the instrument is holding near the peaks from May of this year, which, along with the 50-day exponential moving average, form key support structures for the recent rally. The market is awaiting further decisions from the Chinese establishment. Source: xStation5

Summary

China faces a series of internal challenges that may intensify with Donald Trump's return to the White House. The dynamic growth in exports in recent months has helped mitigate the effects of weak domestic demand, which is failing to meet the economic growth targets set by the Chinese Communist Party. The already heated stock market may therefore raise its expectations for further stimulus packages aimed at sustaining the normalization of economic conditions in the face of reduced foreign trade. However, it is the time required for the effects of the implemented fiscal and monetary policies to manifest in macroeconomic data that matters the most to both investors and policy makers.

XTB HQ

Daily Summary - Powerful NFP report could delay Fed rate cuts

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

BREAKING: US100 jumps amid stronger than expected US NFP report

Market wrap: Oil gains amid US - Iran tensions 📈 European indices muted before US NFP report