The US Dollar Index faces a critical juncture ahead of Wednesday's CPI data, with market expectations tilted toward persistent inflation pressures potentially delaying anticipated Fed rate cuts. Core inflation remains stubbornly elevated, while political transition adds new layers of uncertainty to the dollar's trajectory.

Key Market Statistics:

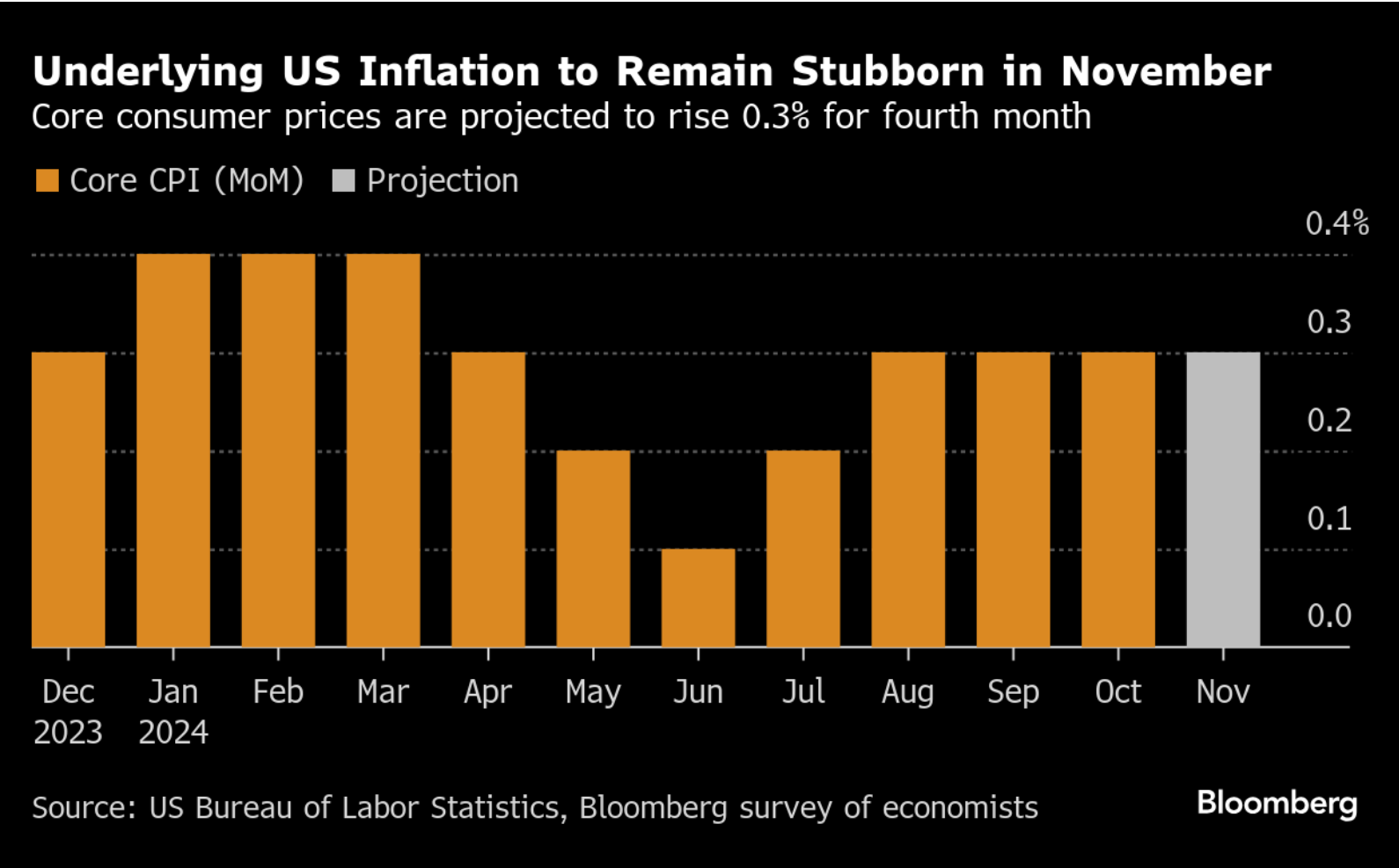

- Core CPI expected at 0.3% MoM for November, marking fourth consecutive month of firm readings

- Market-implied probability of December rate cut declining as inflation concerns mount

- Dollar finds technical support as Treasury yields maintain 4% floor across key tenors

The dollar's near-term direction hinges critically on Wednesday's inflation report, with forecasters anticipating another month of sticky price pressures. The core consumer price index, excluding food and energy, is projected to maintain its 0.3% monthly pace, suggesting the Federal Reserve's path to its 2% target remains challenging.

Core CPI forecast. Source: Bloomberg

Notable inflationary pressures persist across several sectors, with used car prices expected to rise 1.2% in November, following a 2.7% increase in the previous month. Housing costs continue to show limited signs of meaningful deceleration, with Owner's Equivalent Rent projected to increase between 0.3% and 0.4%, maintaining its above-pre-pandemic pace.

The technical picture shows increased caution among institutional investors, with recent flow data revealing significant duration reduction and selling of long-dated securities by mutual funds. This positioning adjustment, combined with year-end portfolio rebalancing, suggests heightened potential for market volatility.

Market Implied Rate Cuts. Source: Bloomberg

Looking ahead, market attention remains firmly focused on today's CPI release and its implications for Fed policy. While traders still largely anticipate rate cuts in the coming months, the persistence of elevated core inflation readings may prompt a more gradual approach to monetary policy easing than currently priced.

The political transition adds another layer of complexity to the dollar outlook, with proposed policies including potential tariffs and tax cuts potentially creating new inflationary pressures. Some businesses are already adjusting pricing strategies in anticipation of these policy shifts, potentially complicating the Fed's inflation-fighting efforts.

The market's overwhelmingly dovish positioning creates potential for significant dollar movement if inflation data surprises to the upside. Deutsche Bank economists note that while a December rate cut remains possible, the Fed's messaging is likely to emphasize a more gradual pace of easing going forward, particularly if inflation continues to show resistance to monetary tightening.

As we approach year-end, the interplay between persistent inflation pressures, potential policy shifts, and market positioning suggests the dollar may face increased volatility. Wells Fargo projects the journey to the Fed's 2% inflation target could extend through 2026, with limited progress expected in the year ahead.

USDIDX (D1 interval)

The US Dollar Index is currently trading above the 38.2% Fibonacci retracement level. A break below this level could lead to a retest of the July highs at 105.728. Conversely, bulls are targeting the 23.6% Fibonacci retracement level as the next resistance, with an eye toward an all-time high (ATH) retest.

The RSI is beginning to trend higher, signaling potential bullish divergence, which suggests strengthening momentum. Meanwhile, the MACD is tightening, indicating a likely crossover that could confirm bullish momentum in the coming sessions. These factors position the index at a pivotal point, with critical levels acting as decision markers for its next move. Source: xStation

Daily Summary - Powerful NFP report could delay Fed rate cuts

BREAKING: US100 jumps amid stronger than expected US NFP report

Economic calendar: NFP data and US oil inventory report 💡

Morning Wrap: Dollar in a trap, all eyes on NFP 🏛️(February 11, 2026)