The global economy has not entered a recession, and consumers in recent years, not only in Poland, but also in Europe and the United States, have proved surprisingly resilient to inflation, increasing spending. However, their growth is becoming more selective, and the need to rebuild savings, coupled with uncertainty about the further trajectory of inflation or energy prices, is prompting millions of households to operate more cautiously with their budgets and rebuild savings. Will positive trends on the wage growth side and 'solid' consumer sentiment on both sides of the Atlantic translate into a successful November for retailers and record shopping on Black Friday? Or will 'Black Week' turn out to be a disappointment? And above all, what kind of reaction can we expect from the stock market?

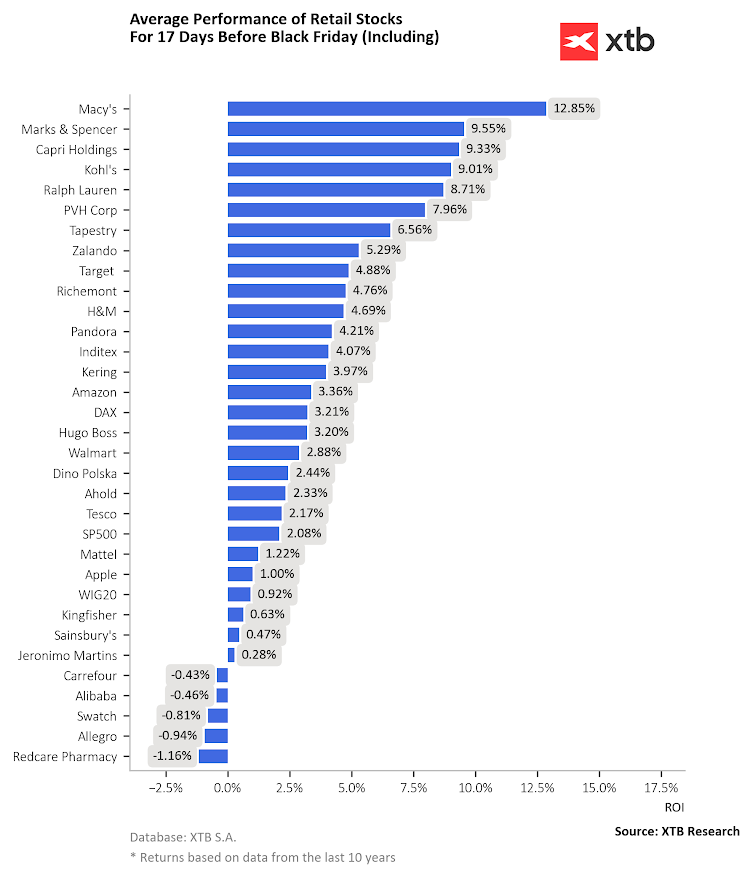

Retailer stocks have done better than the S&P 500 over the past 10 years, with investor activity usually rising about two weeks before Black Friday. This year, the gap, still favorable to the retail sector, has weakened slightly. Source: XTB Research

Start investing today or test a free demo

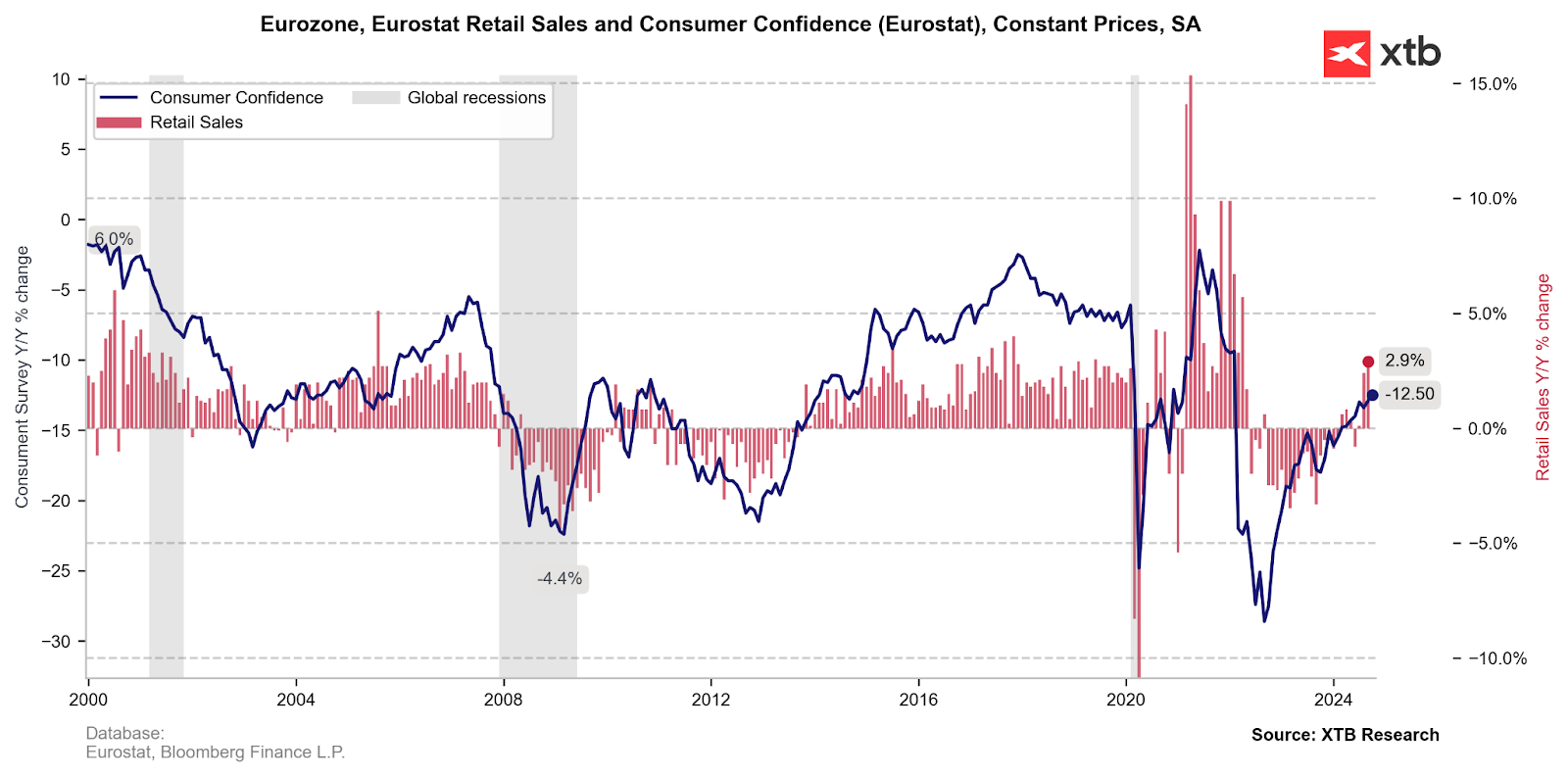

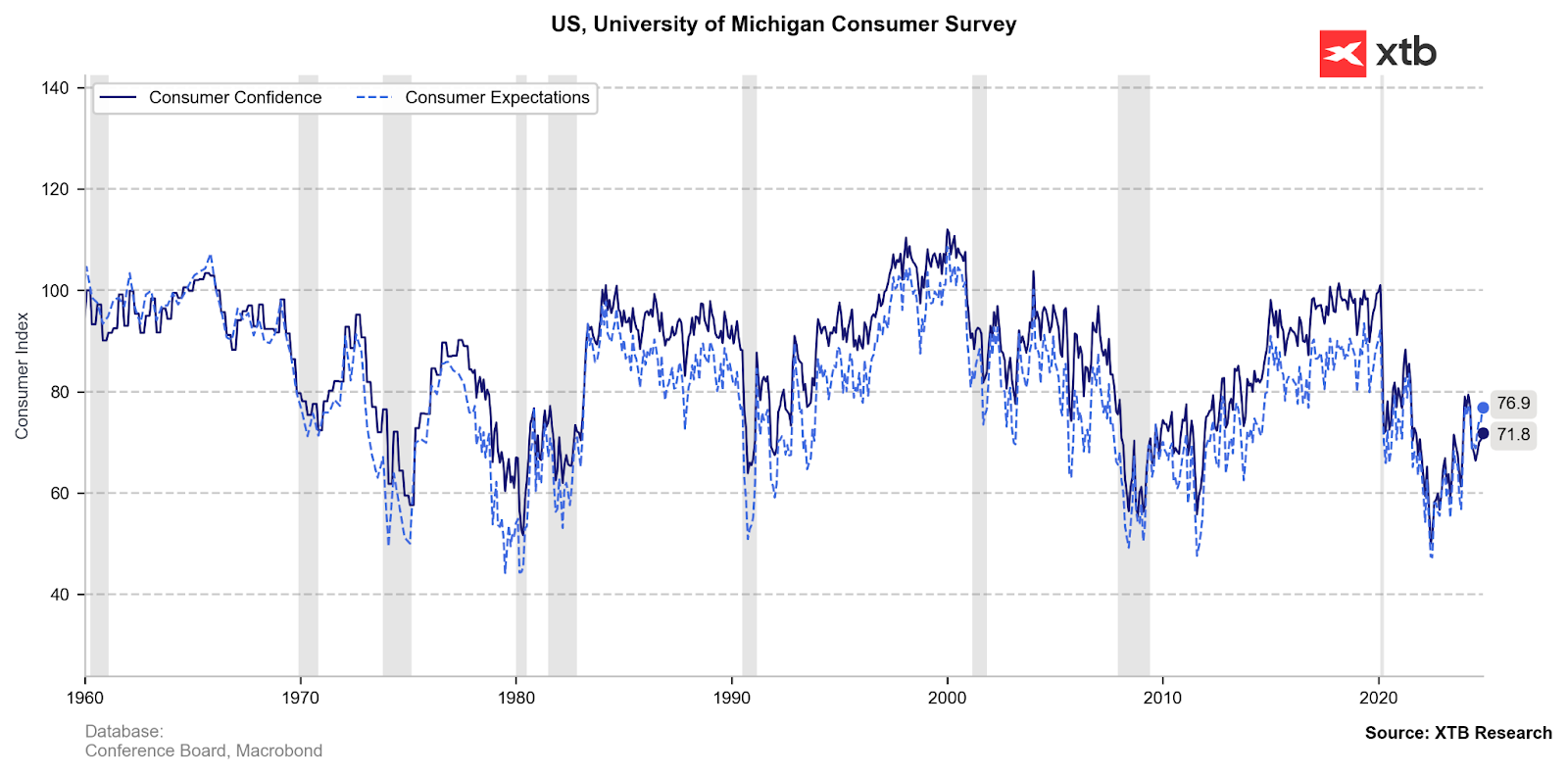

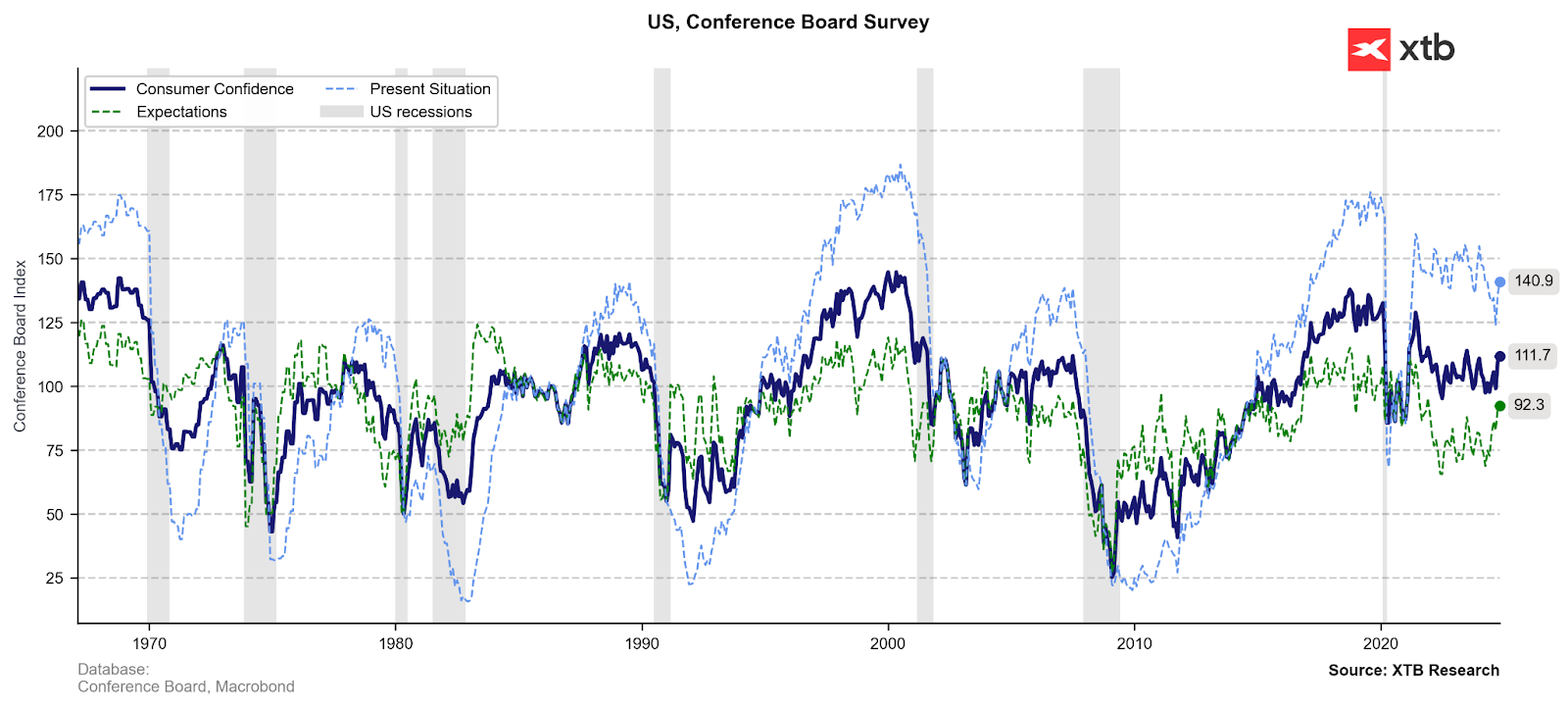

Create account Try a demo Download mobile app Download mobile appLooking at consumer sentiment in Europe and the United States, one can see a very significant improvement from levels in late 2022 and early 2023, when pessimism about the condition of the global economy was at record levels. This, coupled with a potentially weak Black Friday, could represent some disappointment and expand the discussion around changes in consumer trends, their impact on the market, or even a potential reversal of the 'optimistic trend'.

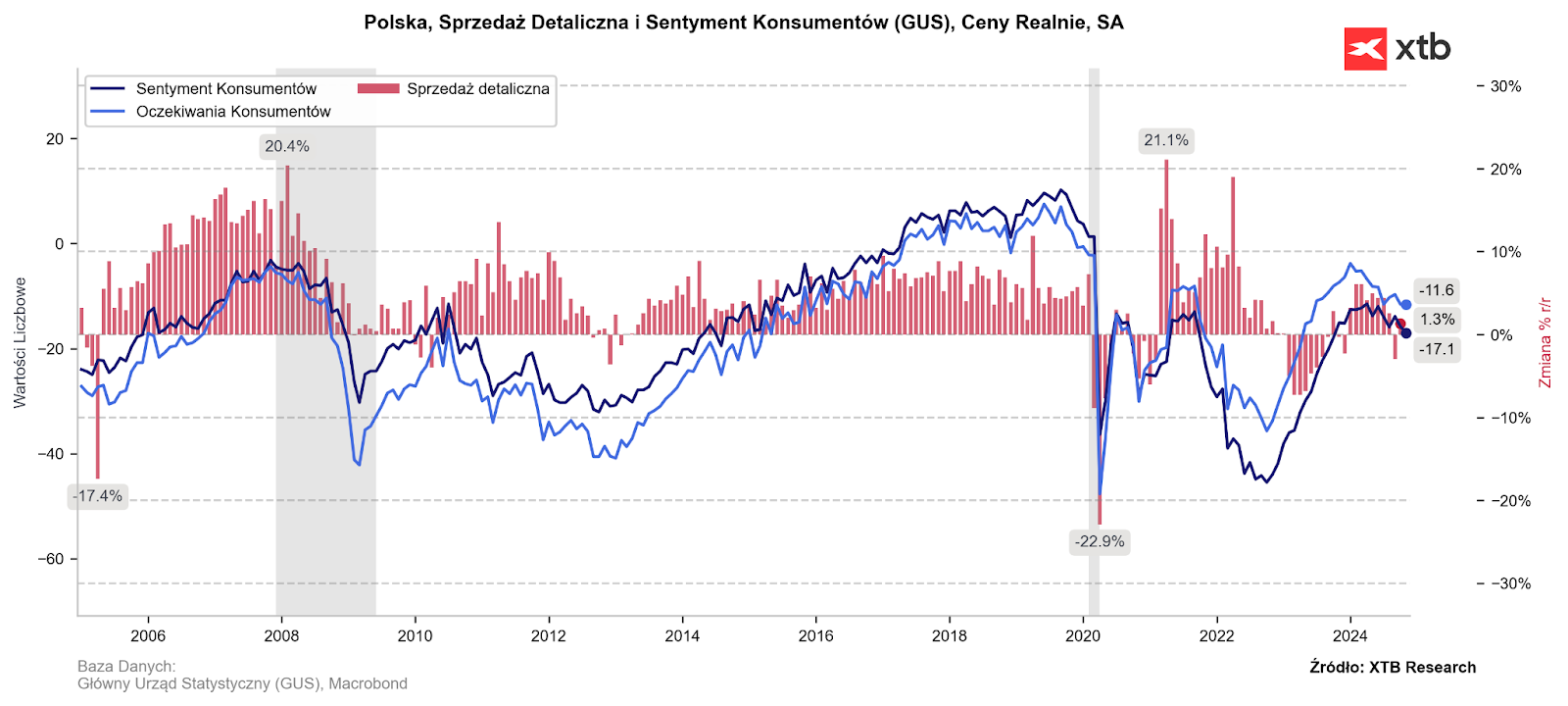

In Poland, we are actually seeing a significant cooling of sentiment in 2024, and 'confirmation' of this trend can be found in the mostly weaker performance of shares of Polish retail companies, and related industries. In recent months, we have seen inflation accelerate, and higher energy prices are making consumers even more uncertain about tomorrow. As a result, the prevailing trend is to postpone spending. Moments before Black Friday, it is futile to look for signs of optimism. Will record 'seasonal' promotions go unnoticed this year? Or are consumers already sharpening their teeth for sales of some companies' overstocked inventory?

Source: XTB Research

Uncertain future for retailers

The retail industry acts as the front line and is one of the first to feel the weakness of consumers as well as a surge of activity on their part. With automated systems and data sets, large chains can react quickly and adjust prices to meet demand. There are many indications that falling inflation has indeed brought a decline in pricing power and limited room for margin expansion. Consumer patterns are not fixed, and real wage growth is not always associated with a corresponding increase in purchases.

Black Friday will be an important indicator this year of the actual global strength and actual 'need' for consumption in major Western markets. The recent performance of the fashion/luxury sector, as well as retail chains that have operated for years on a higher margin relative to their competitors (in the US, a good example is Target vs. Walmart, in Poland, Dino Polska vs. Biedronka i.e. Jeronimo Martins), shows a rather different situation.

Consumers choose more often what is cheaper and give up 'prestige'. Although 'on paper' they look strong, they are leaning towards lower prices and often abandoning the 'unnecessary spending' they were willing to do in 2020 - 2022. The fashion industry was the first to feel the pressure from this side, where shares of fashion holdings like LVMH, Kering, Richemont, Swatch and PVH Corp. collapsed. Declines have so far been resisted virtually only by companies creating exclusive goods, such as Hermes, Ferrari and Brunello Cucinelli.

The rise in popularity of online sales means a higher emphasis on online offerings and probably a reduced number of in-store promotions. Convenience and cost-effectiveness may steer consumers toward e-commerce orders. The change is by no means unequivocally positive for the retail industry and could put pressure on margins, due to higher order fulfillment costs. Are interest rates taking a toll? The weaker performance of the stocks of retailers, which have historically done very well, just before Black Friday raises some concerns about consumer activity and sales performance during this period.

Prior to Black Friday, shares of New York department store chain Macy's, Marks & Spencer and Kohl's were the strongest gainers. Over the past month, however, Macy's has gained a disappointingly small amount of more than 2.5% (vs. an average of 12.8%), Marks & Spencer shares have seen no significant change in value, Kohl's is down 20%, and Capri has gained 6.5%, below the statement measure. Allegro's shares don't look like the beneficiary of this trend at all (including this year), and Dino performs weaker against its U.S. peer, Walmart, though clearly better, than Tesco or Jeronimo Martins. Source: XTB Research

U.S. retailers 'not delivering'

Polish retailers aren't the only ones with a problem this year. Bloomberg data shows that the observed sales growth of 'flagship' retailers Walmart and Kohl's is slower than in 2023; for Walmart it is 1.3% y/y, while Kohl's records a nearly 10% decline. At Target i.e. Walmart's biggest competitor, sales are down 1.2% y/y, while at Best Buy, where consumers 'hunt' for promotions related to long-discounted electronics and consumer electronics and appliances, y/y growth is 5.5%.

Lower inflation is driving prices of some goods down. Incoming, current data suggests that major retailers in the U.S. are reporting year-on-year declines, except Walmart, which is up 0.4%. Comparable sales at Walmart stores, which attracts a consumer oriented toward promotions and savings, are expected to increase by 3.9%, for Target to grow year-on-year only marginally, and for Best Buy and Kohl's to decline.

Many Black Friday deals are also available online, which may keep consumers from visiting stores and malls. Placer.ai data suggests that visits to U.S. stores in October through November 15 were down year-on-year at Target and Best Buy, as well as Kohl's; for Walmart, the increase was trace.

During Black Friday in 2023, growth in shopper visits weakened at Target, Best Buy and Kohl's. Then, Walmart-only traffic was stronger than in 2022. This year, that dynamic is unlikely to change. Retailers have been promoting Black Friday deals since the beginning of November, just as they did a year ago. This strategy can help attract thrifty shoppers who spread out their purchases over time, as well as weaken the size of the shopping cart. To sum up, it is not worth expecting 'fireworks' after Black Friday this season, and the performance of retailers' stocks suggests that the market has not built up high expectations for November-Christmas sales in recent weeks.

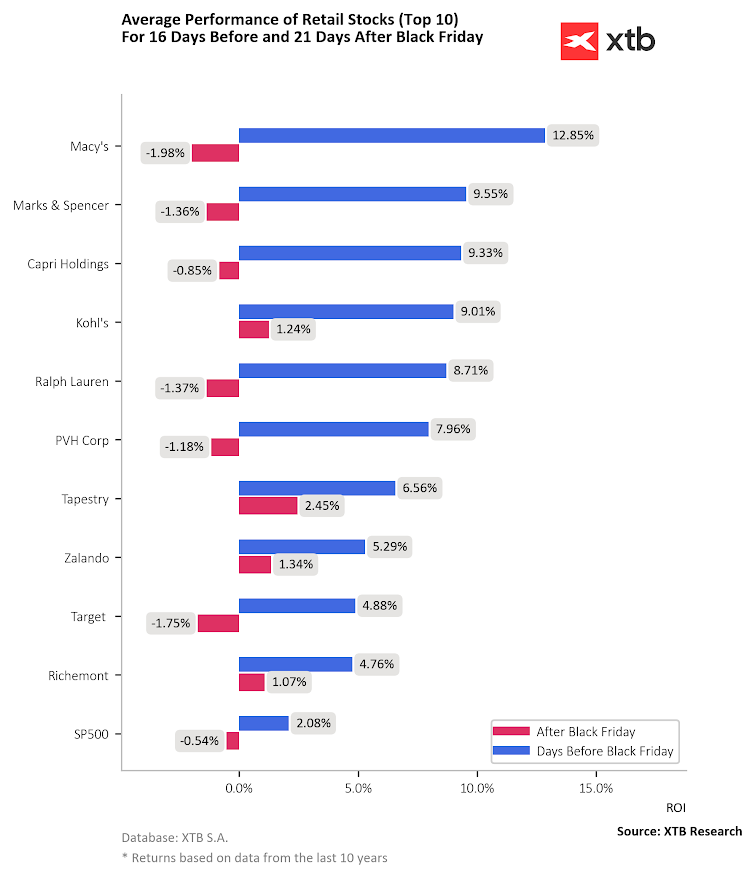

Looking historically, Black Friday turned out to be more of a 'bargain' for profit-taking. While the stocks of retailers gained significantly two weeks before the 'peak' of promotions, after Black Friday, most of the companies' shares recorded declines. Source: XTB Research

Walmart (WMT.US, D1 interval)

Stocks of American retailers such as Target, Macy's or Kohl's are underperforming Walmart (WMT.US) since 2022, as the Walton's company seems to be a main beneficiary of rising inflation, providing lower prices.

Source: xStation5

Eryk Szmyd Financial Markets Analyst XTB

Bartłomiej Mętrak Financial Markets Analyst XTB