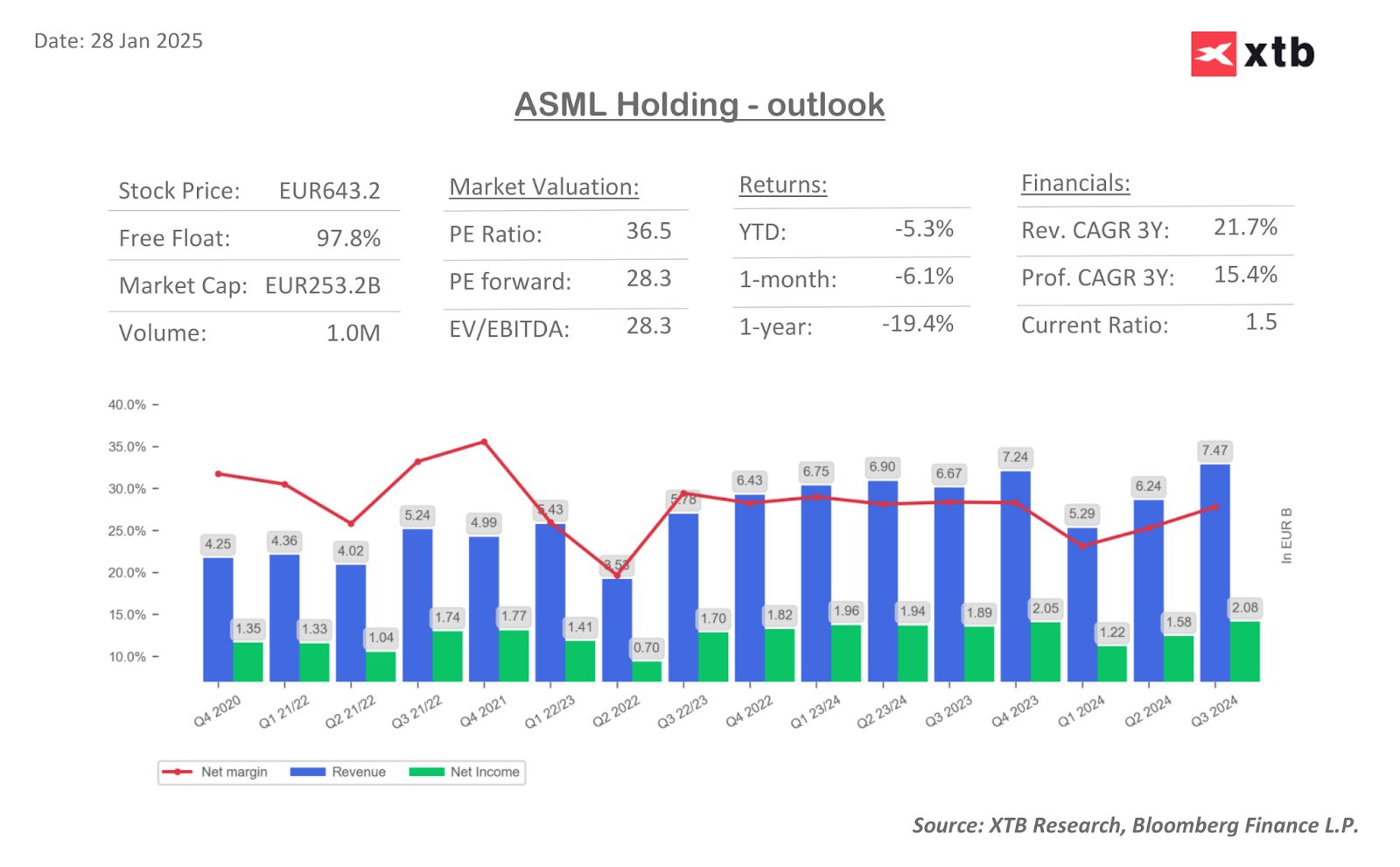

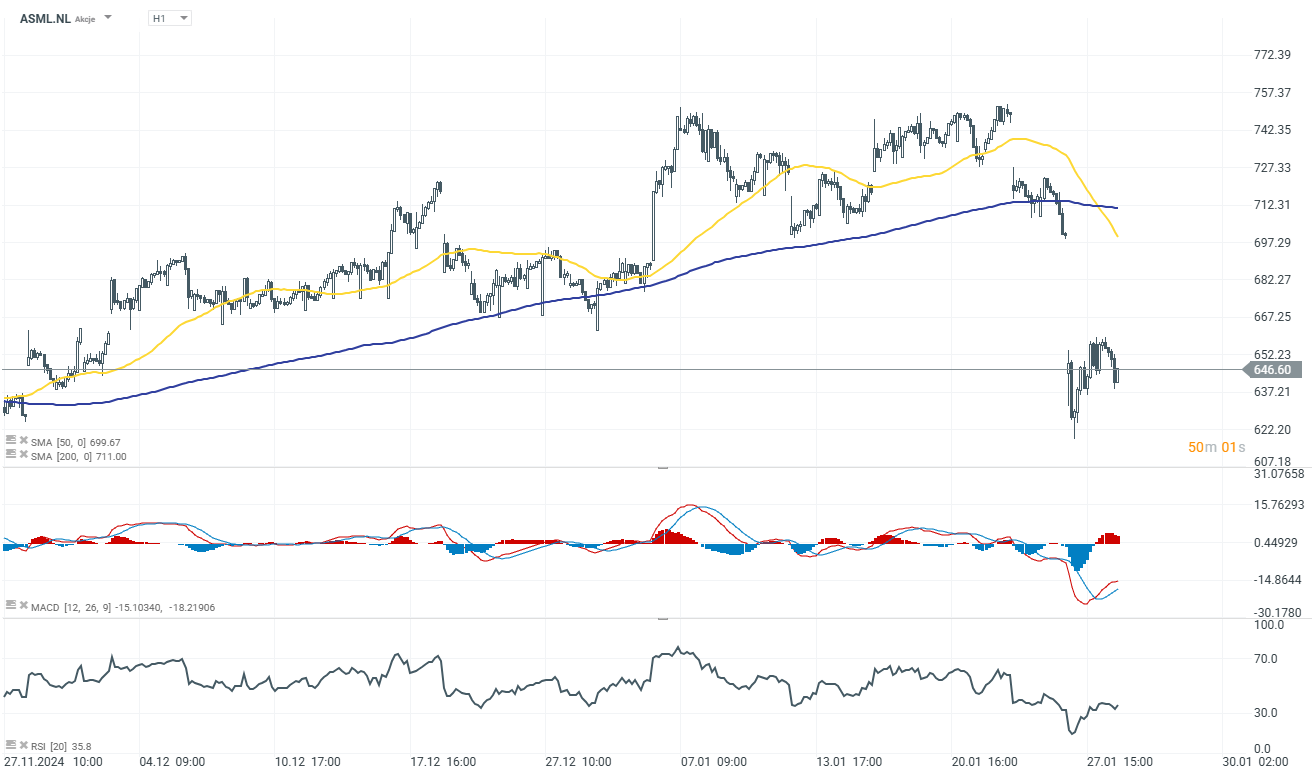

ASML Holding (ASML.NL) declines in today's session, further extending yesterday's losses. A global leader in semiconductor equipment, is set to release its Q4 2024 earnings on January 29, 2025 before market open. This report comes at a critical time as the company faces both opportunities and headwinds, including the emergence of China’s AI disruptor DeepSeek and ongoing geopolitical challenges. Below is a concise summary of what investors should watch for.

Key Points

- Revenue & Earnings Projections

- Q4 Revenue: Estimated at €9.02 billion, a 26.6% year-on-year increase.

- Net Income: Forecasted at €2.62 billion, reflecting robust demand for lithography systems.

- Gross Margins: Expected at 49.6%, slightly lower due to High-NA EUV system costs.

- Earnings Per Share (EPS): Projected at €6.68.

- Order Bookings & Systems Sold

- Q4 bookings are estimated at €3.53 billion, with 121 lithography systems shipped.

- EUV orders remain subdued, with analysts anticipating a €1 billion contribution.

- DeepSeek’s Impact

- The rise of DeepSeek, a Chinese AI startup using less advanced, cost-efficient chips, could reshape demand for high-performance semiconductors.

- DeepSeek’s approach raises concerns about long-term EUV sales, a key driver for ASML.

- 2025 Guidance

- ASML maintains its 2025 revenue guidance at €30–35 billion, though expectations lean toward the lower end due to geopolitical uncertainties and customer delays.

- Geopolitical and Customer Risks

- Ongoing U.S. export restrictions limit ASML’s sales to China, its third-largest market.

- Dependency on major clients like TSMC, Samsung, and Intel makes the company sensitive to spending cutbacks.

Analyst Commentary

- Citi: Highlights a lower hurdle for ASML following its recent share price drop, with expectations for bookings as low as €2 billion.

- JPMorgan: Expects ASML to meet 2025 guidance unless Intel/Samsung make drastic cuts. Sees 2026 orders from TSMC in H1 2024.

- Barclays: Does not anticipate significant near-term recovery in EUV orders, given lingering uncertainties.

- ING: Optimistic about strong order momentum, despite limited surprises expected for the full-year update.

ASML’s Q4 results will be crucial in understanding its strategy to address evolving challenges:

- AI Demand & DeepSeek’s Impact: Will ASML address risks of cheaper AI models reducing reliance on cutting-edge chips?

- China Exposure: 15–20% of 2023 sales came from China; updates on export controls and domestic competition (e.g., SMEE’s lithography tools).

- 2025 Guidance Confidence: Any revisions to €30B–€35B sales target amid geopolitical and demand risks?

ASML’s monopoly in EUV lithography (critical for AI/advanced chips) and €6.17B cash cushion provide resilience. However, DeepSeek’s rise, China risks, and customer concentration (TSMC, Samsung, Intel) pose challenges. The earnings call’s tone on 2024 order visibility and AI-driven demand shifts will be pivotal for sentiment. Watch bookings data and management’s 2025 confidence – a beat on €4B+ orders or upbeat EUV commentary could catalyze a rebound.

Source: xStation 5

Economic calendar: NFP data and US oil inventory report 💡

Daily summary: Weak US data drags markets down, precious metals under pressure again!

Datadog in Top Form: Record Q4 and Strong Outlook for 2026

US Open: Wall Street rises despite weak retail sales