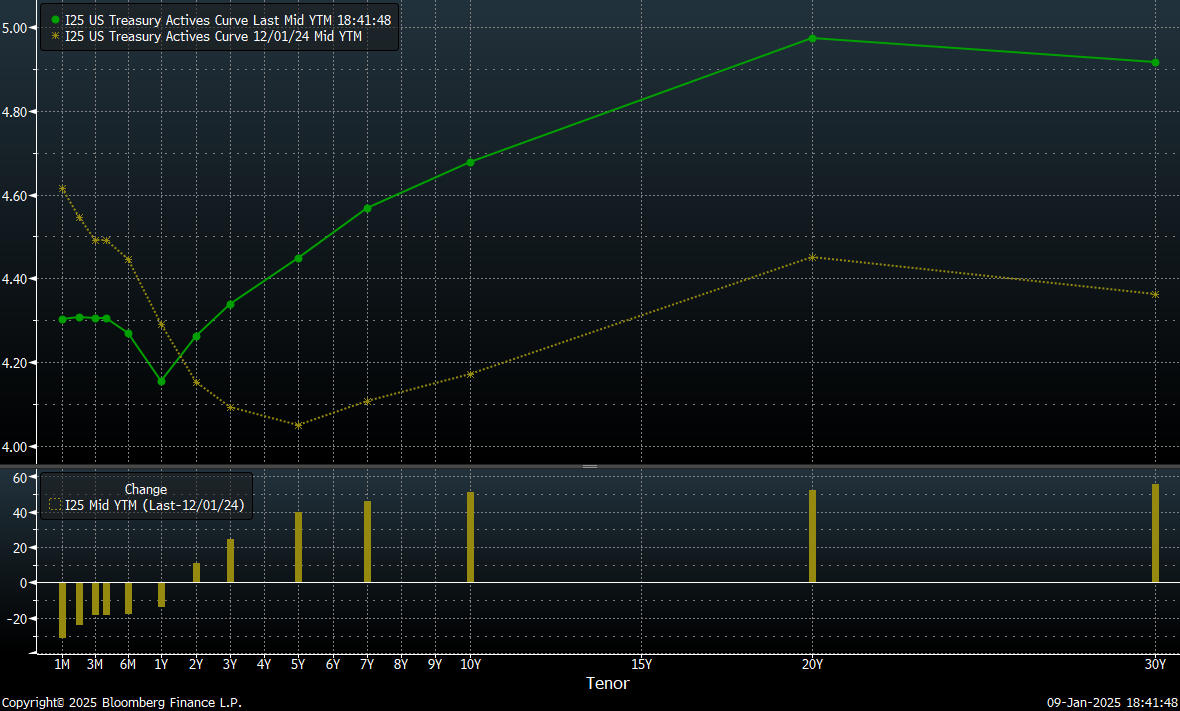

The US long term treasury yields have seen a sharp rise over the past month, partly driven by growing market concerns about inflation and the Fed's future decisions. However, the current steepening of the yield curve compared to December 2024, supported by both the sharp movement in long-term bond yields and the decline in yields on shorter-term bonds, raises questions about the future direction of investor movements and casts doubt on the extent of the market's response.

Start investing today or test a free demo

Open real account TRY DEMO Download mobile app Download mobile appToday's yield curve (green line on the chart) and the yield curve from December 1, 2024 (yellow line on the chart). Source: Bloomberg Finance L.P.

Wednesday's movement, driven by concerns over Donald Trump's policies and the potential introduction of drastic tariffs targeting both the political allies and economic opponents of the U.S., pushed the 10-year bond yields to 4.728%, surpassing the April peaks on a yearly basis. This marks the highest level since the October 2023 peak, which came shortly after the end of the fastest interest rate hike cycle of the 21st century. Such a yield movement could serve as a basis for taking long positions by funds looking to go against market sentiment. Any failure of the risks associated with Trump's announcements to fully materialize would leave room for yields to decline, even in the face of a slower rate-cutting cycle by the Fed.

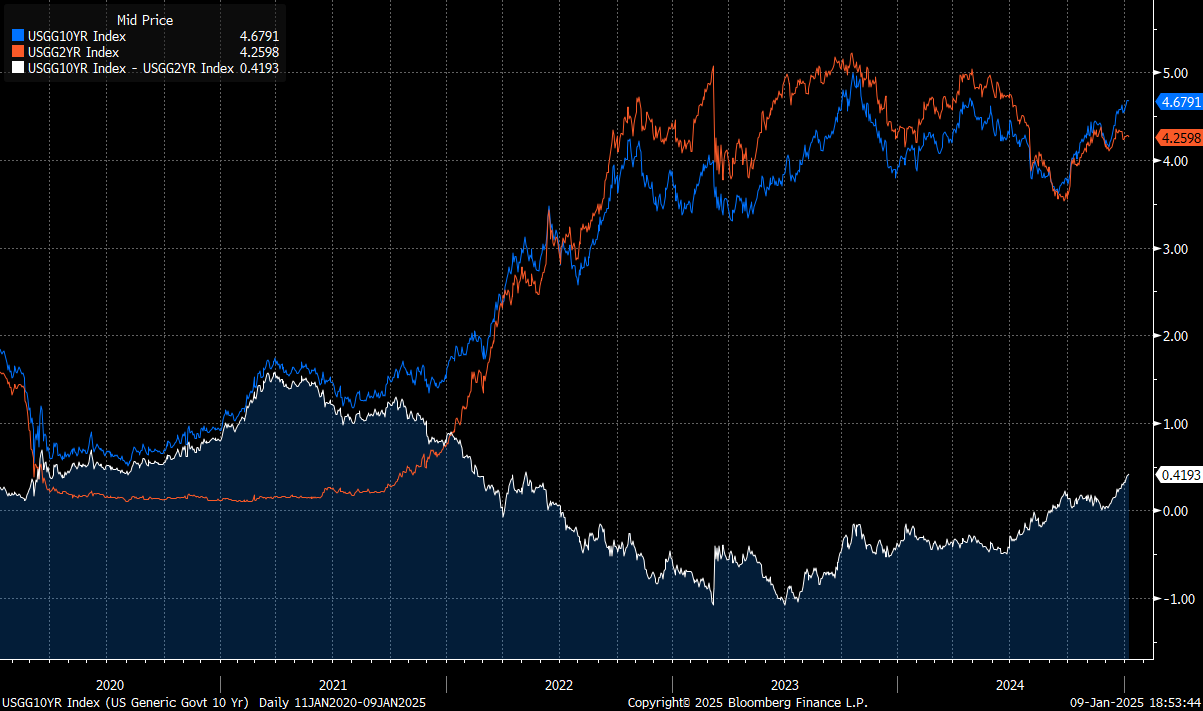

It is also worth noting that recent movements in the bond market have led to the highest value spread between 10-year and 2-year treasury yields since 2022, which currently stands at 41.9 basis points. The spread value returned above zero in the last quarter 2024 after approximately two years of being below zero. A strong upward movement of the spread, combined with the stabilization of 2-year U.S. bond yields around 4.26%, could create additional pressure to reverse the 10-year yield impulse back to 4.3%.

The U.S. 2-year Treasury and 10-year Treasury yields and their spread over the last 5 years. Source: Bloomberg Finance L.P.

It is worth noting, however, that if market concerns are realized, such as the imposition of broad tariffs, a strong labor market is maintained, and inflationary pressures return, the yields on short-term bonds may continue to rise at a similar pace as long-term ones. As a result, instead of a narrowing of the spread due to a decline in 10-year bond yields, we could see the spread close from the bottom due to the rise in 2-year bond yields.

The futures price of U.S. 10-year bonds approached a key support level of 108.02 yesterday. If this level is breached and the downward trend continues, the next significant support will be the April lows around 107.37, which represent the last support before the lows of 2023, marking the lowest level of the contract since 2006. Source: xStation