CPI inflation will be key for Fed

While the Fed is looking primarily at PCE inflation, CPI is usually released earlier and shows the general trend that PCE is likely to follow. Also, PCE inflation usually reacts later and with a lag compared to CPI but larger shifts in CPI gauge recently have given markets hope that Fed may be less hawkish going forward. What to expect from today's reading? Median forecasts point to a significant slowdown in both headline and core annual gauges. On the other hand, expectations for month-over-month readings do not look so rosy. While headline CPI is expected to be left unchanged, core inflation is expected to increase 0.3% MoM. This is still to a huge extent driven by 'shelter inflation'. However, should headline CPI gauge drop by 0.1-0.2% MoM and core gauge increase just 0.1-0.2% MoM, Fed would have reasons to slow rate hikes further. Without such a steep drop in inflation measures, it is unlikely that Fed will change its approach.

Headline CPI inflation is expected to slow to 6.5% YoY but, given lack of drop in monthly reading, markets would welcome a drop to 6.2-6.3% YoY. Should core gauge come in above expected 5.7% YoY, USD will have a chance to recover from recent losses. Source: xStation5

Headline CPI inflation is expected to slow to 6.5% YoY but, given lack of drop in monthly reading, markets would welcome a drop to 6.2-6.3% YoY. Should core gauge come in above expected 5.7% YoY, USD will have a chance to recover from recent losses. Source: xStation5

Energy prices are dropping

Of course, taking a look at energy prices we can see that those dropped significantly in December. This means that the contribution of energy prices is likely to drop further from the current 1 percentage point. It stood at above 2 percentage points in mid-2022.

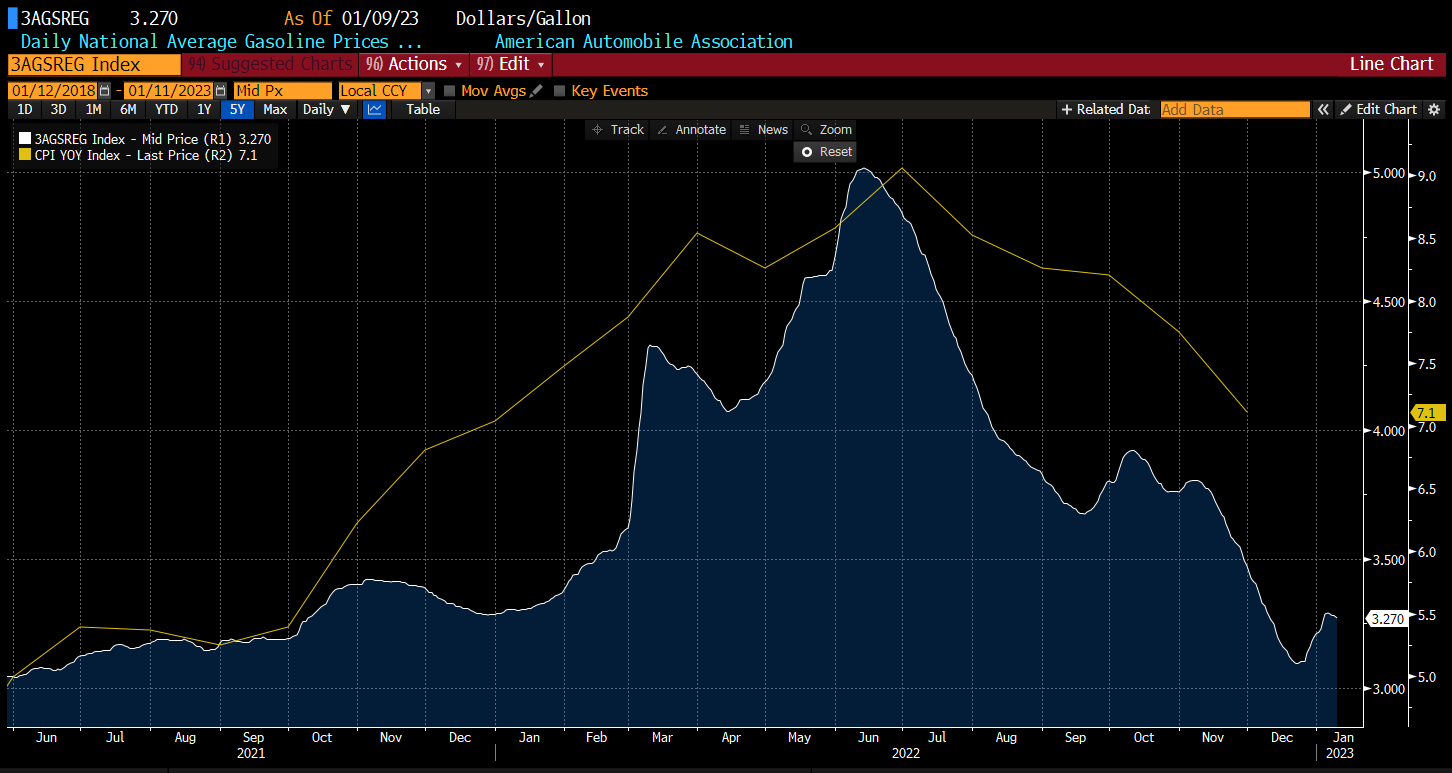

Fuel prices dropped and were lower than a year ago. Gas prices were significantly higher but this relates only to market prices, not consumer prices. Simultaneously, one should remember that gas prices have dropped significantly off the peak. Source: Bloomberg

Fuel prices dropped and were lower than a year ago. Gas prices were significantly higher but this relates only to market prices, not consumer prices. Simultaneously, one should remember that gas prices have dropped significantly off the peak. Source: Bloomberg

Food prices are expected to start dropping

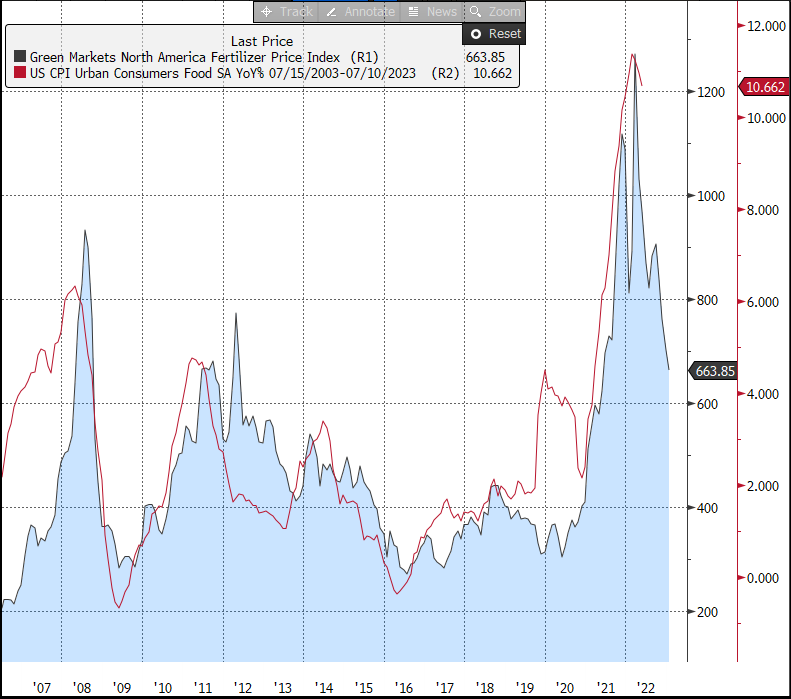

A bearish trend on the food market can also be spotted. A drop in fertilizer prices signals that food prices may drop even quicker in the coming months. Source: Bloomberg

A bearish trend on the food market can also be spotted. A drop in fertilizer prices signals that food prices may drop even quicker in the coming months. Source: Bloomberg

Cars and rents key for core inflation

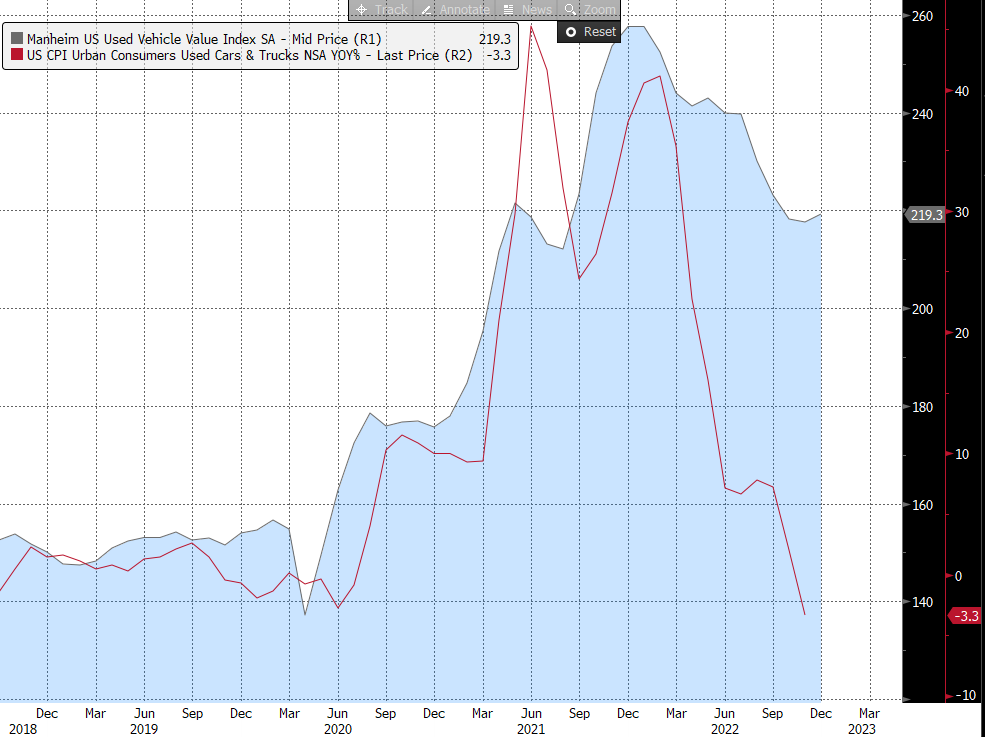

When it comes to core inflation, cars and rents will be key components. Car prices dropped recently but December saw a rebound. Of course, earlier price cuts should also impact CPI reading, which tends to react with a lag. When it comes to rents, lagged inflation data continues to show rising prices but more timely market data starts to show signs of slower price growth emerging.

Car prices according to Manheim index and car component in CPI inflation. Source:Bloomberg

How will US100 react?

US100 has been one of the most oversold major indices in 2022. The latest drop in yields failed to support the Nasdaq index as it was the case with S&P 500. Fed will look primarily at core inflation data for hints on the size of a rate hike at February meeting. Market is currently pricing a small chance of a 50 bp rate hike and latest comments from Bostic and Daly showed that today's data will be crucial. If headline inflation slows to 6.3% Yoy or more, euphoria on the markets may ensue. On the other hand, if car prices and rents have a significant contribution to inflation in December, Fed may have reasons to go on with a 50 bp rate hike. In such a scenario, US100 may trim recent gains and USD may regain some of its shine.

If US inflation slows significantly more than expected, the range of the double bottom pattern on US100 may be realized and the index may break above 11,600 pts. On the other hand, should core inflation surprise to the upside, the chance for a 50 bp rate hike would increase and US100 may pull back towards 11,300 pts. Source: xStation5

If US inflation slows significantly more than expected, the range of the double bottom pattern on US100 may be realized and the index may break above 11,600 pts. On the other hand, should core inflation surprise to the upside, the chance for a 50 bp rate hike would increase and US100 may pull back towards 11,300 pts. Source: xStation5

Reggeli összefoglaló: Trump „a kőkorszakba” akarja visszaküldeni Iránt. Az indexek zuhannak (2026. április 2.)

Live Trading - 2026.04.01.

Gazdasági naptár: hamarosan érkeznek az ISM- és az ADP-adatok 🔎

Reggeli összefoglaló (01.04.2026)

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.