Just as cars cannot drive without having oil in the tank or a charged battery, the market for new technologies cannot develop without silicon integrated circuits. These chips require huge development expenditures and special production conditions. The world faced the prospect of competition for strategic supplies of semiconductors, which can determine the pace of technological development and the competitiveness of businesses in the new technology market.

Demand for new technologies and devices began to weaken in an environment of global recession and inflation, and the semiconductor market faced the prospect of contraction due to sanctions imposed on its largest consumer, the Middle Kingdom. Threatened by Chinese intervention, Taiwan, which is still the hub of global chip production, came into focus. Does the fear that has set in on the semiconductor market create an investment opportunity?

U.S. looks toward domestic manufacturing

The globalized world worked, and chip supplies were not a problem supporting manufacturers' margins until China's emerging power began to pose a significant security threat to the United States, and the global supply chain was shaken by a coronavirus pandemic. For many years, U.S.-based technology giants diverted chip production to Taiwan without fear of possible confrontation or Beijing's claims to the island.

However, the situation has changed with the rise of China. Tensions have not eased, with President Xi Jinping stressing at the October Chinese Communist Party summit that China reserves the right to use force against Taiwan, which China regards as an integral part of its national borders. The Biden administration, in turn, has pledged military assistance in the event of aggression by the Middle Kingdom; moreover, the United States is working on a land lease bill that would make available to Taiwan the ability to directly lease U.S. military equipment on 10-year repayment terms. The chip market has become extremely sensitive to escalating geopolitical tensions.

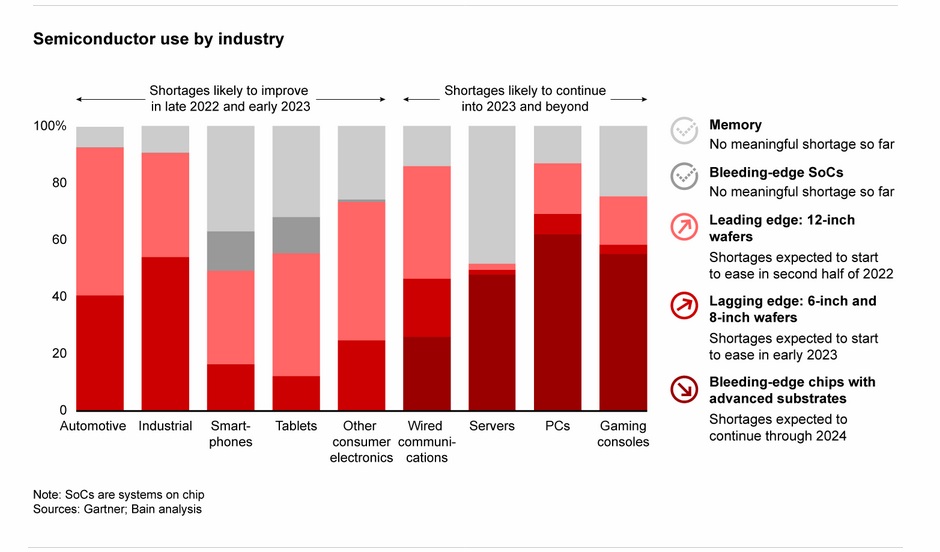

Not surprisingly, the technology market fears a collapse; after all, Taiwan Semiconductor's factories account for nearly 65% of global semiconductor shipments, including 90% of shipments of 7nm and smaller chips used in cutting-edge technologies. Nearly 60% of the world semiconductor market's revenue is consolidated on the island, and it is where Silicon Valley giants have so far moved production. China has already been almost completely isolated from Taiwanese supplies, the US fears Beijing's technological armament development and does not want to stimulate it with the latest generation of chips.

The chipmakers are ill-served by sanctions that deprive them of access to the Chinese sales market. After all, China is the largest consumer of chips, spending $350 billion in 2020, more than on oil imports. China's chip production accounts for just 5% of the world's output and is not enough to saturate its domestic market. What's more, China is condemned to importing cutting-edge chips because its technology does not yet allow mass production of semiconductors used in computers, laptops or smartphones.

Republicans against Chips and Science ACT

The Democratic Party, which currently holds a majority in both chambers of Congress, has pushed through the Chips and Science ACT, a bill to support the US semiconductor market with nearly $52 billion in funding, which will go toward research and rebuilding the chip industry in the US. The bill was met with criticism from Republicans, who voted against it and accused its authors of siphoning public money at a time of inflation, overburdening the budget and providing insufficient safeguards against the influence of Chinese capital.Midterms elections will be held in November, which could shed more light on the semiconductor sector and Beijing's relationship with Washington.

We can guess that a Republican victory in the House of Representatives and Senate elections is likely to be met with a negative reaction from US chipmakers, although the need to gradually move chip production from Taiwan to the US seems more legitimate than ever. However, it will not be without an impact on the margins of the major players, as it requires financial outlays, and the specific industry requires years of investment. It takes up to two years to build a factory with easy access to materials, and due to the cost and coordination of the entire supply chain, the cost usually pays for itself only after another five years, which is a major reason why the market is reluctant to abandon the services offered by manufacturing facilities in Taiwan.

Investment opportunity?

Focusing on the semiconductor market, we have selected two listed companies that have shown the strongest revenue growth, strong cash position and high levels of net profit in 2020 and 2021 compared to other companies in the industry. Both companies have relatively little debt, although the amount of technology industry debt has increased by leaps and bounds as interest rates have risen and financing costs have risen. Philadelphia's PSI semiconductor index, which measures the average stock prices of the 30 largest U.S. chip companies, has fallen nearly 50% this year, with 38% of the decline coming in 2022, making it the largest annualized decline since the 2008 financial crisis.The average price-to-earnings ratio for the PSI index companies is 14.5, which is an 11% deviation from the index's historical average and a nearly 40% discount to the NASDAQ average c/z ratio. So let's take a look at the two fastest-performing U.S. companies.

Advanced Micro Devices (AMD.US)

The company has a well-diversified business supplying systems in both the processor and GPU markets, with both markets ranking second behind Intel and Nvidia, respectively, which have businesses that are geared decidedly more to one side. AMD's stock provides exposure to industries such as gaming, cryptocurrencies, the metaverse, cloud computing, data centers and automation, where AMD-supplied chips are an indispensable, fundamental part of growth. Over the long term, the company's stock is likely to be able to return value to shareholders as the landscape around the technology market begins to improve.

The company has long-term agreements with Microsoft and Sony. The company's gaming sector still grew 32% y/y despite the slowdown in the technology market. Sales forecasts for the console market remain optimistic, with both Microsoft and Sony expecting higher sales of the PlayStation 5 and Xbox.

Additionally, margins may be positively impacted by the acquisition, completed at the beginning of the year, of Silicon Valley-based US manufacturer Xilinx, which developed FPGAs and to date holds half of the global market for devices made with this technology. With the acquisition, AMD is positioning itself to benefit from the development of AI and edge computing. The company is able to compete in the processor market with Intel, the Ryzen chip remains the most powerful gaming unit at least until the upcoming release of Intel processors, Rapor Lake. AMD also has a diversified location of production facilities, with the largest located in the Batu Kawan industrial park in Penang, Malaysia. In June, the company announced plans to expand its manufacturing expansion in Malaysia. Only a portion of production is being redirected to Taiwan's TSMC, while most chipmakers primarily use Taiwanese capacity.

AMD will show results on November 1 this year. The key question is whether the market has already priced in a slowdown in demand in the PC market, if so - a drop in activity in this segment is unlikely to cascade down AMD, which has already lost nearly 70% of its valuation since the beginning of the year. The company expects a 45% annual return from the Data Center sector, but has cut its annual growth forecast to 29% from its previous 55% estimate due to the slowdown in the PC industry.

AMD (AMD.US) shares, D1 interval. The stock is moving in a downtrend, and looking at the bands of the 200 and 50 session averages, there are no signs that the 50SMA is preparing to reverse towards the SMA200 which could result in a 'golden cross' and trend reversal. Fundamental indicators are healthy and trading at a discount from the index average. The price-to-earnings ratio is 16 points, while the price-to-book-value ratio oscillates at 1.7 and is nearly .065 below the index average. The debt-to-asset ratio at the end of Q2 was 0.04, meaning that for every $0.04 in debt the company has $1 in assets. The long-term debt ratio increased, but levels are still safe at 0.03 on a debt-to-asset basis. Source: xStation5

Nvidia (NVDA.US)

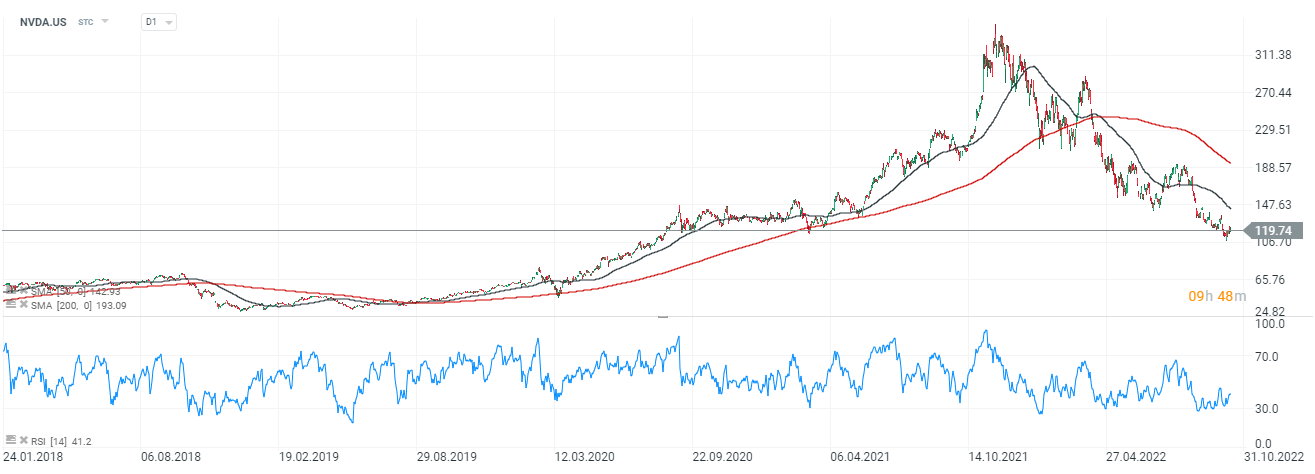

The company is AMD's main competitor, and despite the similarities in the quality of the two companies' products, Nvidia's graphics chip technology appears by many to be marginally superior (at the expense of price to the consumer).

The semiconductor market has recently faced the specter of stagnant business in China, on which the U.S. has imposed sanctions.However, Nvidia has confirmed that the U.S. government will allow it to continue developing its H100 artificial intelligence chip in China. The company's recent results have not been optimistic, with the end of the Covid boom (which supported the computerization of remote work), a decline in mining activity in the cryptocurrency space, and the migration of the second largest cryptocurrency, Ethereum, to a 'proof of stake' system and associated declines in RTX graphics chip margins limiting bullish momentum.

The company operates primarily in the gaming and database sectors - both of which analysts agree will grow over the next decade. Additionally, margins may be supported by Nvidia's growing Omniverse virtual industrial simulation segment, 'digital twin' technology and the growing popularity of cloud gaming.

The company has already lost more than 65% from its highs. The one-year average target price recommended by analysts is $192 per share. The company will report its latest results on November 16. EPS is expected to reach $0.71, compared to $0.51 last quarter.

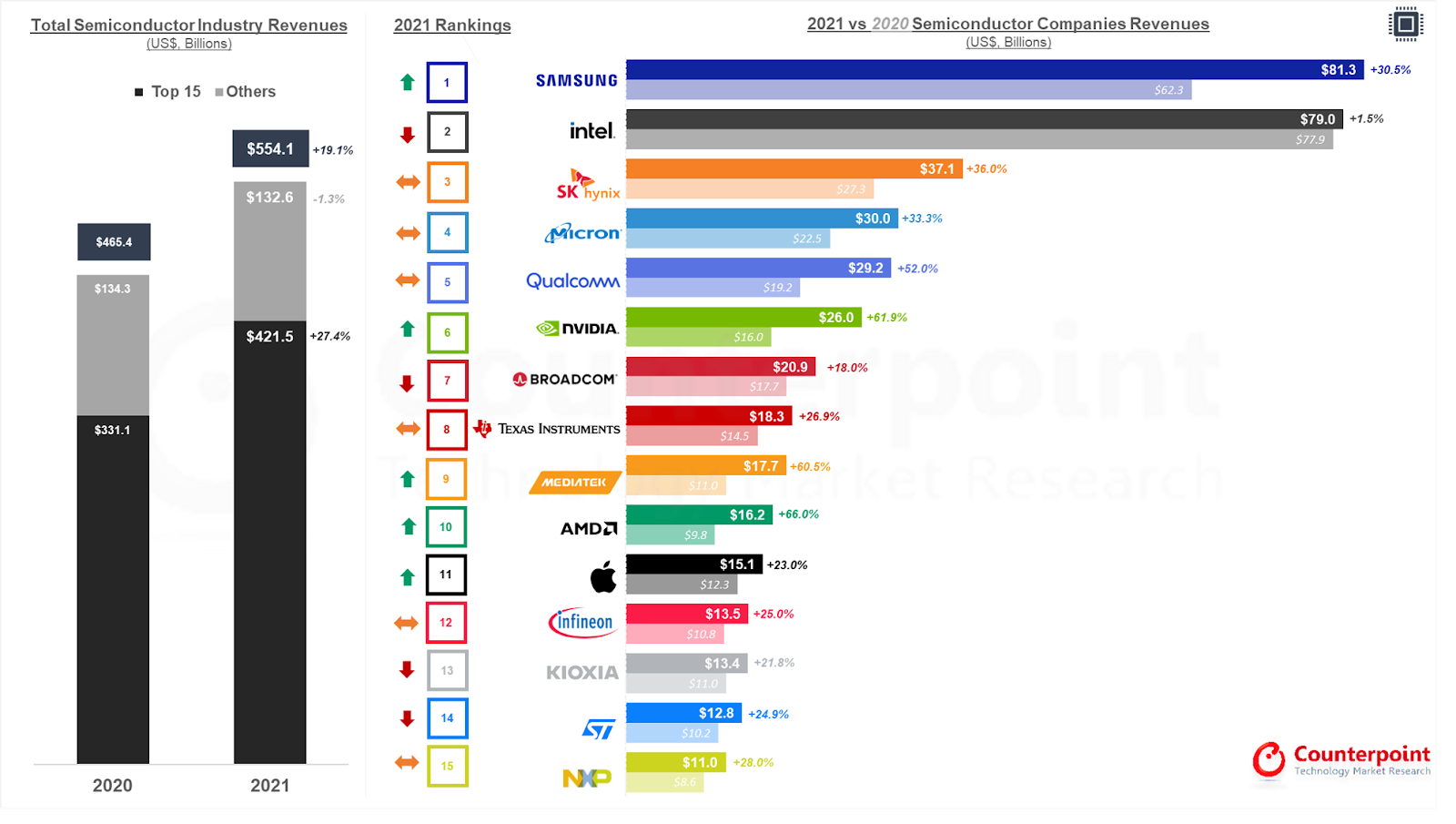

The report created by analysts in 2019 pointed to the value of the chip market at $405 billion in 2020 and $430 billion the following year, while reality showed that the estimates were far too conservative and the pace of technology development - underestimated. In 2020, the value of chipmakers' revenues indicated $465 billion, and in 2021 $554 billion (!) Going by this, we can see that the semiconductor market has grown faster than analysts' already optimistic assumptions, and the situation is likely to repeat itself as soon as chip demand improves as inflation falls and the global economic slowdown is resolved. It's worth noting, however, that in 2020 and 2021, chip demand has been further shot up by the cryptocurrency market, which has been moving in 4-year cycles so far, and a related 'mining sector' in which devices compete with each other's computing power to form a proof-of-work network. Source: Precedence Research

XTB Research

Gazdasági naptár: NFP-adatok és amerikai olajkészlet-jelentés 💡

Live Trading - 2026.02.10.

🌍 Gyorsjelentési szezon az XTB-vel

🌍 Gyorsjelentési szezon az XTB-vel

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.