Euphoria in the stock market fueled by AI technology and the prospect of an imminent end to interest rate hikes in the US has caused investor capital to begin flowing into technology ETFs at a very strong pace. Market bulls are looking primarily toward the Nasdaq 100 index, which was heavily oversold last year, and there is a good chance that the first half of this year will be one of the record-breaking ones in terms of positive change on the index. The capitalization of the seven largest U.S. technology companies has increased by a record nearly $3.8 trillion since the beginning of the year. Nvidia joined the ranks of companies valued at more than $1 trillion in May, leading the semiconductor maker's frenzied growth in shares. The stock market pendulum is back in motion - from panic and fears of a repeat of the 'dot-com' bubble sell-off, we moved smoothly to extreme euphoria. In the midst of it, shares of Apple or Microsoft have already hit new historic highs, and technology ETFs have not seen such huge inflows for a long time. What are they due to?

ETFs - diversified and easy exposure to technological rally?

The huge inflow of capital is directly due to the market euphoria resulting from artificial intelligence. This one is undoubtedly a technological milestone - it can affect the margins and performance of many companies. However, it is still unclear to what extent, making it difficult to value the future impact of AI on the revenues and margins of thousands of companies. This spurs imagination and prompts investors to pay ever higher prices for shares. Particularly those companies that have a real chance to scale their business thanks to the new technological revolution like Nvidia or Microsoft with a stake in OpenAI. Shares of Exxon Mobil, the largest oil producer in the U.S., are down 4% since the beginning of the year. At the same time, Apple has scored a 47% rally, and the company's market capitalization is approaching a dizzying $3 trillion.

Many investors are looking for passive exposure to the technological trend because you hear about artificial intelligence almost everywhere. Some of them don't have time to actively manage a portfolio or don't consider this method optimal in their case. There is also a sizable group of investors who prefer to invest in a broad index of companies, which potentially reduces the risk from erroneous investments. By purchasing shares in ETFs, an investor is assured that his investment will reflect the 'average' - in good times for technology, however, the 'average' can be very satisfactory.

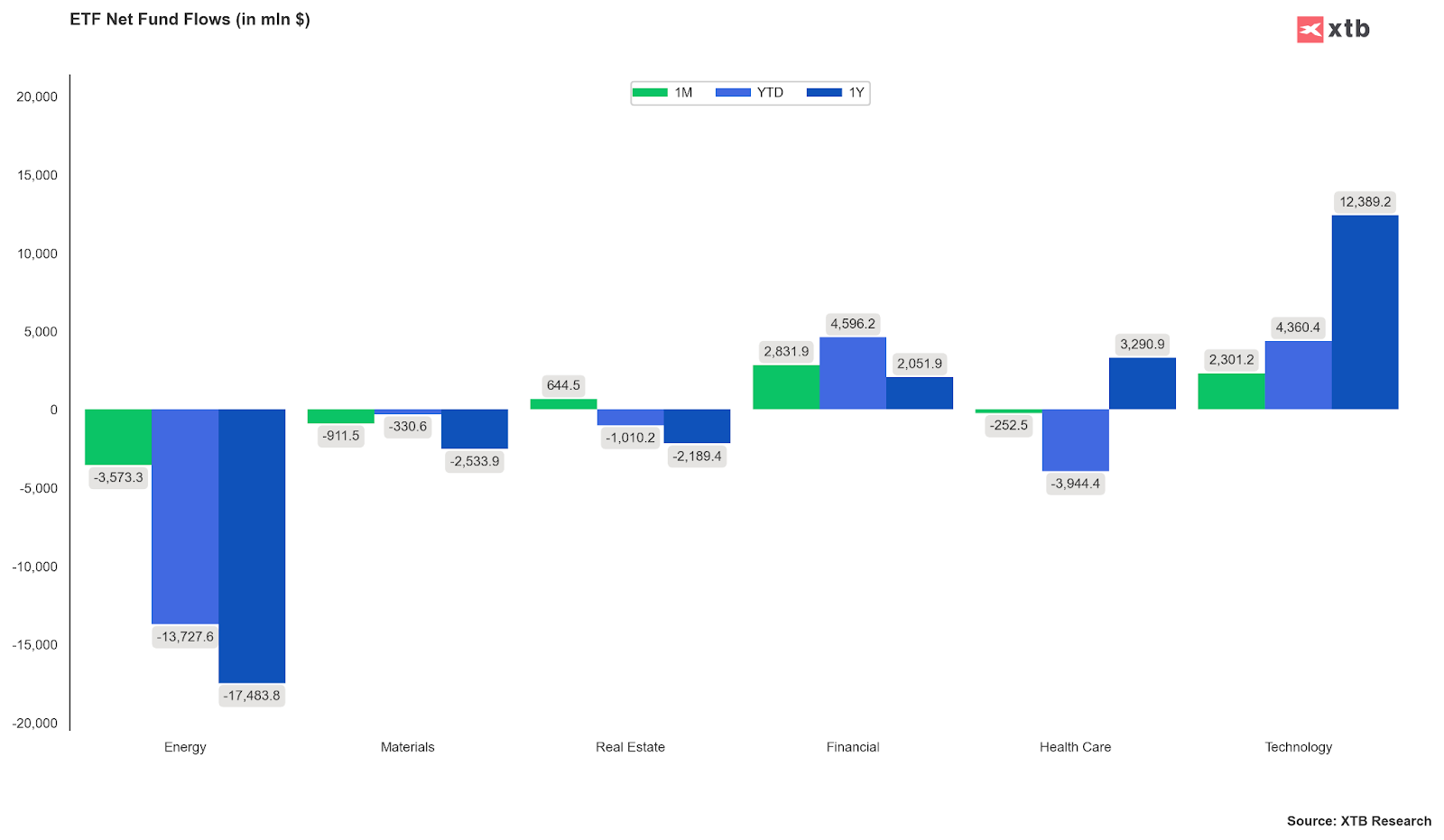

Net inflows into technology ETFs have accelerated significantly recently, coinciding simultaneously with a complete pullout of funds from energy ETFs. More than 400 of the world's largest technology ETFs (mostly U.S. and Asian) have attracted net inflows of more than $12 billion over the past year, while more than $17 billion has been pulled net from more than 300 energy funds. By comparison, it can be seen that other sectors such as real estate, materials, and health care were not popular. Only the financial sector credited fairly sizable inflows, although smaller than those of technology companies.

Net flows among the world's largest equity funds. Source: Bloomberg, XTB

A few examples are worth mentioning. The iShares S&P 500 Information Technology (IUIT.UK) and iShares Nasdaq UCITS (CNDX.US), which are among the most popular ETFs in the world, are also doing great, boasting an annual change of 37% and 30%, respectively. It is important to note, however, that the largest shares in these ETFs are held by the most well-known companies such as Apple, Microsoft and Nvidia. The share of smaller companies that have been the stars of the artificial intelligence rally (such as C3.AI, which has gained almost 300% since the beginning of the year) is negligible. Indirectly, the euphoria of the Nasdaq and the weaker U.S. dollar has lent itself to emerging markets, including India, where technology companies like Saksoft and Cyient have a sizable share in the indexes. As you can see, ETFs offer exposure, even to such exotic markets - since the March low, iShares MSCI India (NDIA.UK) has already gained more than 15%, and the year-to-date outlook is up about 10%.

Opportunities and threats

It's worth noting that since the beginning of the year, the euphoria around technology has taken place in an environment of sleaze in the stocks of companies from other segments of the economy. Capital outflows are being recorded by ETFs on energy companies, which were doing well in 2022. The prospect of a recession and lower commodity prices, including oil (Brent crude has lost 15% year-to-date, and is down more than 40% in compare with June 2022) are discouraging investor exposure to the industrial-energy sector. The rally of technology companies, however, has been tremendous, and without the 'magnificent seven' the S&P500, would be trading at January levels. In the time since the beginning of the year, while oil has been losing, the Nasdaq has risen nearly 40%.

In view of this, some investors may be looking for exposure to ETFs that mitigate the risk of a possible correction of the largest (technology) companies in the index, but still offer exposure to the broad equity market. Such ETFs equalize the share of all companies in the index, for example, XTrackers Equal Weight S&P500 (XDEW.UK). Since the beginning of January, this fund has seen record inflows of up to $700 million ($127 million in the second week of June). The inflow of capital into the "safer" ETF is because investors are concerned about the growing influence of technology companies, whose share of the S&P or Nasdaq 100 index is overwhelming. In the event of a recession or further increases in interest rates, capital can be expected to start migrating to sectors where passive investors currently have less exposure.

The primary threat to technology ETFs today is the risk of an economic slowdown, which could significantly 'cool' the euphoria. In addition, inflation in many countries, including the U.S., could prove more anchored, prompting central banks to tighten monetary policy further and ultimately - a deeper slowdown. Higher interest rates may prompt investors to look for a safe way to allocate capital and reduce borrowing for investments in the stock market (i.e., margin). For the moment, the base scenario in the U.S. is a 'soft landing', i.e. no or very shallow recession. This is a very positive scenario for the stock market, but does not necessarily appear to be the most likely one.

Live Trading - 2026.02.10.

A nap chartja 🗽

🌍 Gyorsjelentési szezon az XTB-vel

🌍 Gyorsjelentési szezon az XTB-vel

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.