New York Fed chief John C. Williams and Lisa D.Cook of the Federal Reserve Board commented today on the US monetary policy situation:

Fed Williams

Kezdjen befektetni még ma, vagy próbálja ki ingyenes demónkat

Élő számla regisztráció DEMÓ SZÁMLA Mobil app letöltése Mobil app letöltése- Fed policy is not very restrictive at the moment although overall I see that financial conditions have tightened;

- The Federal Reserve may need to maintain a restrictive monetary policy even for several years;

- If financial conditions loosen too much, as expected by the Fed's outlook, the Fed will have to raise interest rates;

- There are many indications that the U.S. economy is becoming more resilient but we may slow down rate hikes now as we are closer to the peak. If the situation changes, however, we may move faster than 25 bps;

- 25 bps rate hikes seem to be the best option for now. Currently, however, a target rate of 5%-5.25% is a reasonable target;

- Maybe service prices will remain high, and if that happens, we will need higher rates. Demand for services as well as labor is still very high, demand in the economy is stronger than usual;

- There is a lot of uncertainty around the outlook for inflation, it may prove to be more persistent for some reasons;

- So far, commodity prices are falling but there is a long way to go before a further decline. However, inflation driven by the rental market is weakening, and the housing sector is clearly slowing down;

- The labor market is extremely tight, and it is unclear whether and by how much unemployment will rise. With a strong economy, job growth may continue to rise.

Fed Cook

- The data paint a clear picture of a strong labor market with persistently high inflation. The cycle of increases is not over yet;

- Inflation is still too high despite the decline, the Fed will maintain a restrictive monetary policy for a long time;

- It is possible that the upward path of the unemployment rate will be lower than the latest Fed forecasts. I believe that inflation can be contained without a large increase in unemployment;

- The combination of a strong labor market and falling wages and prices has raised hopes of a soft landing. I expect inflation to continue to decline this year and next, although progress may be uneven

- Lower rate hikes are more appropriate now, as the Fed assesses the cumulative impact of past hikes;

- The Fed has seen improvement but needs to pay attention to a lot of data. In 2023, U.S. GDP growth seems most likely today though I expect it to be below average.

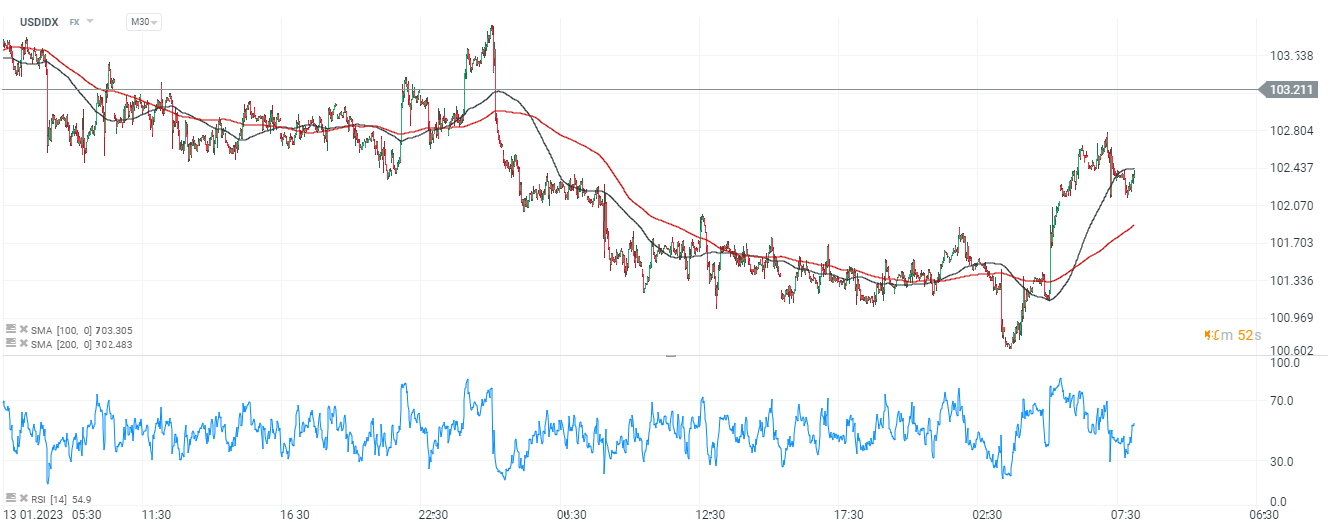

The USDDIDX Dollar Index reacted with an initial rise to Williams' comments, but supply came to a head near the SMA100 average (black color) and is attempting to pull back the 'greenback'. Source: xStation5

The USDDIDX Dollar Index reacted with an initial rise to Williams' comments, but supply came to a head near the SMA100 average (black color) and is attempting to pull back the 'greenback'. Source: xStation5

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.