A combination of 'risk appetite' sentiments fueled by hope around a 'helpful Fed' and banking sector problems has put downward pressure on the US dollar and a rally on EURUSD. Following the bankruptcy of three US banks Silvergate, Signature, Silicon Valley Bank (now we now that,First Republic Bank also joined this trio) the Federal Reserve, the Treasury Secretary and the National Economic Council reached an agreement with banking regulators. The institutions decided to help depositors through liquidity programs and created an instrument so that banks would not have to realize losses on bonds to cover payouts. Indexes and cryptocurrencies reacted with a dynamic rally to the regulators' effort to provide more details before markets opened in Asia to prevent panic and stop a potential domino effect.

Index futures ignored news of Signature Bank's collapse, and declines in the eurodollar took their toll. EURUSD gains were supported by today's comments from Goldman Sachs, which does not expect the Fed to keep rates unchanged at its upcoming March 22 meeting. According to analysts, the regulators' decisions will increase liquidity in the banking sector and improve depositor confidence. At the same time, Goldman reiterated expectations for a 25bp hike in May June and July, still sees the final rate in the 5.25 - 5.5% range

Kezdjen befektetni még ma, vagy próbálja ki ingyenes demónkat

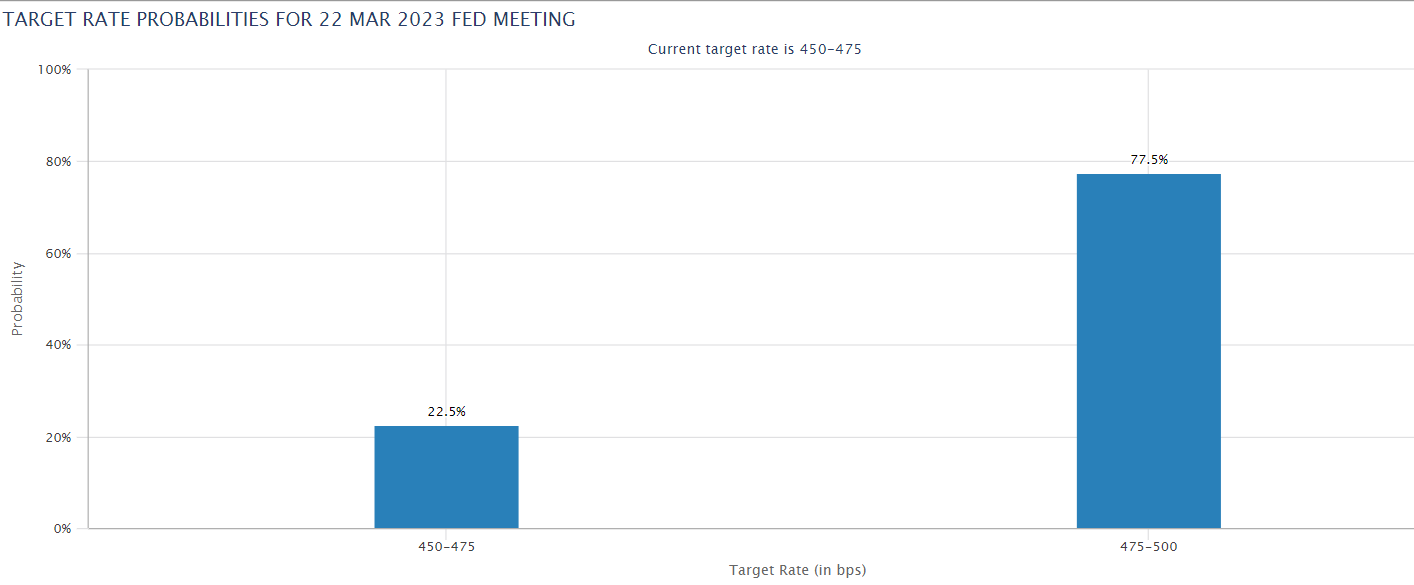

Élő számla regisztráció DEMÓ SZÁMLA Mobil app letöltése Mobil app letöltése The market has sharply reduced expectations for the amount of a Fed rate hike on March 22. It now sees a 22,5% chance of no hike and a 77,5% chance of a 25 bp hike. Before to the banks' collapses, a narrative of 50 bp prevailed. Source: CME, FedWatch

The market has sharply reduced expectations for the amount of a Fed rate hike on March 22. It now sees a 22,5% chance of no hike and a 77,5% chance of a 25 bp hike. Before to the banks' collapses, a narrative of 50 bp prevailed. Source: CME, FedWatch

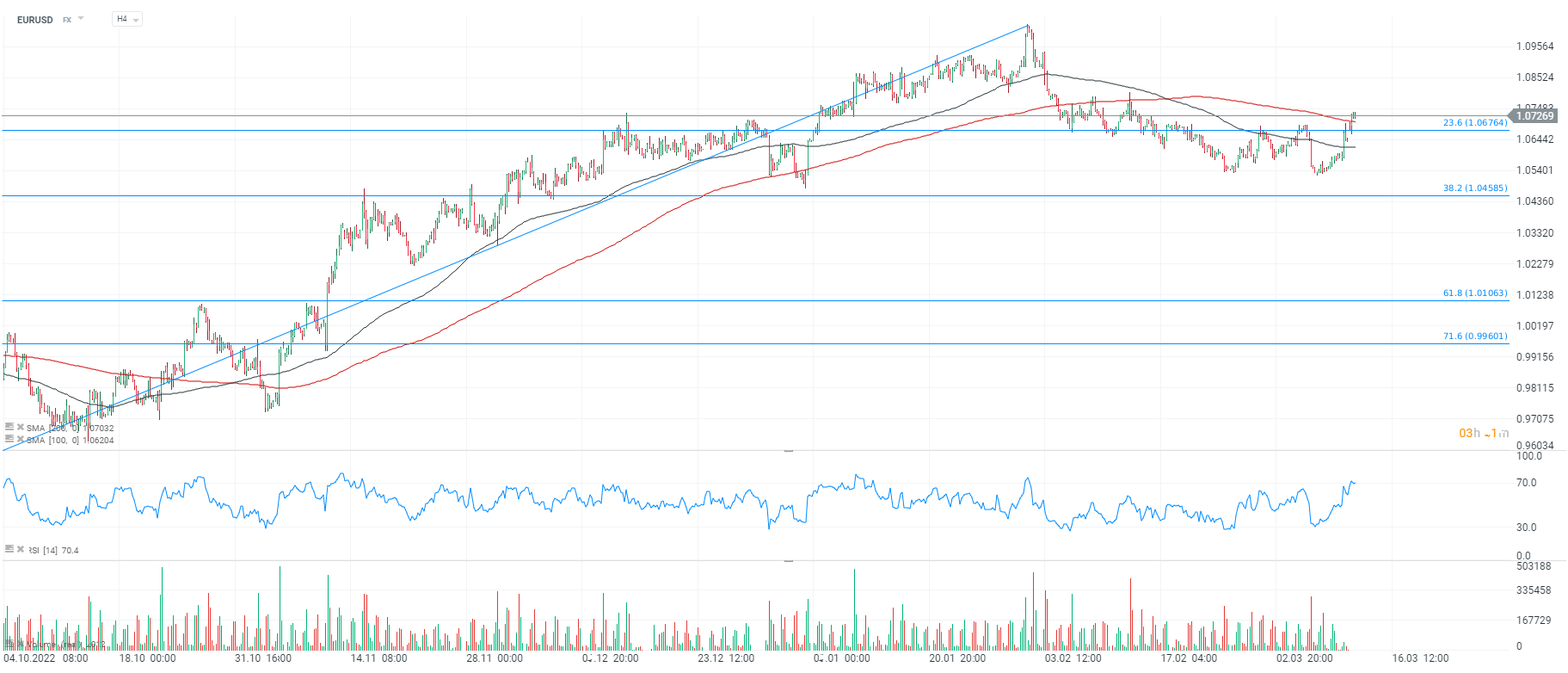

EURUSD chart, H4 interval. The dollar has weakened mightily since March 8, the EURUSD exchange rate returned above 1.07. The market reacted positively to the Fed's support. The price climbed above the 23.6 abolition of the upward wave started in September 2022 and the 200-session average SMA200 (red line). Looking at the volume candles, that the dollar's prolonged weakness is supported by considerable volume signaling the markets' hopes for the end of the Federal Reserve's rate hike cycle while maintaining a hawkish stance at the ECB, which has started raising rates of late. Source: xStation5

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.