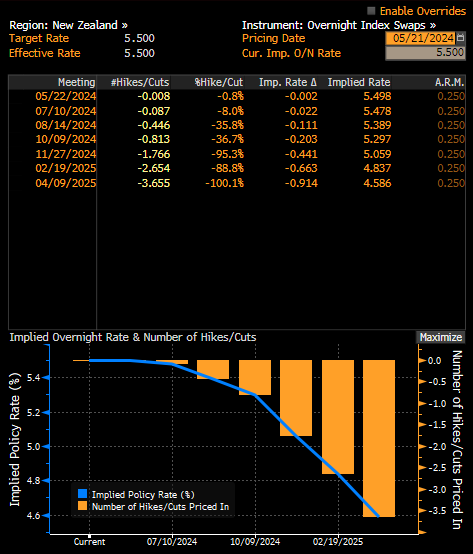

The market is not pricing in any interest rate change from the RBNZ at tomorrow's meeting, during the Asian session. In fact, the market is not pricing in any move from the Reserve Bank of New Zealand until as late as November this year. In fact, that's when a full cut is priced in, although there is a combined chance that rates could be cut in October.

Expectations for tomorrow show that RBNZ will keep interest rates unchanged but may soften its stance. The market is not pricing in the first possible cut until October, although the probability could increase after any dovish commentary, which could open the door for cuts to begin in August. Source: Bloomberg Finance LP

What are the predictions?

- It is suggested that the RBNZ will be the first to communicate the possibility of a cut this year, getting ahead of the RBA. The RBA may not start cutting until 2025.

- The New Zealand economy is very weak. Q3 and Q4 2023 saw quarterly declines, which means a technical recession.

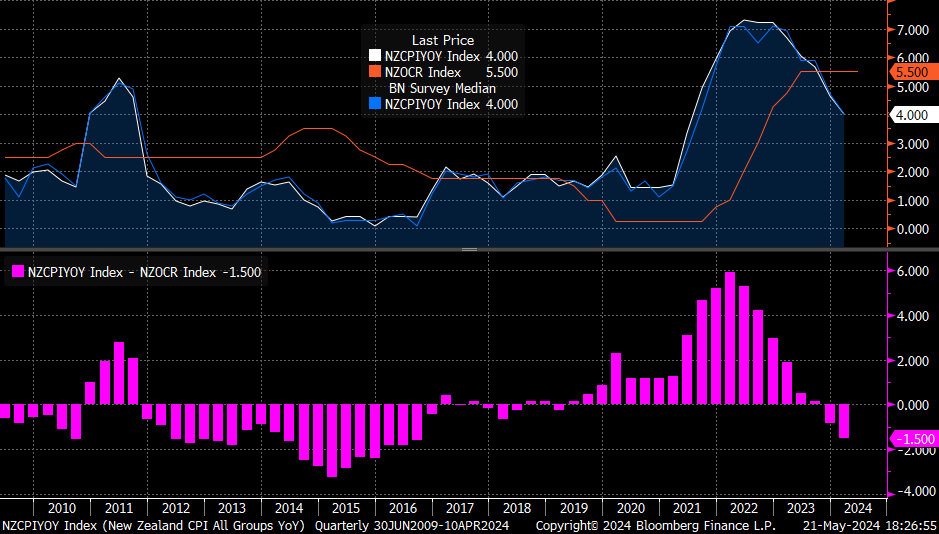

- New Zealand inflation is falling, although it was hoped that inflation could fall a bit more in Q1 and came in line with expectations. The difference between inflation and rates is not yet as wide as it was in 2015 when the rate cut cycle began.

- The real rate has only been positive for two quarters.

- Since the RBNZ's last meeting in April, inflation expectations have fallen to their lowest in almost three years, and the unemployment rate has edged higher. This opens the door to a somewhat more dovish stance.

Difference between interest rate and inflation in New Zealand. Source: Bloomberg Finance LP, XTB

Difference between interest rate and inflation in New Zealand. Source: Bloomberg Finance LP, XTB

How could AUDNZD react?

If there is indeed dovish communication from the RBNZ, then the pair could again break above 1.10. Of course, we are observing an interesting situation in which AUDNZD is at the upper limit of its multi-year consolidation. On the other hand, we have recently seen significant increases in industrial metal prices, which should benefit the Australian economy, although there is no significant correlation between AUDNZD and copper.

Source: xStation5

Daily summary: Weak US data drags markets down, precious metals under pressure again!

BREAKING: US RETAIL SALES BELOW EXPECTATIONS

Takaichi’s party wins elections in Japan – a return of debt concerns? 💰✂️

Three markets to watch next week (09.02.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.