Key points for investors ahead of this week's crucial session, when the market will learn the latest US CPI data:

-

The market expects inflation pressure to remain elevated, with the main reading showing a year-over-year price increase of 2.9% compared to the previous reading of 2.7%.

-

Core inflation is expected to maintain the current price growth rate at 3.3% y/y.

-

Yesterday, the market learned that producer inflation data came in lower than expected, which is somewhat correlated

-

The Japanese yen is gaining today following hawkish comments from BoJ's Ueda

-

Lower US CPI data could increase the scale of this appreciation further

-

Trump's announcement regarding sudden tariff increases remains an element of uncertainty in creating dollar demand

Investors face a key session of the week, with US CPI data due at 14:30. The USDJPY pair is losing nearly 0.7% today, which is related to the low US PPI reading and hawkish comments from the BoJ president.

PPI Data:

-

PPI indicator: actual 3.3% y/y; forecast 3.5% y/y; previous 3.0% y/y;

-

Core PPI indicator: actual 3.5% y/y; forecast 3.8% y/y; previous 3.5% y/y;

Producer inflation in December failed to meet pro-dollar expectations. Both the general and core readings came in below forecasts (3.3% and 3.5% y/y respectively), slightly weakening hawkish investor expectations regarding US monetary policy in 2025.

Ueda's Statement:

President Kazuo Ueda's comments intensified speculation about a potential rate hike at next week's meeting (January 23-24). The president emphasized promising wage talks from the beginning of the year and recent meetings with branch directors, marking a significant change in communication strategy. These comments, following similar forward-looking statements from Vice President Himino, caused the Japanese yen to strengthen.

Overnight index swap contracts now indicate a 71% probability of a rate hike this month, up from 60% earlier in the day, reflecting growing market conviction. Source: Bloomberg Financial LP

Yield Dynamics

Japanese government bonds came under selling pressure, with 2-year bond yields reaching their highest level since 2008 (0.7%), and 30-year bond yields reaching a new peak since 2009. The BOJ's rinban operation noted increased sales, putting additional pressure on JGB futures.

What will the Fed do after CPI?

The US bond market, due to better economic data, has started pricing in a hawkish FOMC pivot and one rate cut in 2025. This translated directly into strengthening of the American currency, with the dollar index rising by 2.5% in just the last month.

Overnight index swap contracts suggest a 32 basis point cut in 2025, slightly more than one cut. Source: Bloomberg Financial LP

Yesterday's PPI came in better than expected, giving Wall Street hope for continued looser policy. Historically, PPI and CPI are correlated, but PPI is a measure more dependent on fuel prices, while CPI is influenced by various other factors (such as food prices, car prices, and rents).

Car prices are showing a return to price increases - so far small, but this factor will stop pulling overall inflation down in the medium term. Source: XTB

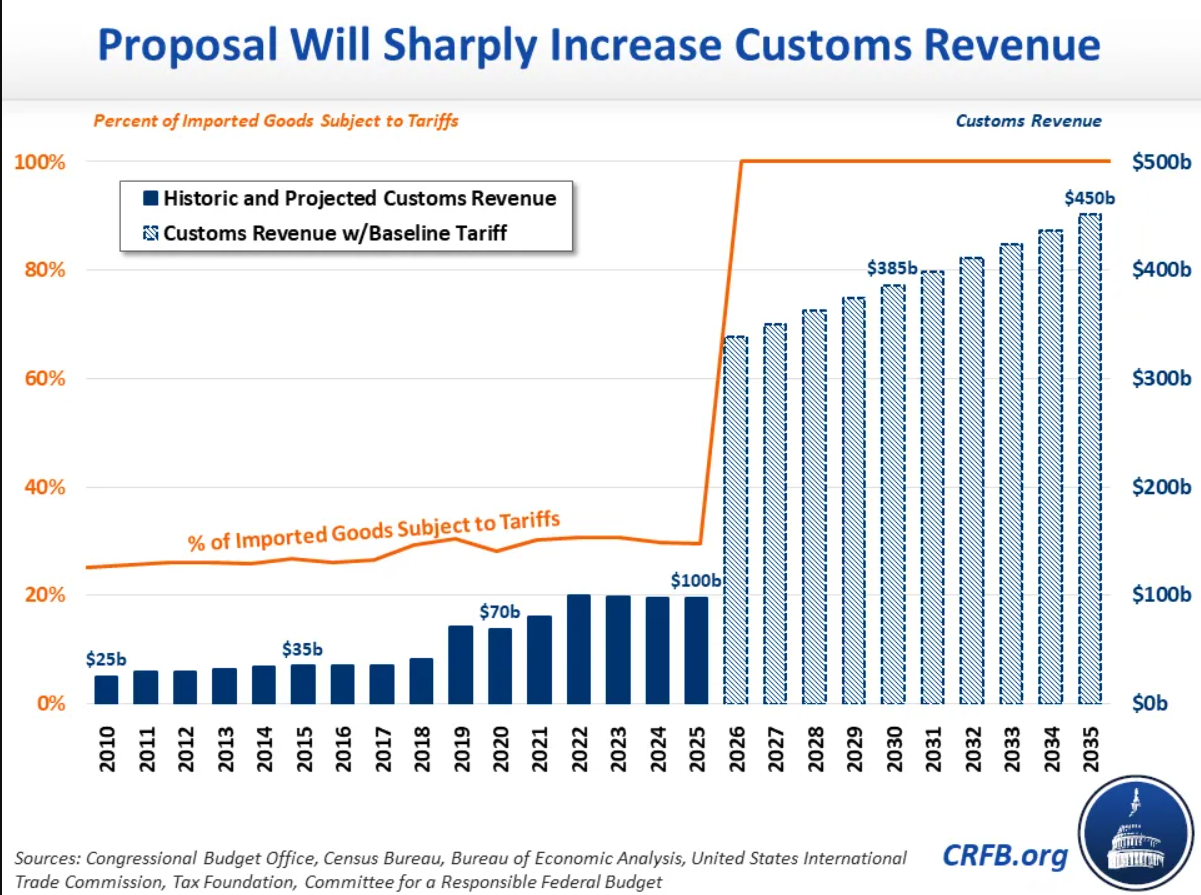

Trump as the "Wild Card" in the Inflation Puzzle

Any reaction in dollar-related pairs may not be long-lasting, however, as the main topic creating market uncertainty in the long term is Trump's policy regarding dynamic tariff increases. At this point, any rumors suggesting a more gradual model of their implementation were quickly denied by Trump himself, which is why markets are increasingly concerned about how the new policy will translate into inflation and thus future Federal Reserve decisions.

The market expects a jump in tariff rates and the revenue they generate for the government treasury. Source: CRFB

USDJPY (D1 Interval)

USDJPY has entered a critical zone associated with previous currency interventions. After today's comments, the pair fell below the 15-day EMA and slightly below the 78.6% Fibonacci retracement level from the downward movement. Key targets for bears include the 30-day EMA and 50-day EMA, followed by the 23.6% Fibonacci retracement level from the upward movement at 154.272. The RSI indicator signals bearish divergence, suggesting weakening upward momentum, while MACD confirms bearish sentiment. Source: xStation

Daily Summary - Powerful NFP report could delay Fed rate cuts

BREAKING: US100 jumps amid stronger than expected US NFP report

Economic calendar: NFP data and US oil inventory report 💡

Morning Wrap: Dollar in a trap, all eyes on NFP 🏛️(February 11, 2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.