Will Fed cut rates the last time in this cycle? 💵 Markets await FOMC decision at 7 PM GMT

The US Federal Reserve decision will be announced at 7 PM GMT today, while the Fed chair Jerome Powell press conference will begin half an hour later. However, at 7 PM GMT, in addition to the level of interest rates and the statement, we will also learn the latest macroeconomic projections, along with the famous dot-plot chart, which shows the expectations of U.S. central bankers on future interest rate levels. The latest data from the U.S. economy has added a rather confident edge to today's market. Key to the reaction, however, will be what happens next year with rates. There has been a lot of talk recently about a “hawkish” cut and holding off on reductions for a while. But is there a chance that today's cut will be the last in the cycle?

Market expectations

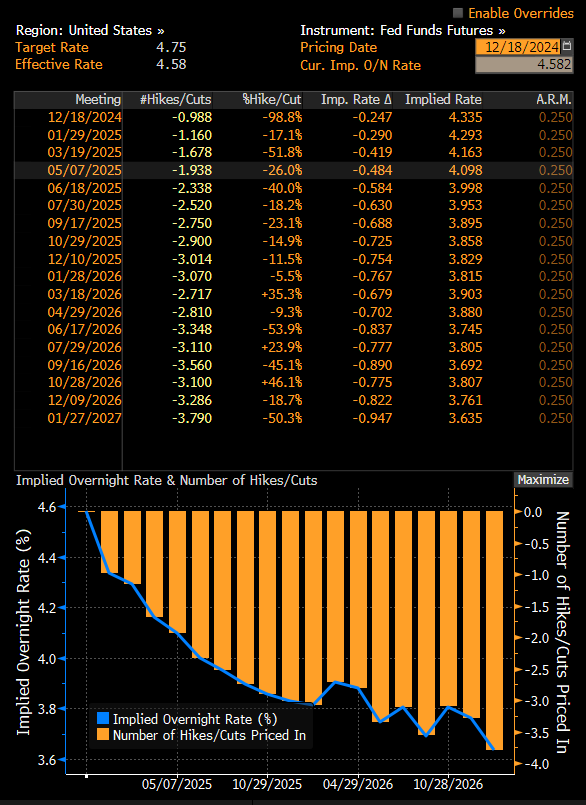

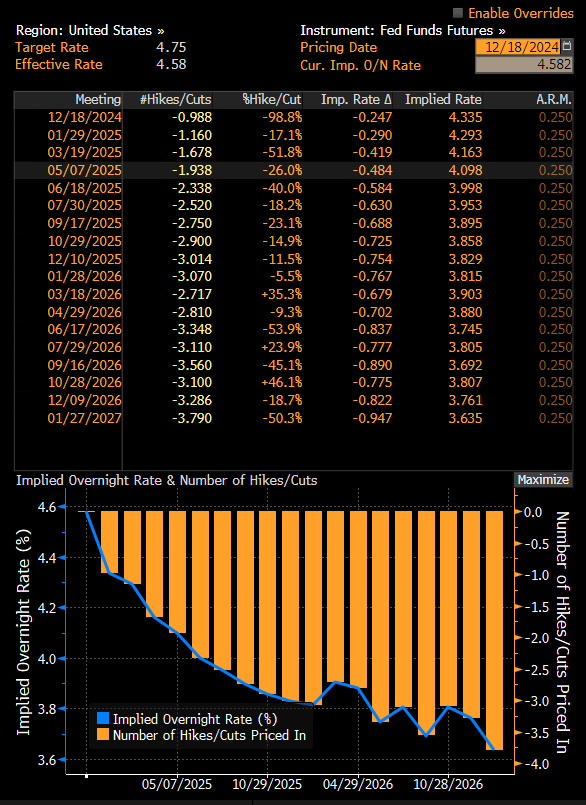

CPI and core CPI inflation rebounded for November, in line with market expectations. Nevertheless, we did not observe a major surprise, which most likely reinforced policymakers' view that today's cut will be justified. The market sees a 99% probability for today's cut. The situation is definitely more interesting later on:

Start investing today or test a free demo

Open real account TRY DEMO Download mobile app Download mobile appThe market sees only a 17% probability for a hike in January

For March 2025, the probability of a hike is 52%, and combined with January's is just under 68%

For June 2025, an incomplete combined cut is still priced in!

Market expectations for interest rates next year. Source: Bloomberg FInance LP

The market has changed its attitude quite dramatically. Just a few months ago, it expected rates at 3% in mid-2025. Now a rate of 4.0% is expected in the middle, while by the end of next year rates could reach a minimum of 3.75%.

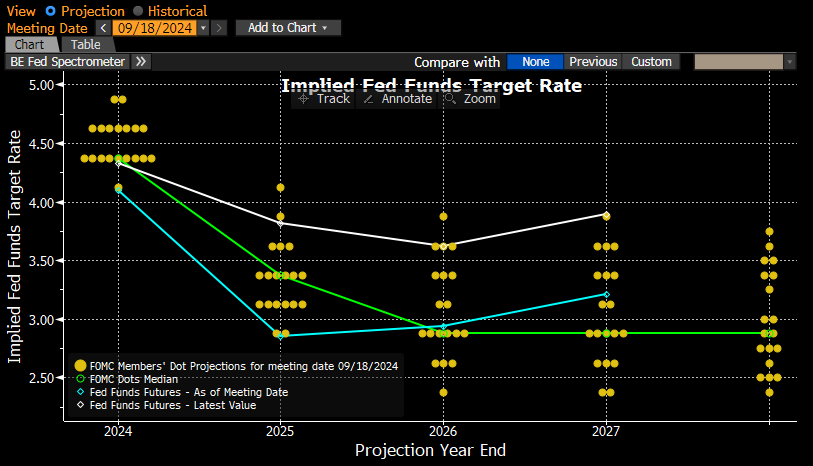

How the market views the future is very important. The curve for rate futures has risen dramatically compared to the previous meeting. One might suspect that the bankers' expectations themselves will change quite a bit.

- The median for next year pointed to 3.4%, while the median for 2026 (as well as for 2027 and the long term) pointed to 2.9%. Assuming today's cut, the main range for rates would be 4.5%, which would put the outlook for 3 cuts next year. We expect the Fed to reduce its expectations by at least one cut for next year.

- No change would be viewed dovishly by the market. Nonetheless, it is indicated that if inflation were to be raised to 2.5%, and the neutral real interest rate were assessed at 1.75%, then a nominal neutral rate of 4.3% could be priced in. This would suggest that today's move in rates could be the last. While this is not the baseline scenario, such a scenario cannot be ruled out.

Dot-chart will most likely show less expected rates for 2025 and 2026. Source: Bloomberg FInance LP

What will the macro forecasts show?

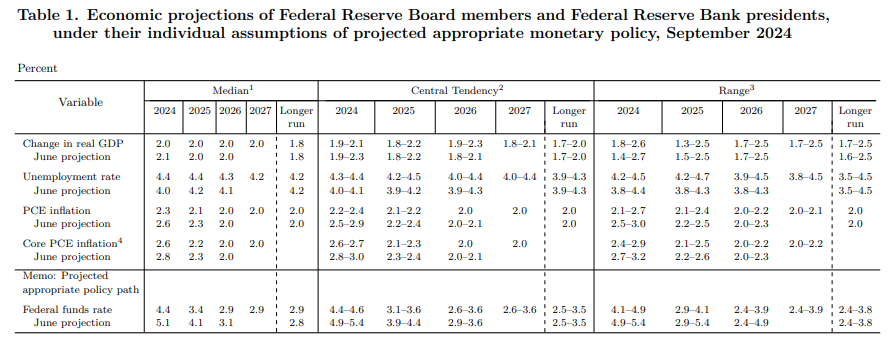

Next year is uncertain due to Trump's policies. Protectionist policies will lead to loose fiscal policy, which could lead to higher inflation. GDP growth has been solid this year, so the Fed can potentially afford to hold off on cuts for longer. If forecasts show stronger growth for next year than 2.0%, this could suggest a more restrictive approach by the Fed. The same will apply to inflation. Recently, the core inflation projection was lowered to 2.2% for 2025. However, if it is raised to 2.5%, that would imply a higher neutral interest rate. The Fed still sees a return to target in 2026 at this point. The change in forecasts may suggest a more hawkish approach going forward.

September macroeconomic forecasts. Source: US Federal Reserve

How will the market react?

A theoretically hawkish cut, i.e. a suggestion that another cut will have to wait, could lead to a temporary sell-off on Wall Street and a strengthening of the US dollar. Yields on 10-year bonds rose to 4.4%, suggesting that the market expects higher neutral interest rates. However, could higher rates be a hindrance to Wall Street? Not necessarily.

The current time compares to 1996 and 2019. Back then, the cycles of cuts consisted of 3 moves (of course, in 2020 we had a pandemic and we don't count those cuts). Despite the pause in cuts at these two points in time, the S&P 500 has risen in the first case by more than 30% since the last cut, while in the second case by 12% (here, of course, everything stopped by pandemics).

S&P 500 and interest rates in the US. Source: Bloomberg Finance LP, XTB

If the economy is strong and the new administration's actions support US companies, this should benefit the main index, although of course, in the short term itself, a correction cannot be ruled out. In addition, the mere pause in reductions could be good for the dollar, which could lead the EURUSD below parity next year.

The US500 is defending an important support at 6050 points. In addition to this, after today we will have a rollover, at the level of about 70 points up. If the Fed is hawkish today, a correction cannot be ruled out. On the other hand, the price will open higher tomorrow, and in addition we have support at the level of 6000 points and an upward trend line. In view of this, it cannot be ruled out that we will see Santa Claus in the stock market later this year and new historical peaks will be tested. Source: xStation5

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.