While natural gas isn't dominating headlines as it did in 2022, when European prices soared past €300 per megawatt-hour, current prices are several times lower, yet still significantly higher than the levels seen just a few years ago. However, Americans continue to enjoy the benefits of cheap gas. Consumer prices, while distinct from prices on commodity exchanges, are still a fraction of those in Europe. However, the US landscape is shifting. While the US president Donald Trump wants to pursue an "drill baby drill" approach to maximize oil and gas production, domestic demand is surging, and export ambitions are growing. Simultaneously, Europe's gas needs may be on the rise. Could this signal the end of cheap gas in the US, sacrificed for international expansion?

Declining Russian Supplies: A Real Shift?

Before the Ukraine war, Russia was Europe's undisputed leading natural gas supplier, primarily via pipelines. The conflict drastically altered this dynamic, virtually halting pipeline deliveries. Yet, Europe remains a significant buyer of Russian LNG. 2024 saw record-high Russian LNG imports, even as US deliveries declined. Russian gas, including its liquefied form, is simply cheaper, a fact exploited by major European economies. The EU aims to curtail this practice, potentially opening doors for other suppliers, notably the United States.

The US: An LNG Powerhouse

About one year ago, the US export capacity hovered around 12 billion cubic feet, but now frequently surpasses 15 billion. The US Energy Information Administration (EIA) forecasts North American LNG export capacity to double to 24.4 billion cubic feet by 2028. The US intends to leverage its potential, capitalizing on higher prices abroad.

EIA indicates that export capacity from North America could double. Source: EIA

Europe's gas needs remain, amidst green deal questions and depleted stockpiles. Donald Trump has urged Europe to increase LNG imports to address the substantial trade deficit. A timely opportunity arises as Europe, having depleted gas reserves earlier this winter, likely seeks to diversify away from Russian supplies.

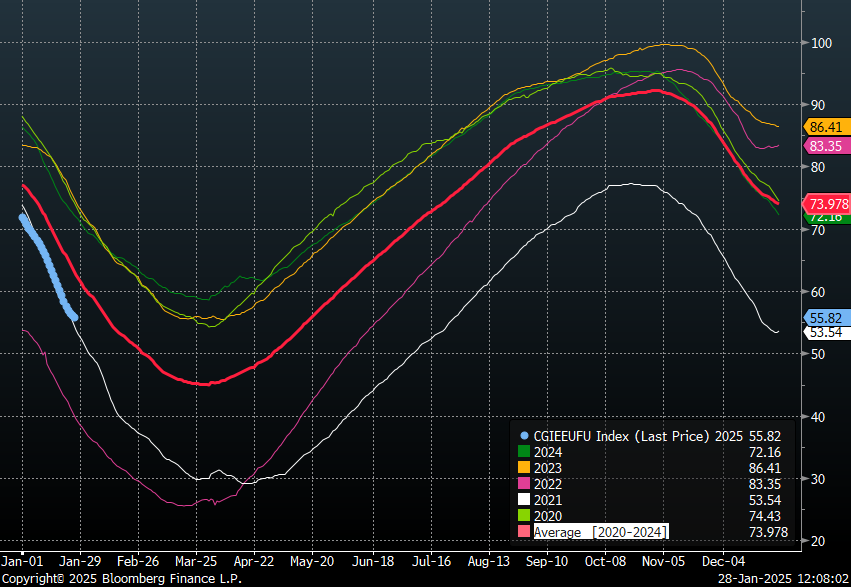

European storage levels currently stand at roughly 55%, below the 5-year average, echoing the situation in 2021 when Russia began reducing deliveries. Reaching the target 90% storage capacity by early November will necessitate increased US imports. Source: Bloomberg Finance LP, XTB

Weather's Influence

Cold spells at the turn of the year in both the US and Europe intensified heating demand. The preceding two years saw subdued gas consumption. Consequently, prices in both regions climbed. However, weather patterns are volatile, and indications suggest the worst of winter might be behind us. Europe, however, faces a different reality, still grappling with constrained supply and prices above €50/MWh. In contrast, US prices have already retreated almost 30% from their seasonal peak. Should last year's trend repeat, a 40-50% decline from the price zenith is plausible, potentially revisiting the $2.2-2.5/MMBTU, a range that was seen last autumn.

Price Outlook

European and Asian prices remain multiples higher than those in the US. Factoring in transport and liquefaction costs, the gap between global benchmarks and US prices would narrow considerably. Yet, increased US export capacity will tighten domestic supply. While production growth potential exists, local demand is also poised to increase, driven by the rise of AI infrastructure. Donald Trump has suggested US energy needs could double in the coming years, with gas-fired plants accounting for over 40% of US electricity generation. This could lead to a squeeze on domestic supply amidst rising demand, inevitably driving prices upwards. This is partly reflected in the forward curve, projecting prices of $4.5-4.6 by next January, though these levels could be reached sooner. The upcoming summer is forecast to bring extreme temperatures, further straining US energy needs and potentially limiting stock replenishment ahead of the next heating season. The question then becomes: Is this the twilight of cheap American gas?

Daily summary: Silver plunges 9% 🚨Indices, crypto and precious metals under pressure

🚨Gold slumps 3% amid markets preparing for Chinese Lunar Year pause

Cocoa falls 2.5% to the lowest level since October 2023 📉

NATGAS muted amid EIA inventories change report

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.