Interest rates in the US were cut as expected to 4.5%, while macroeconomic forecasts and interest rate expectations changed quite noticeably. The Fed is also changing its communication somewhat in the statement, and one Fed official (Cleveland Fed president, Beth Hammack) is holding off on the decision to cut.

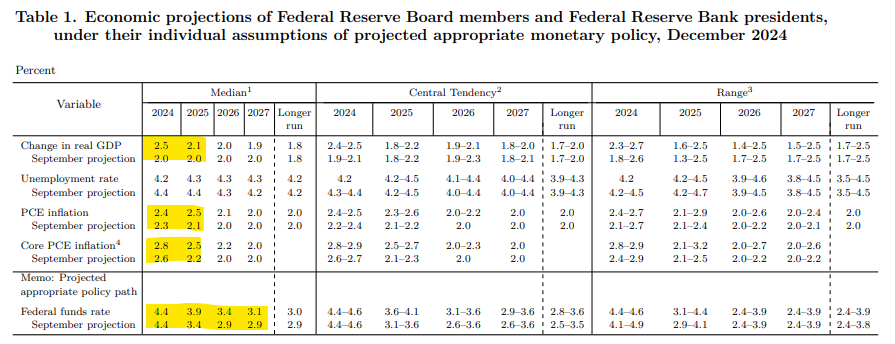

Quite a bit of change in macroeconomic forecasts. We can see higher assessments of inflation, slightly higher assessments of economic growth and a markedly higher outlook for interest rates. Source: the Fed

The Fed's statement indicates that it is considering a longer period of time before its next decision to adjust interest rates. The committee will carefully evaluate incoming data, the changing outlook and the balance of risks. The Fed explicitly raises interest rate forecasts:

- 3.9% for 2025 (up from 3.4%)

- 3.4% for 2026 (up from 2.9%)

- 3.1% for 2027 (up from 2.9%)

- 3.0% for the long term (up from 2.9%)

- The Fed raised its 2025 GDP growth target to 2.1% y/y from 2% in September

- It also significantly raised its forecast for PCE inflation in 2025; it estimates it at 2.5%, up from 2.1% in September (before the election). The baseline is expected to be 2.5%, it was previously expected to be 2.2%

- The unemployment rate in 2025 is expected to be 4.3%; the Fed previously expected 4.4%. So the Federal Reserve does not see a significant increase in unemployment from current levels.

- The Fed also raised the long-term rate to 3% from 2.9% previously, and estimates a 50 bp cut in rates next year and in 2026

The tone of the projection is very hawkish, and seems to support the narrative of no, or very few, rate cuts in 2025. It is worth noting, however, that circumstances could still change, the Trump administration will take office in the US, in the second half of January. If the tariff policy turns out to be as 'aggressive' as Trump sees it, the dollar seems to have even more room to rise.

In response, we have seen a very strong decline in the EURUSD pair, which started its declines from levels near 1.0500, while levels near 1.0400 are now being tested. There has also been a clear limit to the rise on the US500. If further forecasts point to greater inflation risks, there is a chance that today's cut was the last, which strengthens the potential for the EURUSD pair to fall near parity next year.

EURUSD could close today at its lowest since 2022. Nevertheless, there is still a press conference ahead. Source: xStation5

Daily Summary - Powerful NFP report could delay Fed rate cuts

Daily summary: Weak US data drags markets down, precious metals under pressure again!

BREAKING: US RETAIL SALES BELOW EXPECTATIONS

Takaichi’s party wins elections in Japan – a return of debt concerns? 💰✂️

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.