Euro gains slightly ahead of ECB interest rate decision 🏛️

The ECB's interest rate decision will be published at 1:15 pm GMT., while the press conference will begin at 1:45 pm GMT. The consensus clearly points to a 25 basis point cut, although theoretically a similar surprise as was the case with the SNB cannot be ruled out. A cut of 50 basis points does not seem to be the baseline scenario, nevertheless, for the euro, the macroeconomic projections, which will answer us how low interest rates may go next year, may be definitely more important.

What to watch for in today's ECB decision?

Start investing today or test a free demo

Open real account TRY DEMO Download mobile app Download mobile appThe ECB is unlikely to surprise today and decide to cut interest rates by 25 basis points. By far the greater room for surprise lies in the macroeconomic projections and communications from the bank. The September forecast points to inflation at 2.2% for 2025. However, there is considerable room to cut this forecast even to 1.7%. All forecasts of 2.0% and above would be positive for the euro, in the opposite case negative. The outlook for growth itself will also be important. Currently, the market sees growth at 1.3% next year, while the weakness of the European economy presented by the PMI indicates that the growth projection may be lowered below 1%.

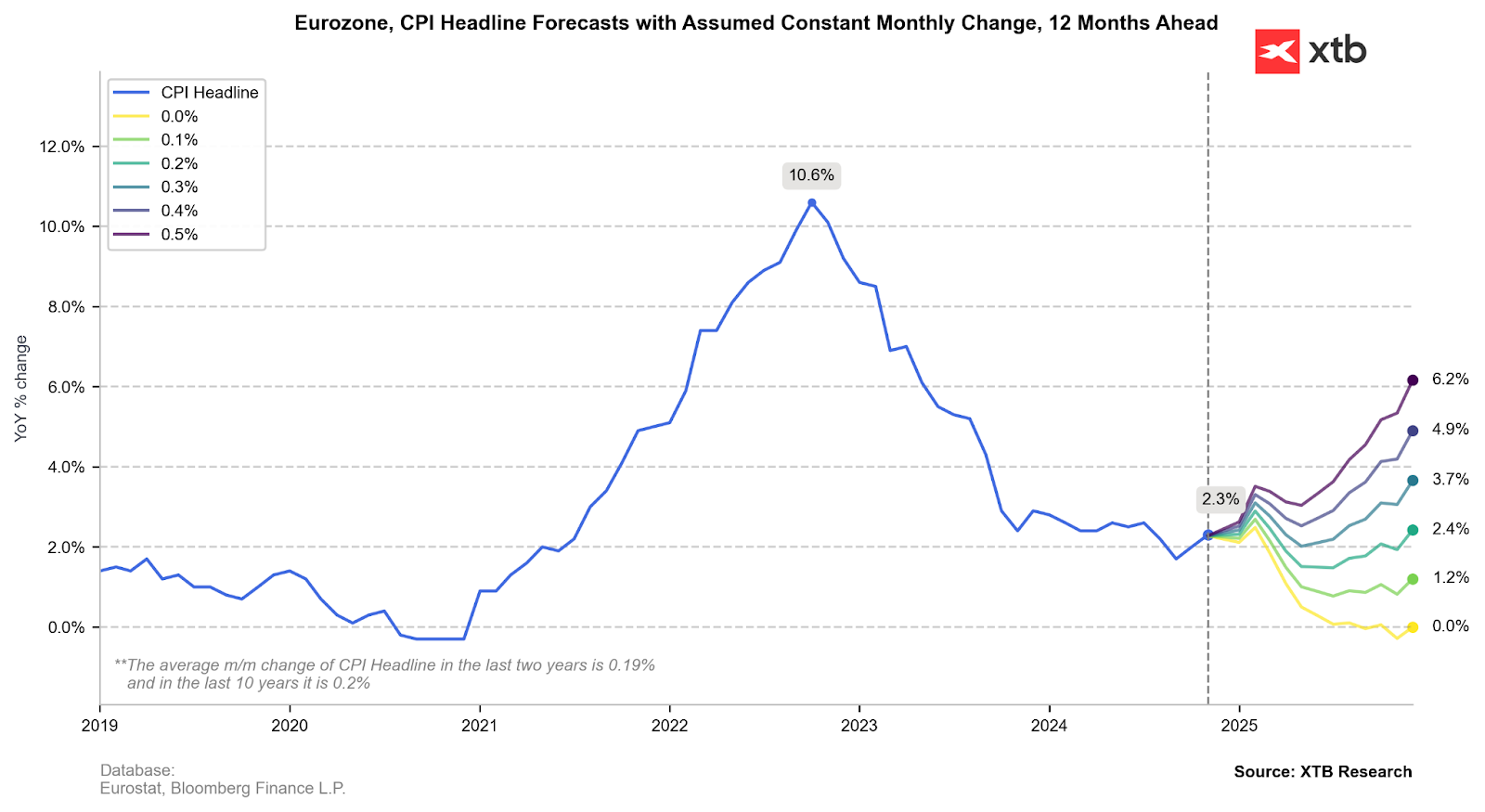

The path of monthly average inflation at 0.2% would suggest a fairly pronounced slide below 2% in the second half of next year. Source: Bloomberg FInance LP, XTB

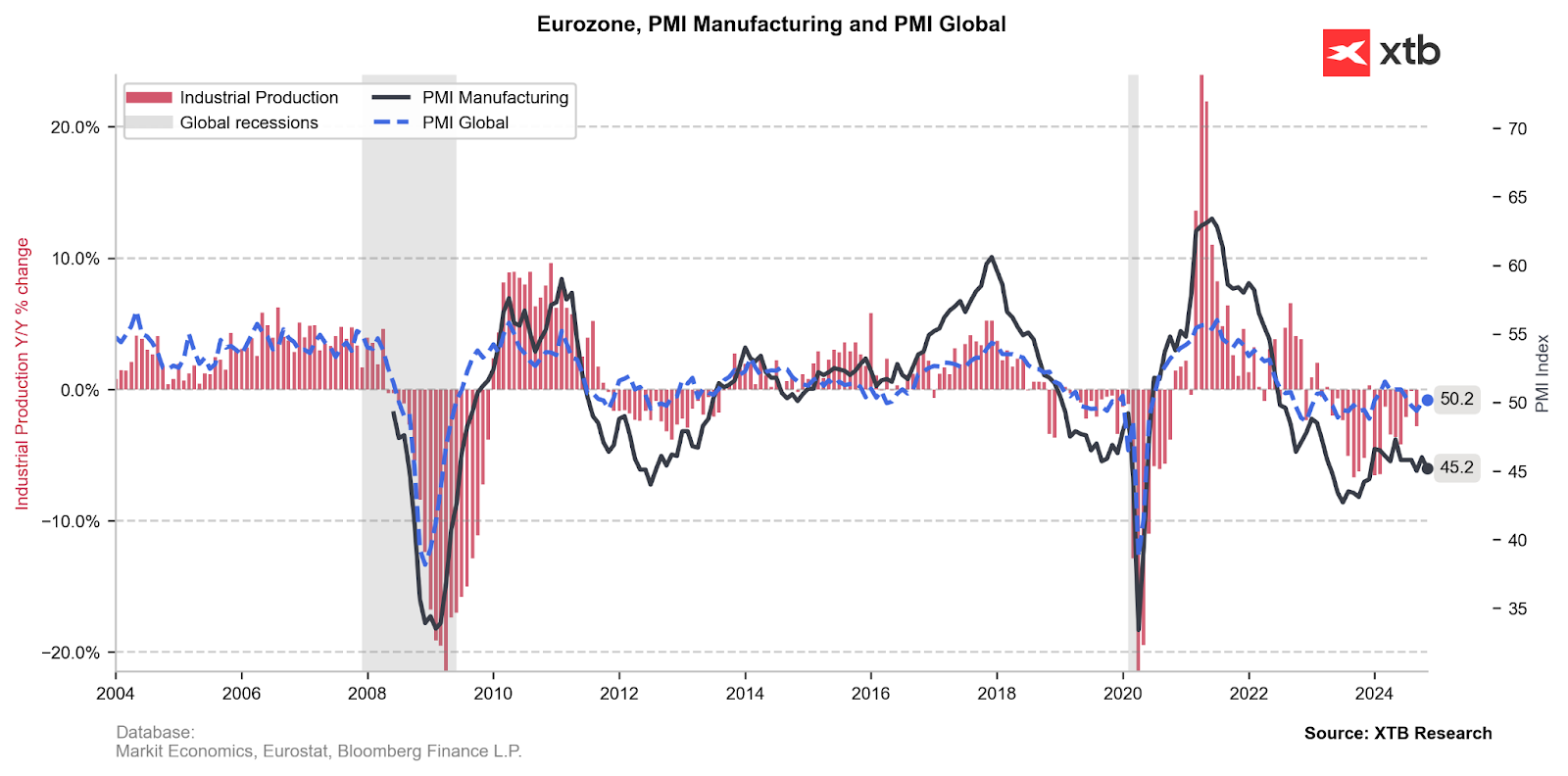

The PMI manufacturing index for the eurozone has remained in a downward trend since the beginning of this year. As you can see, there are no prospects for a recovery in European industry at this point. Source: Bloomberg Finance LP, XTB

ECB communication

So far, communication from the ECB has not been too dovish, despite the rather large economic problems in the eurozone. The ECB has hinted all along at considerable risks regarding inflation, but it is likely that the latest projections may show that the inflation problem could turn into a deflationary one. In view of this, there is the potential for a softer communication and indications of further interest rate cuts.

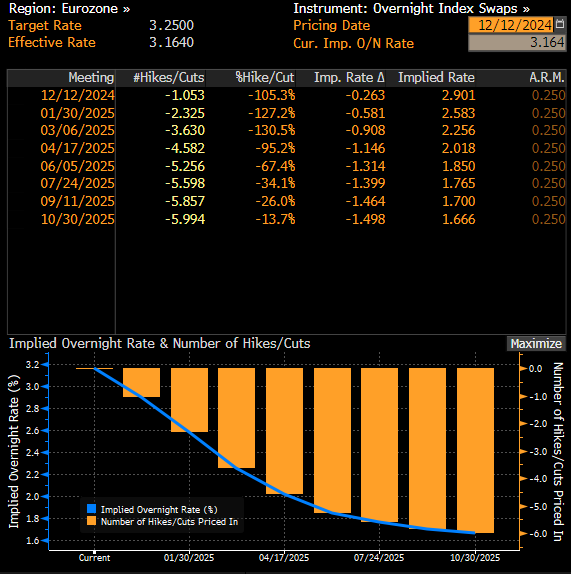

The deposit rate is expected to drop to 3% after today's meeting. The market sees the potential to go as low as 1.5% next year, but that would require a cut at almost every meeting. Bloomberg itself indicates that the cycle of cuts will end at 2.0%, which could potentially happen in April or June, depending on the scale of moves at today's and future meetings.

How might the euro react?

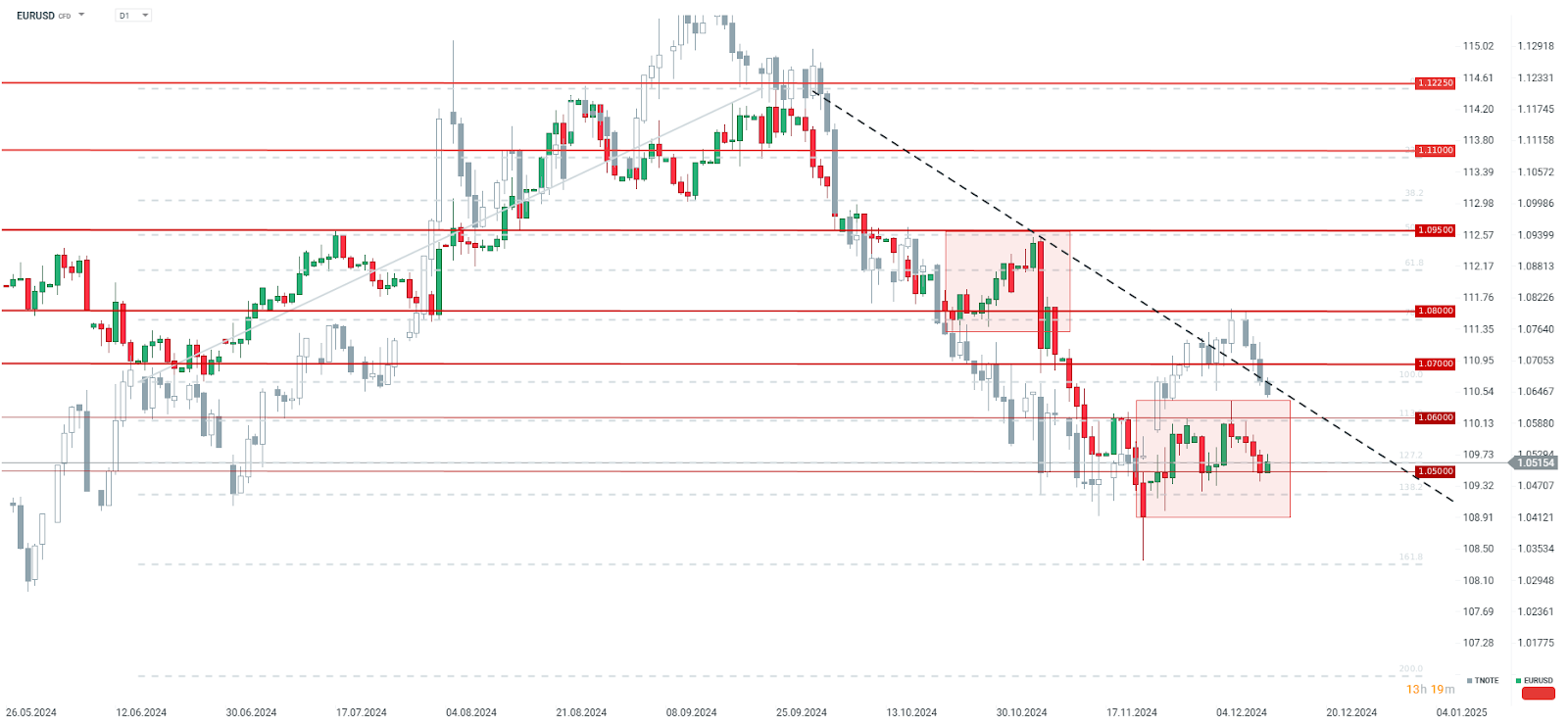

The euro remains quite oversold against the dollar, which is of course due to the weakness of the European currency, but also due to uncertainty about the future of US cuts. In the last few sessions, we have seen a marked increase in US bond yields. The EURUSD pair remains above the level of 1.0500, while a clear cut in macroeconomic forecasts and a change in communication to a more dovish one may cause the pair to go down near the level of 1.045. At the same time, however, volatility on the pair will increase next week with the anticipation of the Fed decision. However, if the ECB does not change its communication and continues to maintain the view of a cautious approach to interest rate cuts, then EURUSD could rise sharply. Nevertheless, the potential move should be limited to the 1.0600 level.

Source: xStation5

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.