A broad sell-off on the U.S. stock market in pre-market trading caused a drastic decline in the yields of U.S. bonds, pushing debt instrument prices to their highest levels since the beginning of 2025.

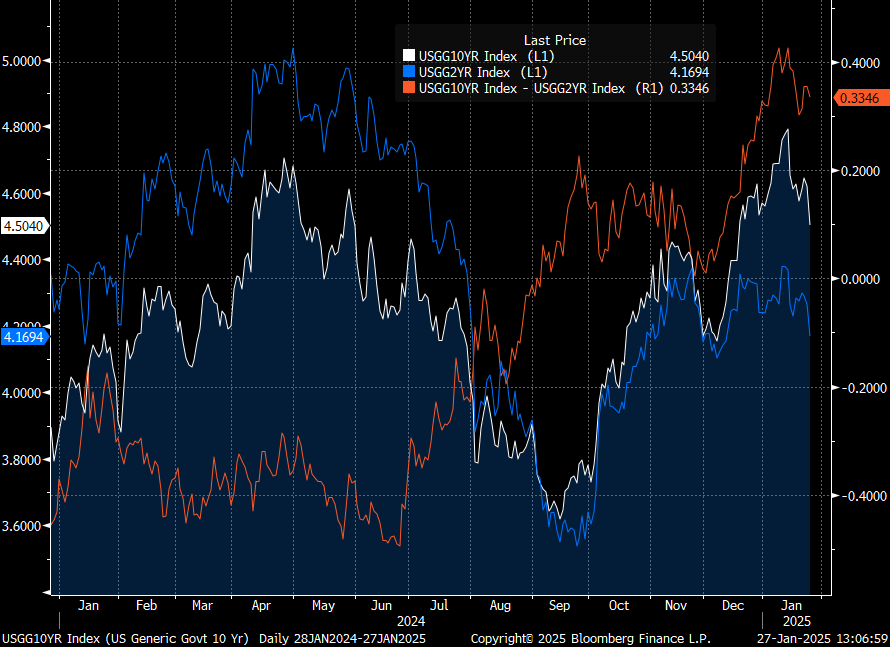

The 10-year Treasury bonds yield fell to 4.504%, approaching the psychological barrier of 4.5%, which had previously served as support for traders investing in the debt market. Meanwhile, the yield on 2-year Treasury bonds dropped to 4.17%, reducing the 10y-2y spread to 0.335% (the difference between 10-year and 2-year bond yields had peaked at the beginning of January, surpassing 0.4%).

Start investing today or test a free demo

Open real account TRY DEMO Download mobile app Download mobile app

Yields of U.S. 10-year bonds (white line), 2-year bonds (blue line), and the difference between 10-year and 2-year yields (red line). Source: Bloomberg Finance L.P.

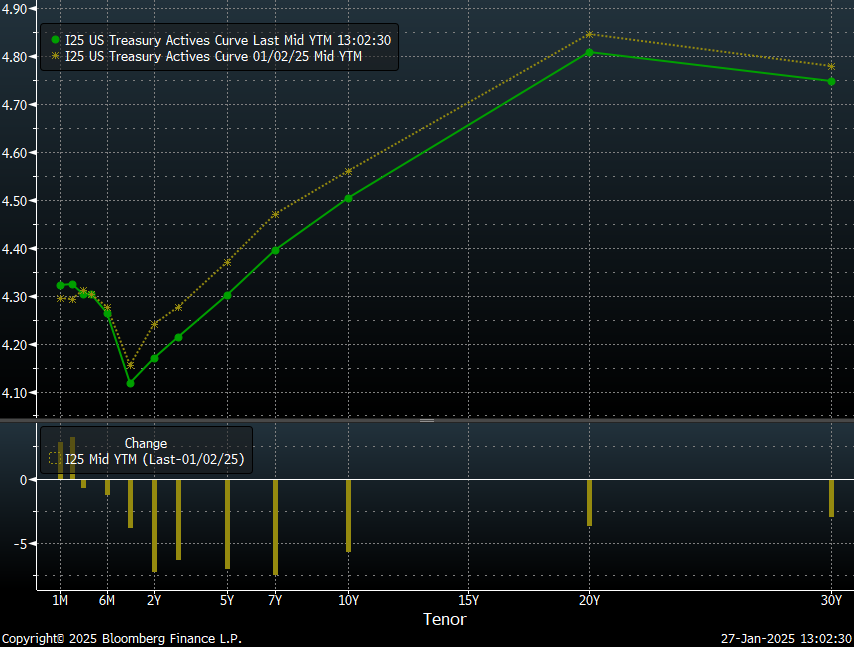

We also observe a shift in the yield curve compared to early January, when the curve inverted following increased market concerns about the future direction of the Federal Reserve's policy. The lack of change in the shape of the curve suggests that the source of today's yield declines is not a shift in investor sentiment toward the Fed's policy but rather an increase in risk-off strategies amid heavy selling in the U.S. stock market.

Comparison of yield curves from January 27 (green line) and January 2 (yellow line). Source: Bloomberg Finance L.P.

Such a strong move in bonds, driven by investor concerns, may prove premature, especially ahead of the Federal Reserve's meeting on Wednesday and its decision on interest rates. The key to sustaining this movement will be the tone of the Fed's decision, as markets currently price in no change in interest rates, and a rate cut in such an environment is highly unlikely. Investors will particularly focus on the Fed's explanations regarding the first week of Trump's policies and the president's push for lower interest rates.

For now, the decline in bond yields reduces the room for further price increases in the debt market in the event of a more dovish tone from the Fed. Instead, investors should expect this movement to strengthen under such a scenario rather than a drastic continuation.

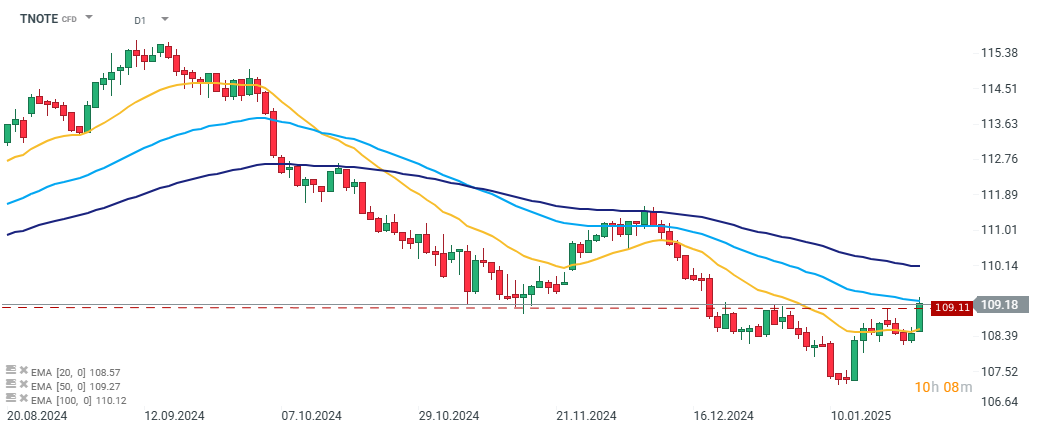

The U.S. bond futures contract approached a key resistance level at 109. At the same time, the contract's price stalled near the 50-session moving average (EMA50, light blue line on the chart). Source: xStation.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.