The increasing amount of digital data being produced, trends of remote work using new technologies and optimization of enterprise costs are driving more and more companies to use cloud computing services. While the pandemic was the catalyst for the rise of the cloud, long before 2020, cloud solutions were already being heralded as the "next big thing" in the IT sector. Despite the slowdown in the technology stock market in 2022, cloud revenues are still beating the margins of their other segments. To delve deeper into the investment appeal of cloud computing, it is useful to first understand the real meaning and prospects for the technology.

What's driving cloud computing growth?

The popularity of cloud computing in business continues to grow. The technology allows businesses to store servers and data off-site, in secure data centers that users can access via the Internet. The cloud enables companies to improve customer experience, increase productivity, reduce costs and help generate revenue by enabling faster time-to-market.There are several key cross-industry global trends that are driving cloud adoption.

Digitization

The demand for anytime, anywhere access to information and the increasing amount of time spent online by both private users and businesses has become the new normal of the third decade of the 21st century. Customers expect to be digitally connected to the world, and companies from all over the world are conducting business online. Opportunities are opening up for companies to connect devices as part of the "Internet of Things." From capturing vast amounts of information, entering new markets, transforming existing products to introducing new business models. The evolution of digital business poses a major challenge to corporate IT in providing solutions that can meet bandwidth and increasingly high security requirements.

Data growth

As digitization continues, the volume of data and interactions is also growing exponentially. More than 90 million children are born each year and are expected to create an average of 600 MB of data each day of their lives. In addition, it is estimated that nearly 10 exabytes of new information will be created in 2021 (1 exabyte is the equivalent of roughly 25 billion DVDs), and according to current projections, data growth will double every two years. The growth of data worldwide is placing limits on the capacity of corporate data centers stored on disk. The move to the cloud provides the flexibility to add new storage and new computers to process the exponential growth of information.

Artificial intelligence (AI) and machine learning (ML)

AI remains an overarching category within computer science. The development of artificial intelligence (AI) has already been referred to as the fourth industrial revolution. The largest amounts of funding are flowing into the machine learning segment, which give computers the ability to improve themselves. Machine learning is inextricably linked to the development of the Big Data and cloud computing segment of recent years because most algorithms are based on large amounts of data. Technology powerhouses such as Google, Amazon and Microsoft have made computing power available through the availability of graphics processing unit (GPU) hardware, which is ideal for implementing ML in large data sets. Previously, this revolution would have required huge capital expenditures and would have been a niche. In addition, these vendors have made their machine learning platforms available and provided cloud services, making these capabilities much more readily available and less expensive for enterprises.

Cost optimization

Controlling expenses and reducing them while maintaining quality and competitiveness is, of course, a task for any technology company. The cloud sector is also growing because it simply pays for itself. Traditional on-premises IT systems typically involve capital expenditures for hardware, software, depreciation. Cloud services do not involve capital expenditures for hardware and software; rather, their cost is based on platform usage and is strictly demand-driven.

Application programming interfaces (API)

APIs make it possible to connect information systems. This provides a platform for creating new digital platforms by composing solutions based on one or more internal or external interfaces. Companies with well-thought-out technology development strategies recognize the need to be part of a digital system. A good example of API adoption is the Payment Services Directive, which requires banks to allow regulated third-party providers (TPPs) to access customer bank accounts (with digital consent). If a customer has multiple bank accounts, TPPs can provide a single digital dashboard across all banks, using each bank's API. In this way, they automatically share potentially huge amounts of information, the ability to handle unpredictable load is crucial and creates pressure for cloud solutions.

Multi-cloud solutions and security

Demand for cloud-based security testing services for companies is growing regardless of their size, industry or business domain. As the threat of cyber-attacks increases, so does the demand for multi-layered cloud strategies. Cloud providers are highlighting security-related solutions. The risk of a hacking attack is decreasing.

Companies that don't want to share all their data with one provider can use multiple clouds, different companies at the same time. This is seen as a strategically secure way to optimize for specific needs and is often more cost-effective. The strategy of using several clouds simultaneously aims to improve business continuity, scaling IT and software resources. It also helps avoid problematic dependence on a single provider, reduces the cost of software operations and storage capacity. Analyst firm Gartner predicts that by 2025, 90% of enterprises will have deployed multi-cloud solutions, with smaller cloud providers like Snowflake and Cloudflare also likely to benefit.

- More than 90% of all business workloads are now processed in the cloud (75% are SaaS)

- Google Drive is the largest cloud storage service, with more than 2 billion users

- Analysts estimate that the cloud computing market will grow to $832 billion by 2025

- North America dominates the cloud computing market, accounting for more than 60% of the global cloud market

Investing in cloud computing

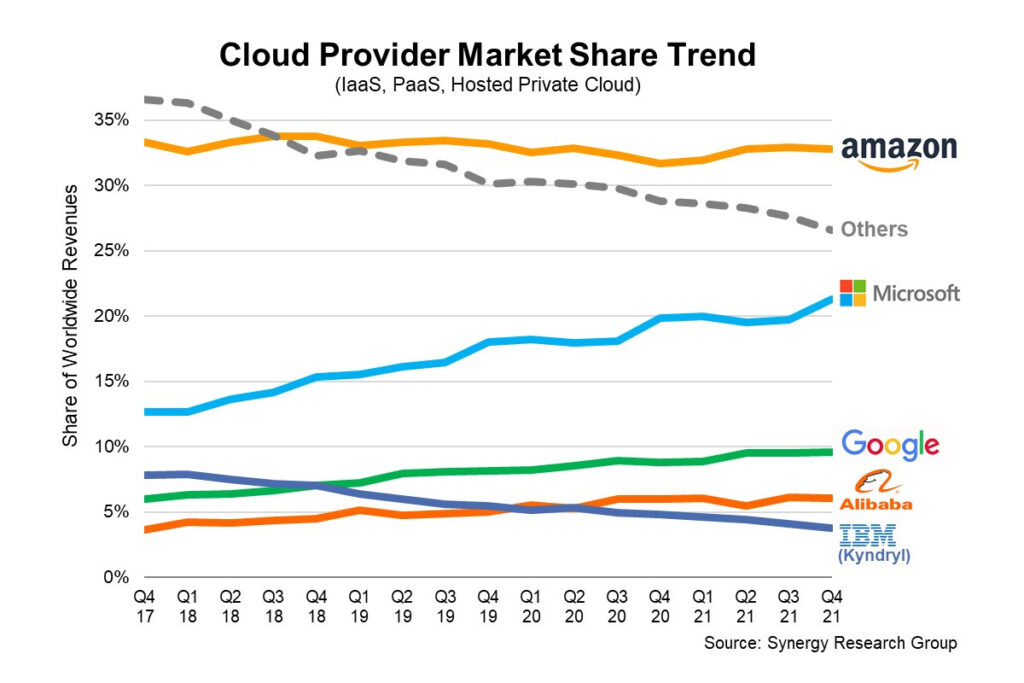

In addition to the number of uses and functionalities of cloud computing, investors are primarily interested in the profit that the shares of listed companies dominating the cloud business could provide them. Out of all the companies, we chose tech giants Microsoft (Azure)and Google (Google Cloud), whose revenue share ranks just behind Amazon (AWS) and has been growing exponentially since 2018. We omitted Amazon Web Services because this one has not been able to increase its revenue share of the cloud computing market against its competitors since the beginning of 2018. We also left out the other, smaller companies because the data shows that their share of global cloud revenue has been declining over the years, and is now around 22% compared to 37% in 2018.

Microsoft (MSFT.US) - Azure

A declining PC market, macroeconomic factors and a strong U.S. dollar have slowed Microsoft's revenue growth to levels not seen in five years. Still, the company managed to beat analysts' expectations in the third quarter of the year. Why? First of all, thanks to cloud computing.

Cloud computing is driving Microsoft's business. Cloud revenue in Q3 2022 was $25.7 billion which accounted for more than half of Microsoft's total revenue. Azure revenue grew 35%, year-over-year, compared to 50% growth a year earlier. Despite the slowdown in growth, cloud computing didn't 'flop' as much as the company's remaining business segments, such as Linkedin whose growth slowed to 17% vs. 42% a year earlier. The ongoing Azure cloud integration is also expected to help Microsoft's acquired developer platform Github, which has nearly 90 million users.

Microsoft expects slightly lower net margins from Azure in the near term, partly due to higher energy costs, which Microsoft estimated at roughly $250 million in additional expenses each quarter of the year. However, looking at the growing cloud computing market share and the nearly 40% drop in Microsoft's stock price, we can assume that the business at current valuations may attract interest from contrarian investors.

Microsoft (MSFT.US) stock price chart, W1 interval. The stock is in a downtrend, which stopped at the key support of the 200-session moving average (red), on the weekly interval. Microsoft's shares are trading near a 35% discount from their peaks in the fall of 2021. The price-to-earnings ratio is about 10% higher than the index average for NASDAQ companies, and the price-to-book value ratio is trading around 10 points, at a nearly 100% premium to the index average. Source: xStation5

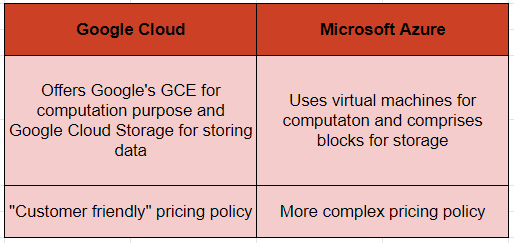

Alphabet (GOOGL.US) - Google Cloud

Google's cloud solutions are aimed at the largest enterprises. Solutions unavailable from competitors, such as the efficient organization of hierarchies in project work and the automation or compression of selected data, make it possible to significantly accelerate work on the largest projects.

SAP loses 4% despite positive recommendation at Bernstein 📉

Ryanair at 5-month low 🚩Jet fuel price surge pressures aerospace industry

Wall Street tries to stop the sell-off as oil surges 🚩Alibaba drops 7% amid earnings miss

Stock of the Week: Micron Technology at the Golden Moment of the Memory Cycle

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.