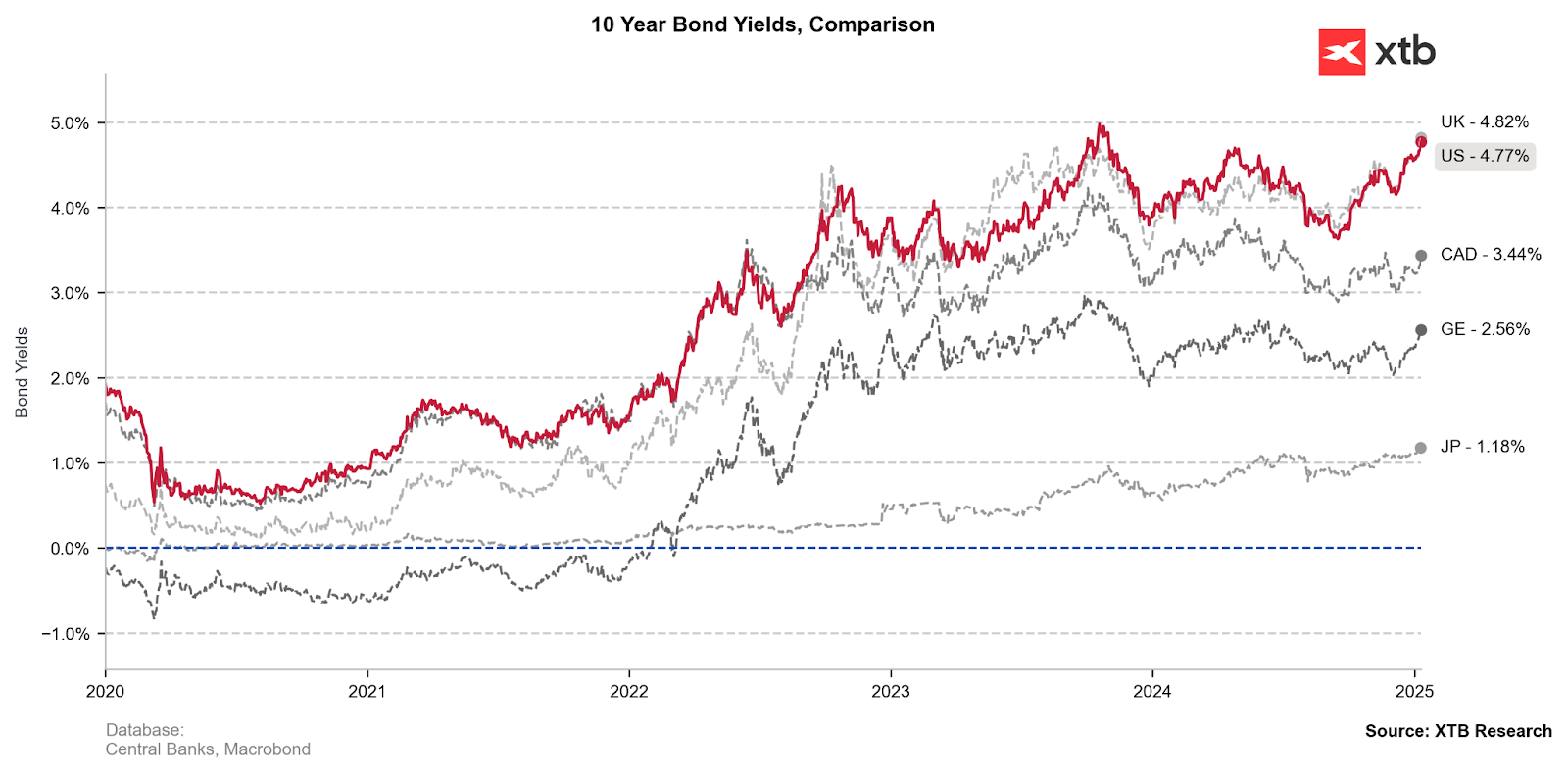

US bond yields have recently been recording record increases on the wave of investor concerns about the return of the Fed’s restrictive monetary policy in 2025. The two main factors supporting this scenario are the start of Donald Trump’s new term in January and the return of inflationary pressure. Essentially, the second factor is also somewhat related to Trump’s policy and fears of a strong turn by the US toward protectionism.

Yields on ten-year US bonds have remained in a strong upward trend basically since the announcement of the US presidential election results.

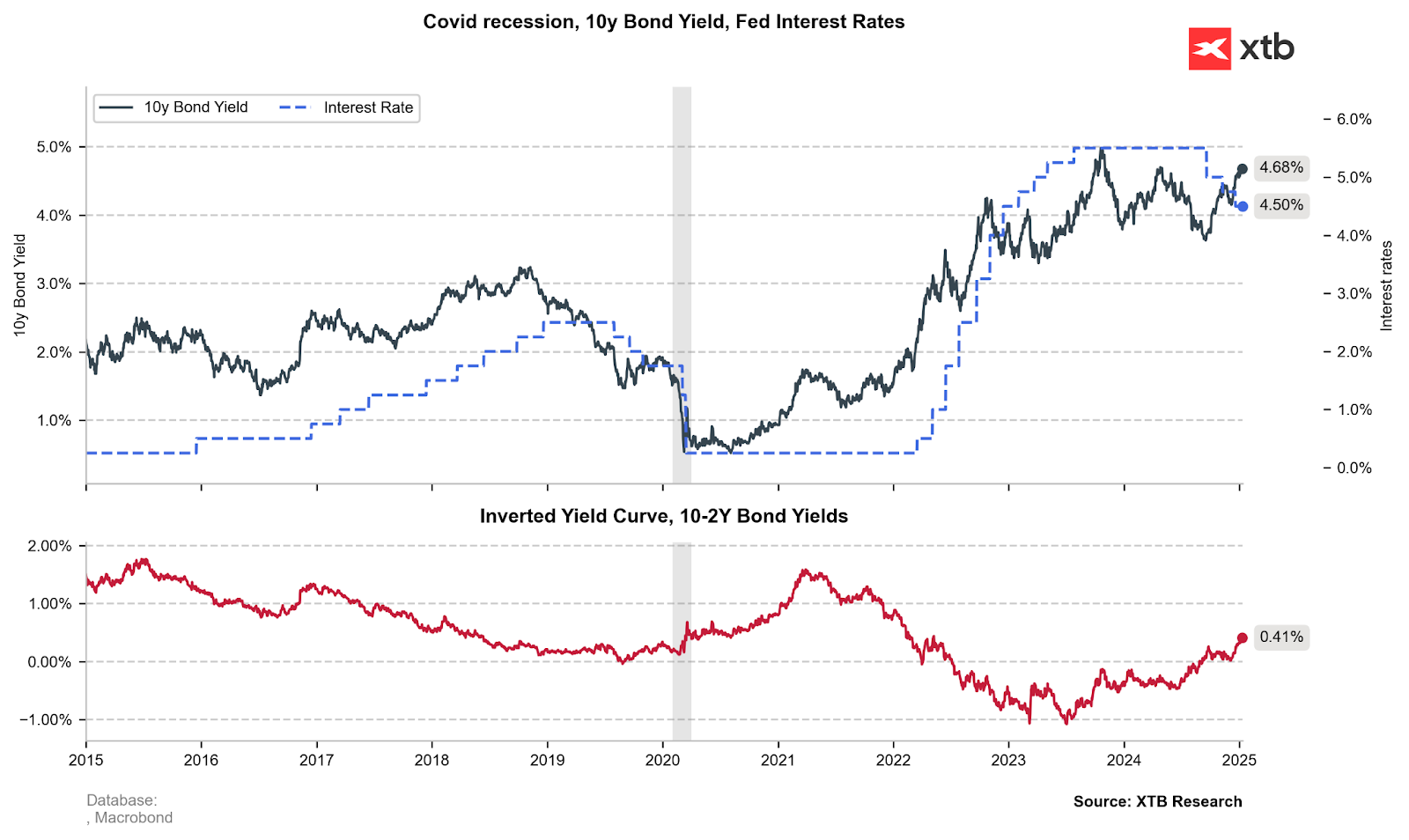

In recent months, we have experienced a rare event — an increase in ten-year bond yields accompanied by interest rate cuts. Investors have also lowered their expectations for rate cuts from two reductions just a week ago to barely one cut in the last quarter of 2025.

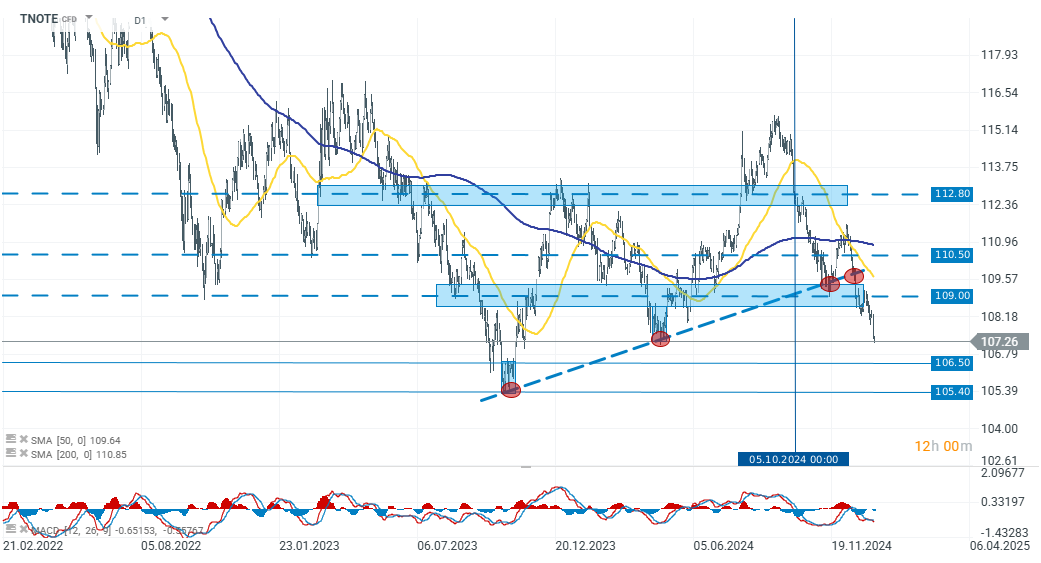

As a result, TNOTE prices were pushed to record-low levels and are now only 1.90% above the bottom of the interest rate hike cycle at the end of 2023. Currently, however, nothing indicates that the Fed is going to return to raising interest rates. In this regard, the most important factors will be inflation data and a sustained increase in price pressure — longer than two or three consecutive months. TNOTE quotes are losing another 0.15% today, dropping to 107.26 points. Source: xStation 5

Three markets to watch next week (09.02.2026)

US100 gains after the UoM report🗽Nvidia surges 5%

Market wrap: European indices attempt a rebound after Wall Street’s record selloff 🔨

📈Wall Street rebounds, VIX slips 5% 🗽What does US earnings season show us?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.