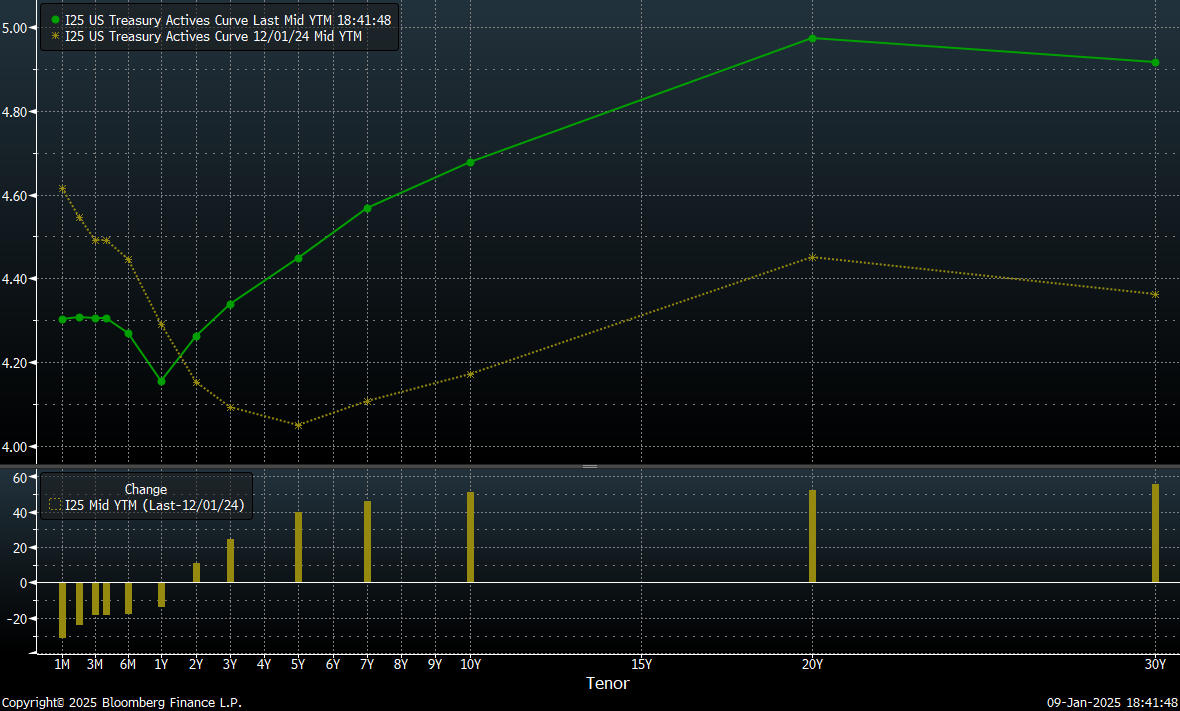

The US long term treasury yields have seen a sharp rise over the past month, partly driven by growing market concerns about inflation and the Fed's future decisions. However, the current steepening of the yield curve compared to December 2024, supported by both the sharp movement in long-term bond yields and the decline in yields on shorter-term bonds, raises questions about the future direction of investor movements and casts doubt on the extent of the market's response.

Today's yield curve (green line on the chart) and the yield curve from December 1, 2024 (yellow line on the chart). Source: Bloomberg Finance L.P.

Wednesday's movement, driven by concerns over Donald Trump's policies and the potential introduction of drastic tariffs targeting both the political allies and economic opponents of the U.S., pushed the 10-year bond yields to 4.728%, surpassing the April peaks on a yearly basis. This marks the highest level since the October 2023 peak, which came shortly after the end of the fastest interest rate hike cycle of the 21st century. Such a yield movement could serve as a basis for taking long positions by funds looking to go against market sentiment. Any failure of the risks associated with Trump's announcements to fully materialize would leave room for yields to decline, even in the face of a slower rate-cutting cycle by the Fed.

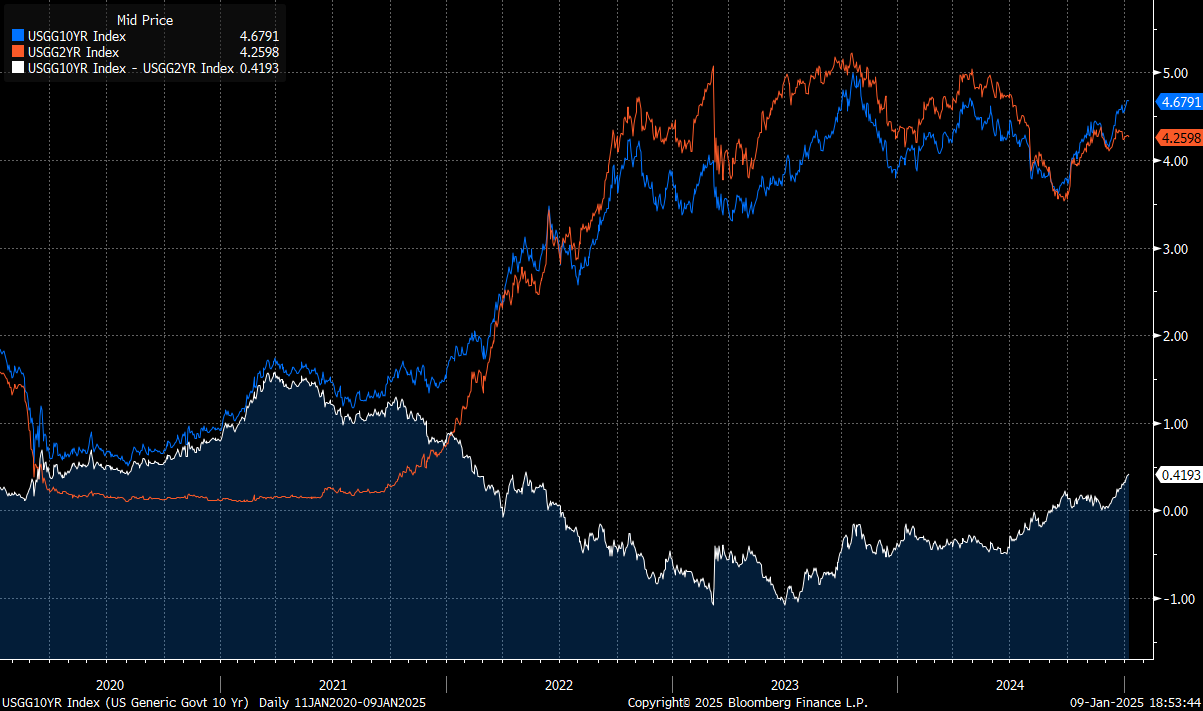

It is also worth noting that recent movements in the bond market have led to the highest value spread between 10-year and 2-year treasury yields since 2022, which currently stands at 41.9 basis points. The spread value returned above zero in the last quarter 2024 after approximately two years of being below zero. A strong upward movement of the spread, combined with the stabilization of 2-year U.S. bond yields around 4.26%, could create additional pressure to reverse the 10-year yield impulse back to 4.3%.

The U.S. 2-year Treasury and 10-year Treasury yields and their spread over the last 5 years. Source: Bloomberg Finance L.P.

It is worth noting, however, that if market concerns are realized, such as the imposition of broad tariffs, a strong labor market is maintained, and inflationary pressures return, the yields on short-term bonds may continue to rise at a similar pace as long-term ones. As a result, instead of a narrowing of the spread due to a decline in 10-year bond yields, we could see the spread close from the bottom due to the rise in 2-year bond yields.

The futures price of U.S. 10-year bonds approached a key support level of 108.02 yesterday. If this level is breached and the downward trend continues, the next significant support will be the April lows around 107.37, which represent the last support before the lows of 2023, marking the lowest level of the contract since 2006. Source: xStation

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

BREAKING: US100 jumps amid stronger than expected US NFP report

Market wrap: Oil gains amid US - Iran tensions 📈 European indices muted before US NFP report

Daily summary: Weak US data drags markets down, precious metals under pressure again!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.