- Yesterday's session on Wall Street overall saw most benchmarks close slightly higher. The Nasdaq gained 0.32% at the end of the day, the S&P500 added 0.14%, the Russell 2000 gained 0.27%, while the Dow Jones index lost 0.02%.

- Futures point to a higher opening of today's session on the Old Continent and the US.

- The RBNZ did not change interest rates in New Zealand, thus keeping the main rate at 5.50%. The decision is in line with market forecasts.

- However, the New Zealand dollar is gaining ground in the face of hawkish comments in the report to the decision. Bankers indicate that rates will remain elevated for an extended period of time.

- The Bank of Canada will also decide on interest rates today.

- The CPI report from the US, the BoC decision and the FOMC Minutes are the most important readings of the day.

- Rating agency Fitch maintained China's rating at A+, but the outlook index was downgraded to negative.

- BoJ Governor Ueda said he would not change monetary policy just to deal directly with currency movements. Accommodative financial conditions will be maintained for now, according to his assessment.

- Morgan Stanley raised the upper end of its Brent crude oil price forecast range to $94 per barrel from its earlier estimate of $90.

- API data yesterday pointed to a larger increase in US crude inventories.

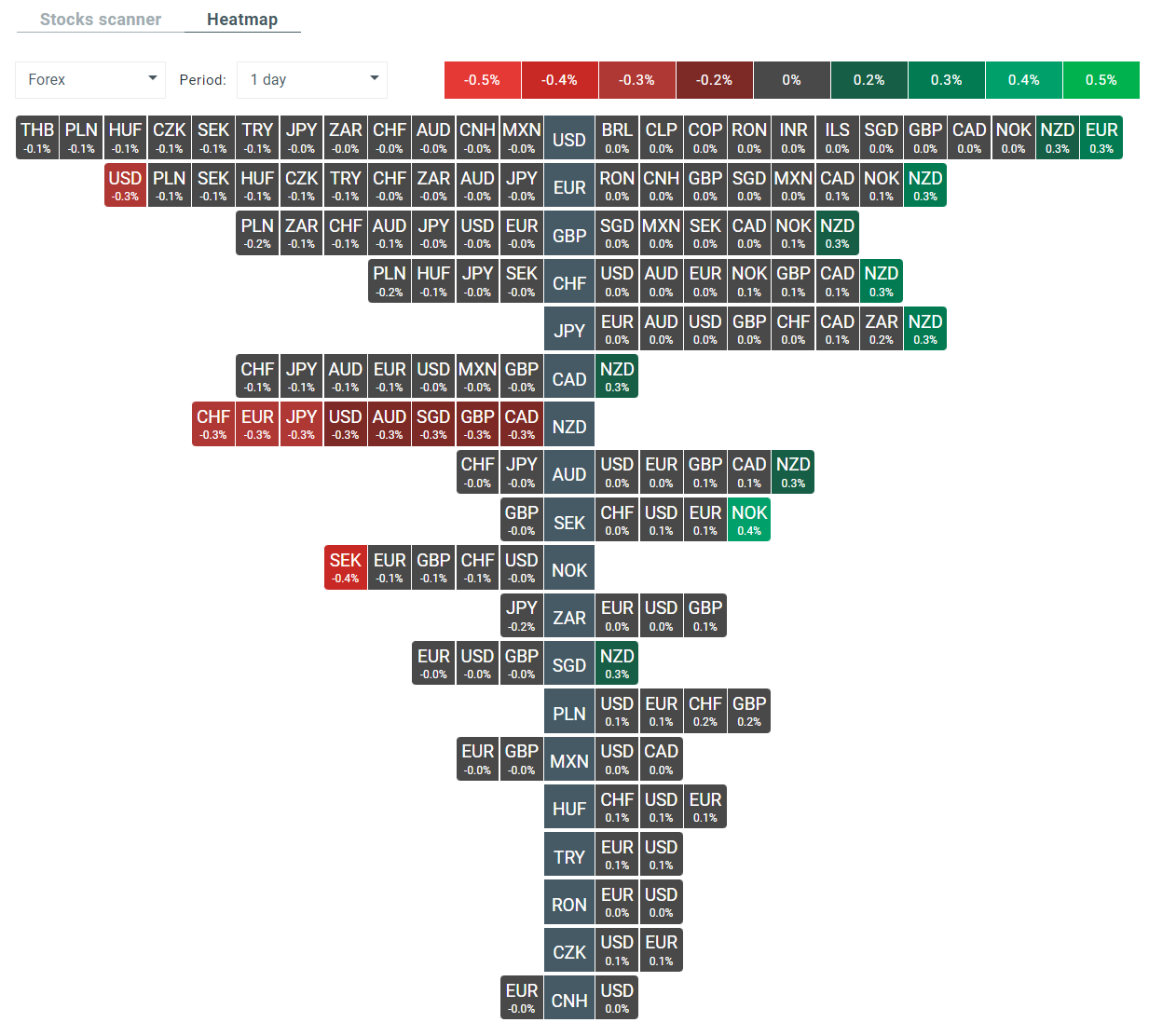

- In the FX market, the previously mentioned NZD is leading the way. Larger declines are seen primarily in the Australian dollar and the Japanese yen.

Volatility heatmap on the FX market at the moment. Source: xStation

BREAKING: US100 jumps amid stronger than expected US NFP report

Economic calendar: NFP data and US oil inventory report 💡

Morning Wrap: Dollar in a trap, all eyes on NFP 🏛️(February 11, 2026)

BREAKING: US RETAIL SALES BELOW EXPECTATIONS