Shares of Beyond Meat (BYND.US), a producer of high-protein, plant-based meat substitutes, are gaining more than 50% today in pre-opening Wall Street trading. The company is trying to recover from a period of high costs and subdued demand for expensive plant-based products. While the difficulties it is experiencing are definitely not over, investors are hopeful for a gradual improvement in profitability. The company's shares have experienced a massive sell-off in recent years, during which the company's capitalization has fallen from more than $14 billion in 2020 to less than $500 million today. Why so much euphoria after the quarterly results, and will consumers 'flip' to plant-based meat again, for the sake of their own health?

Beyond is not changing its strategy - it is refining it

In the Beyond Meat we can find virtually everything. From euphoria, to panic and allegations, to allegedly meat and pharmaceutical sector lobbing of negative research and opinions about 'chemical-laden' plant-based products. The company does not intend to abandon its existing strategy, instead it wants to develop it and believes in its validity. It has improved the recipe of its flagship 'plant-based burgers' by reducing sodium content and adding avocado oil, bean and red lentil protein. The product will be available in stores in the spring, and the company believes it will benefit sales. According to director Ethan Brown, the company needs to present such products so that their 'healthfulness' can never be questioned. Investors are beginning to like this approach. The new burger is expected to be a truly revolutionary step forward in his opinion. For a long time, allegations about the superiority of real meat, over its products, have been hitting the entire business model and expansion of the industry. Especially in the US.

In response, Beyond has collaborated on a new burger product with ... Stanford University School of Medicine and renowned nutritionists. In this way, the company doesn't want to leave critics with any arguments. It is aware that the bulk of its consumers want to choose meat substitutes purely because of diet and its impact on health. Its latest marketing campaign has focused on Beyond Steak, which has been deemed "heart healthy" by the American Heart Association (AHA). However, difficulties may arise in this field as well. A Mintel study last year indicated that nutrition is the second biggest reason (35%) for consumers' aversion to plant-based meat. In 2020, half of US consumers considered plant-based alternatives healthy. In 2022, it was only 38%. Beyond Meat CEO Ethan Brown echoed his concerns, from the previous quarter, estimating that this is the result of lobbying by hostile industries.

Will dormant demand wake up?

The vegetable meat category, has lost consumer interest in recent years. Not necessarily for taste or moral reasons. Raging inflation has depleted consumers' wallets, hitting discretionary spending; also the demand for expensive meat substitutes. Now inflation is gradually falling, giving hope for positive growth in real earnings. This could bring favorable momentum to the company, just as the expected easing of monetary policy could give it more breathing room in terms of servicing its high debt.

According to data provided by Circan, as of January 28, 2024, retail sales of alternative meat products fell 33.6% year-on-year.

While this does not represent a favorable environment for growth, these figures alone do not prejudge dynamics for the rest of the year and beyond. Moreover, they may in time support growth driven by the 'low base;' effect. The company is targeting the global market; sales in the States, where 'steaks' still dominate tables, remain subdued. Interestingly, in Europe where consumers appear to be in weaker shape than in the U.S., demand for its products has remained fairly stable. This only underscores that the niche market for meat substitutes rules.

Business focus on Europe

With the 'polarization of society and the politicization of the US meat market' management intends to focus on the European market. This is indicated by the company's own comments and the closure of production of the plant-based beef substitute 'jerky', which had been in production since 2022, in partnership with PepsiCo. Despite the product's considerable growth potential, particularly in the States. Fundamental changes in the business, however, are focused on Europe, and in the context of the lack of profitability, the company must carefully choose its expansion territory. The company also assessed that cooperation with McDonald's has a positive impact on demand, on the Old Continent. Beyond Meat's U.S. market saw a 32% year-on-year decline in sales, in 2023. Despite lower product prices, revenues fell 27%. Retail sales of vegetable meat by all producers in the U.S., according to Circan's research estimates, fell by about 11% year-on-year in January 2024, to about $1 billion. Not surprisingly, the company does not intend to expand more widely in a market that does not seem promising to it.

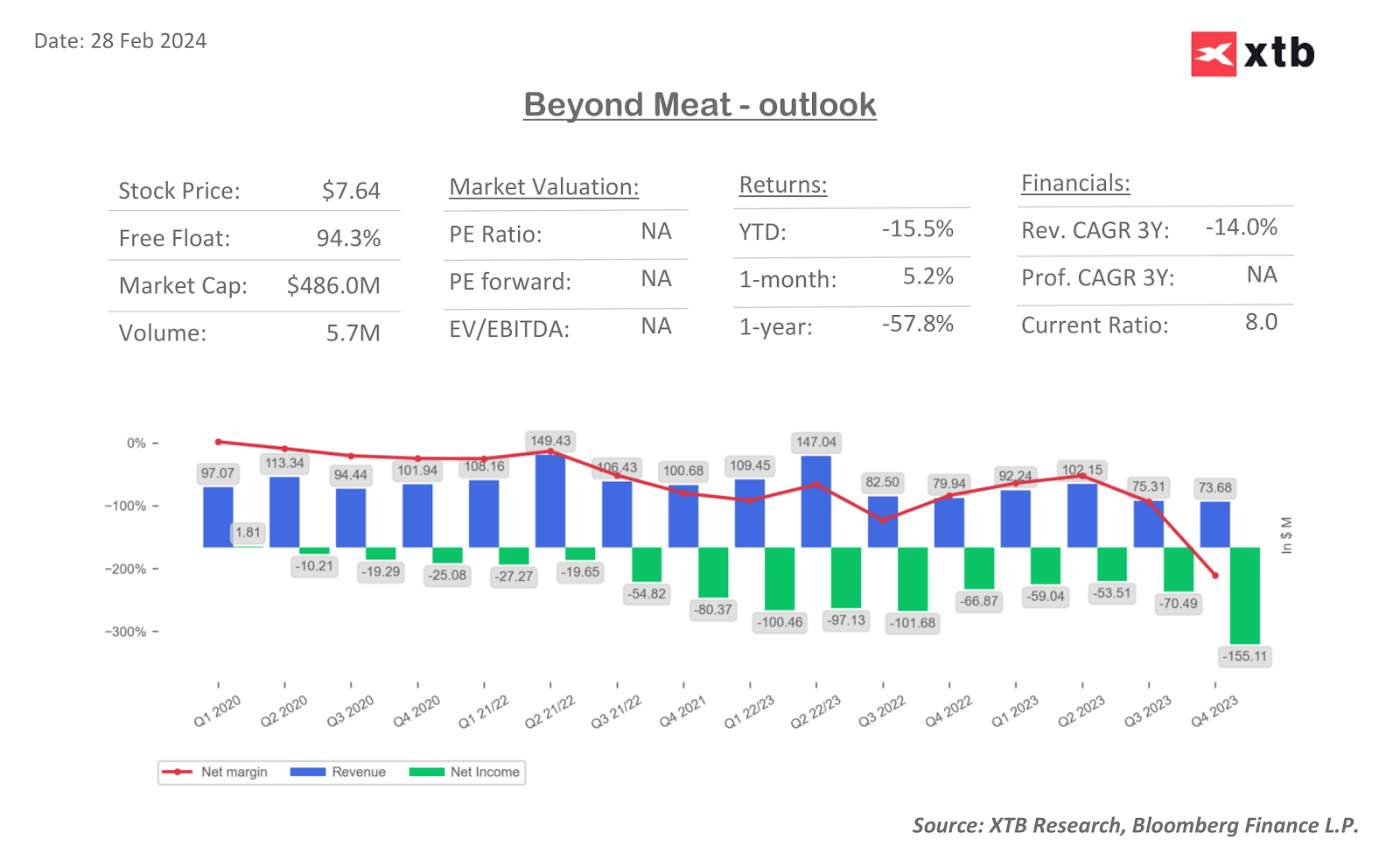

Meanwhile, Beyond's 2023 losses narrowed by 2.5% year-on-year to $338 million. Yes, this is not a great result, all the more so given its debt of about $1.1 billion. However, it seems that the restructuring measures and cost-cutting in 2023 may have a positive impact on improving margins, in the new year. Also, the 85% y/y decline in investments confirms that the company intends to focus on optimizing operations and only later consider expansions. Beyond Meat's net losses in the fourth quarter, doubled quarter-on-quarter, but this was heavily influenced by one-time charges of $85 million. The company paid them as part of a review of its global operations in 2023. The review was launched last November to reassess elements of the business that are not in line with profitability plans (potential restructuring of operations in China).

Q4 weak, but Wall Street 'wants to believe'

Beyond Meat reported higher-than-expected sales in the fourth quarter and is planning price increases for 2024. The net loss in the final quarter of 2023 turned out to be larger than estimated, but the market marginalized the significance of this, thanks to comments from the CEO. In his view, the company will sharply reduce operating costs and will use cash in a limited way this year. In the last quarter, an environment of lower demand meant the company had to cut prices for customers like McDonald's and Yum! chains. 2024 could give the company more breathing room and improve net earnings.

Management estimated that layoffs announced in 2023 have eased pressure on margins. Sales volumes in Q4 2023 rose 8% year-on-year, compared to a 3.5% increase in Q3. Q4 revenues fell 7.8% year-on-year, to $83.7 million, but beat forecasts of $66.7 million and proved much lower than the average annual decline of 18%, for all of 2023. Quarterly revenue fell only 2% versus a 26% decline between Q2 and Q3 of 2023.

Loss per share was $0.92 versus $0.88 forecast. The company's full-year revenue estimate of $315 million to $345 million fell short of expectations of $343 million. The results themselves admittedly did not show a fundamental improvement in the business, but the momentum, while weak, creates room for improvement. In the quarters ahead, Wall Street will be watching net income closely in particular, verifying whether Brown's comments about cost reductions, the catalyst of the new Beyond IV burger and adjusting production volumes to meet demand will be reflected in future results. Investors have decided to believe into a more optimistic future this time around, with the stock rebounding from extreme oversold levels.

Beyond Meat chart (D interval)

If the stock opens near $11 per share, the 200-session simple moving average (red line) will be broken, signaling that the downward trend may be reversed.

Source: xStation5

After a temporary flash of net profit, the company entered a disastrous streak of mounting losses in 2020. The valuation is weighed down by high debt, but investors are beginning to reexamine the prospects for its business, after years of disastrous declines and the actions of management, which, despite the adversity, is sticking to its original goals in terms of product quality and business model; emphasizing confidence in a health-promoting alternative to meat products.

Source: XTB Reserach, Bloomberg Finance LP

XTB Financial Markets Analyst Eryk Szmyd

Daily summary: Silver plunges 9% 🚨Indices, crypto and precious metals under pressure

Does the current sell-off signal the end of quantum companies?

Howmet Aerospace surges 10% after earnings reaching $100 bilion market cap 📈

US Open: Cisco Systems slides 10% after earnings 📉 Mixed sentiments on Wall Street