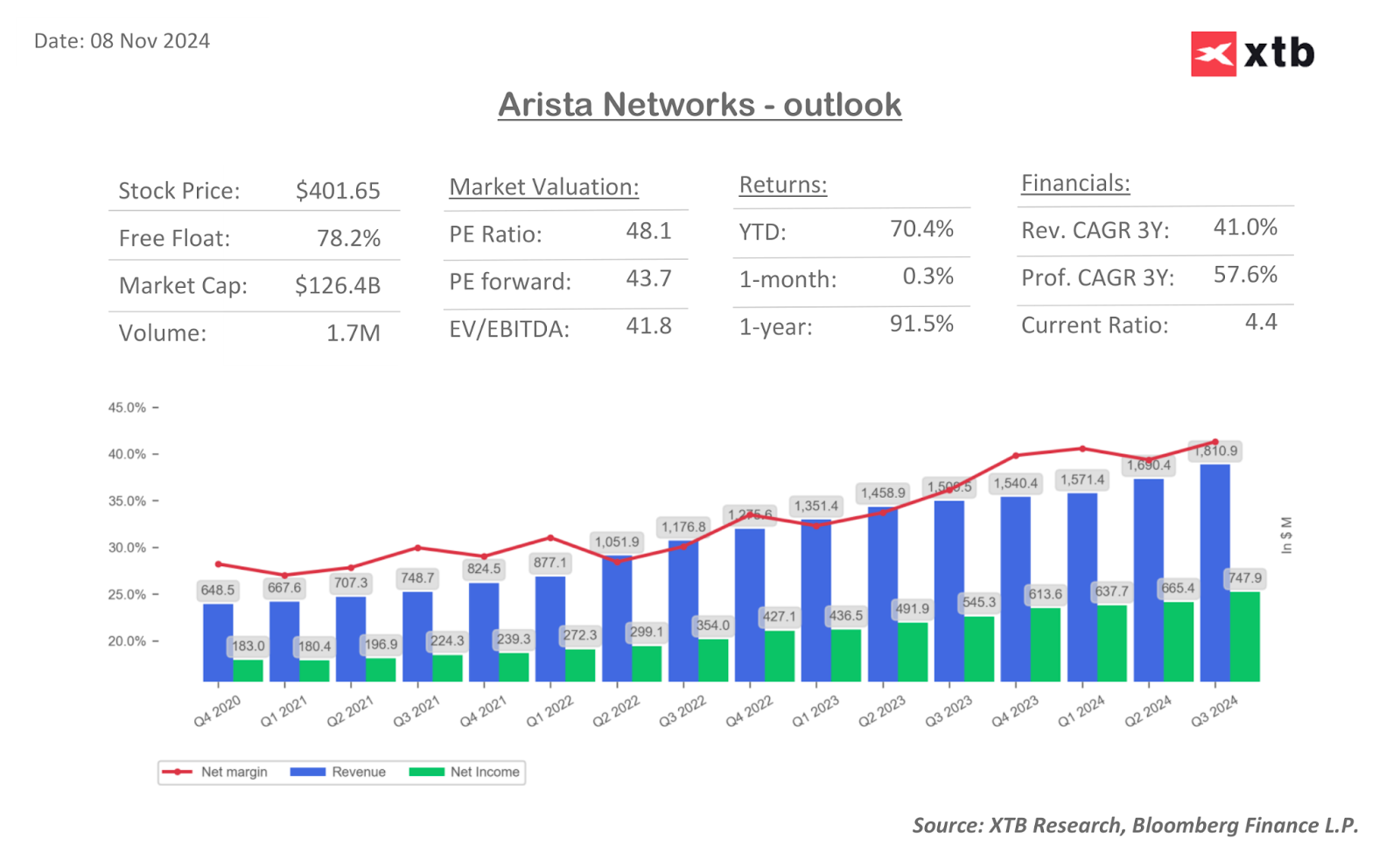

Arista Networks (ANET.US) shares are down more than 7%, despite Q3 earnings beating expectations. The decline is mainly due to the 2025 revenue forecast, which was lowered compared to market expectations.

The company surpassed market estimates across most key financial metrics. Revenue grew by 20% year-over-year to $1.81 billion (versus the forecasted $1.75 billion), with its crucial product revenue segment climbing to $1.52 billion. Additionally, the company maintained cost discipline, allowing it to raise its operating margin to 49.1% (compared to the projected 44.6%). Furthermore, the company announced acquiring a fifth major client in the AI segment, which will be included in its 2025 results.

Despite the better-than-expected third-quarter results, cautious projections for 2025 led to investor reservations and sharper declines in the stock price. CEO Jayshree Ullal stated that Arista expects to reach $8 billion in revenue for 2025, falling short of the consensus of $8.12 billion. Moreover, the company anticipates a weaker-than-expected operating margin for the fourth quarter, possibly due to delayed recognition of operational costs.

Although the 2025 forecasts are lower, it is worth noting that Arista Networks has a track record of exceeding expectations, and more conservative projections for 2025 leave room for potential upward revisions as new clients and orders are secured. This outlook is supported by comments from the company emphasizing its AI network development, with key projects involving clients such as Microsoft and Meta potentially driving further growth.

FINANCIAL RESULTS 3Q24:

- Adjusted EPS $2.40 vs. $1.83 y/y, estimate $2.08

- Revenue $1.81 billion, +20% y/y, estimate $1.75 billion

- Product revenue $1.52 billion, +19% y/y, estimate $1.48 billion

- Service revenue $287.1 million, +28% y/y, estimate $269.7 million

- Cost of revenue $649.2 million, +14% y/y, estimate $634.7 million

- Product cost of revenue $593.3 million, +13% y/y, estimate $582.6 million

- Service cost of revenue $55.9 million, +26% y/y, estimate $53.8 million

- Adjusted operating margin 49.1% vs. 46.1% y/y, estimate 44.6%

- Adjusted gross margin 64.6% vs. 63.1% y/y

OUTLOOK FOR 2025:

- Revenue: 15-17% growth, estimate: 18%

Arista Networks (D1)

The stock has remained in a strong upward trend since the beginning of 2023, with prices breaking below the lower boundary of this trend only once during that period. Today’s sharp decline does not signal a definitive change in sentiment but merely brings the share price back to levels seen before the post-election rally. Investors should pay attention to the $383 level, which serves as the first significant resistance, followed by $373, which is defined by the local peak from June.

Source: xStation

US OPEN: Blowout Payrolls Signal Slower Path for Rate Cuts?

Market wrap: Oil gains amid US - Iran tensions 📈 European indices muted before US NFP report

Economic calendar: NFP data and US oil inventory report 💡

Daily summary: Weak US data drags markets down, precious metals under pressure again!