At 14:30, we will learn the CPI inflation reading for June in the US. Expectations indicate a significant decline, mainly due to a high base from last year. Although today's reading is unlikely to change the Fed's stance on a July rate hike, a very low reading and further decline in PPI inflation on Thursday could result in the rate hike at the end of this year being the last move by the US central bank.

What are our expectations?

- CPI inflation for June is expected to fall to 3.1% YoY (previously: 4.0% YoY)

- Monthly CPI: 0.3% MoM (previously: 0.1% MoM)

- Core CPI inflation is expected to drop to 5.0% YoY (previously: 5.3% YoY)

- Monthly core CPI: 0.3% MoM (previously: 0.4% MoM)

Quantitative models such as ECAN from Bloomberg and the Cleveland Fed indicate even greater declines in inflation, down to 3.0% YoY for the headline reading and 4.9% YoY for the core reading. At the same time, these models suggest that we may see lower monthly readings, around 0.2% MoM, mainly due to lower car prices, not to mention the high base with energy prices from last year. We are also witnessing a further slowdown in housing market price growth, including key factors affecting inflation, such as rental equivalents and actual rents. Furthermore, there is a significant decrease in inflation expectations among service sector entrepreneurs. A 3-month shift suggests that YoY CPI inflation could even drop to 2.5%. However, it should be noted that today's reading of headline inflation will most likely be a local low point for this year, assuming there won't be a monthly price decline.

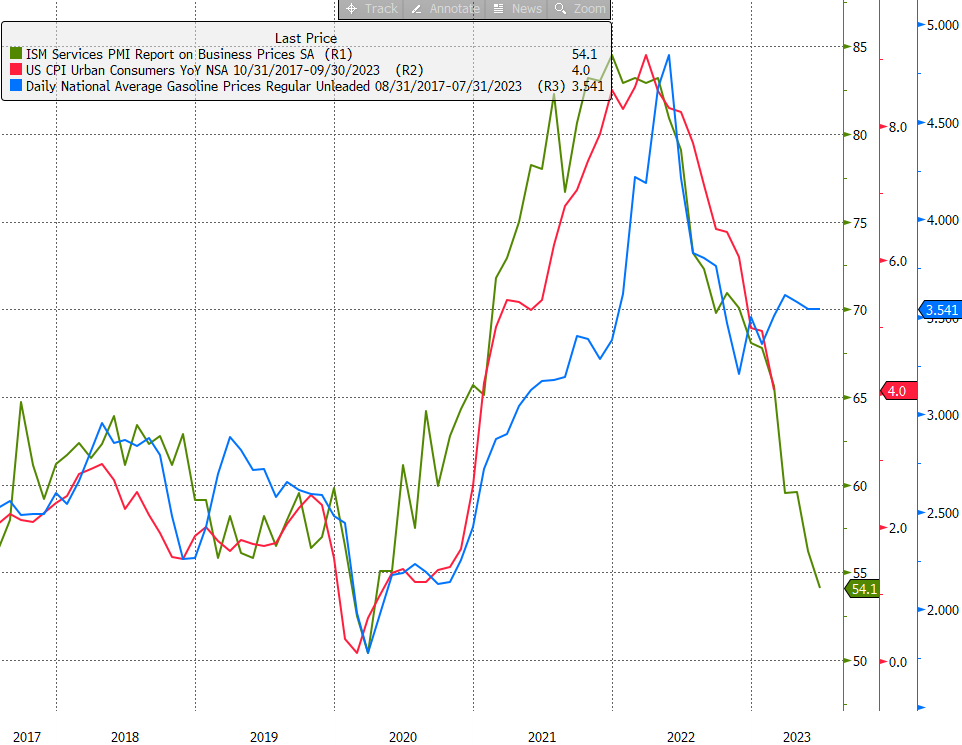

Services indicate that inflation could drop significantly. On the other hand, factors such as relatively stable fuel prices for many months may lead to an inflation rebound later in the year. Source: Bloomberg, XTB.

Services indicate that inflation could drop significantly. On the other hand, factors such as relatively stable fuel prices for many months may lead to an inflation rebound later in the year. Source: Bloomberg, XTB.

What else is worth to consider?

- Tomorrow we will learn the PPI inflation. It is expected to decrease to 0.2% YoY for final demand and reach a negative level for finished goods after the last reading at -0.9% YoY.

- We have recently observed a noticeable decline in health insurance-related inflation. Starting from October, health insurance will have a positive contribution to inflation, somewhat offsetting the impact of falling housing market inflation dynamics.

- BofA's analysis suggests that today's inflation is likely to hit a low point, considering the average monthly inflation growth of 0.2% that occurred before the pandemic. Inflation may still hit a low point this year if prices rise by an average of 0.0% MoM or 0.1% MoM. Assuming a 0.2% MoM scenario, BofA predicts inflation of around 3.9% YoY in January next year, which could be an argument for further rate hikes by the Fed.

Negative fuel contribution will most likely occur in June. Additionally, the Manheim index suggests a significant decline in inflation related to used cars. Source: Bloomberg, XTB.

Negative fuel contribution will most likely occur in June. Additionally, the Manheim index suggests a significant decline in inflation related to used cars. Source: Bloomberg, XTB.

How will the dollar behave?

EURUSD has recently shown a clear rebound in the past few sessions and has likely invalidated the RGR formation, with the neckline around the 1.0700 level. We also observe a noticeable decline in yields, which should support further weakness in the dollar. However, if today's inflation reading does not surprise with lower levels, the market may interpret it as the Fed's readiness for two rate hikes, so we cannot rule out a local peak during today's session. However, an important test will also take place tomorrow because theoretically, PPI inflation for final demand could fall into negative territory. In such a case, on the contrary this could set new local highs for EURUSD.

Source: xStation5

Source: xStation5

Live Trading - 2026.02.10.

Talpra Tréder - 2026.02.09.

Az EURUSD visszanyerte az 1,18-as szintet a kiváló német gyártási adatoknak köszönhetően 📈

Reggeli összefoglaló (05.02.2026)

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.