Report at 1:30 p.m. BST❗

Investors' attention today turns to inflation readings from the world's largest economies. The publication with the greatest market significance is, of course, US CPI inflation, which will be an important factor in shaping the Fed's future monetary policy and may prove to be a valuable reference for other central banks' decisions. Today's 1:30 p.m. BST release will create a lot of volatility in the broad market, so let's take a look at the most important data on the report.

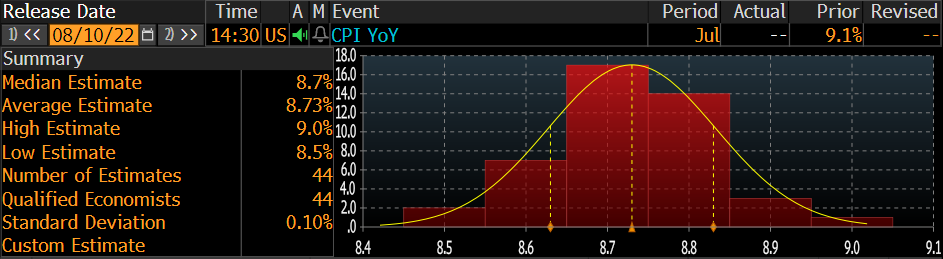

The consensus of analysts surveyed by Bloomberg assumes that the July inflation reading will reach 8.7% y/y, compared to an earlier reading of 9.1% y/y. However, we mark special attention to the small standard deviation of forecasts, which increases the chance of a plus/minus surprise. Source: Bloomberg

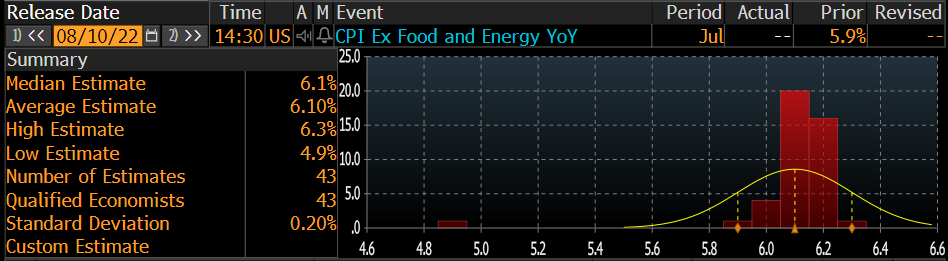

The forecasts for inflation readings excluding food and energy prices are slightly different. Here, analysts assembled by Bloomberg forecast an acceleration of inflation to 6.1% y/y, compared to an earlier reading of 5.9% y/y. This highlights the importance of especially oil and gasoline prices in the US as a factor creating inflation (average prices fell in July). Source: Bloomberg

Money market rates currently point to a 76% probability of a 75 basis point rate hike at the September FOMC meeting. Today's reading will certainly bring an update in market valuations. Source: Bloomberg

At the moment, stock markets are trading at mixed levels, the U.S. dollar is weakening against other currencies, and 10-year yields are rising slightly.

EURUSD pair rose slightly during today's session and is currently testing the upper limit of the triangle formation. Nevertheless, traders restrain themselves from taking larger transactions ahead of CPI release. Markets forecast that the annual inflation rate in the US will slow to 8.7% in July, however a significant downward surprise could reduce some pressure on the Fed and push USD even lower. On the other hand, a hotter-than-expected reading will reinforce the central bank's aggressive stance against surging inflation (especially given last week's strong NFP reading) and likely trigger another dollar rally. Source: xStation 5

Gazdasági naptár: Az amerikai CPI a figyelem középpontjában (2026.02.13.)

Gazdasági naptár: Az amerikai munkanélküli-segély kérelmek és EKB-beszédek adhatnak lélegzetvételnyi szünetet a piacoknak (2026.02.12.)

BREAKING: A font megdermedt a vártnál alacsonyabb brit GDP-adatok után 📉

Gazdasági naptár: NFP-adatok és amerikai olajkészlet-jelentés 💡

Ezen tartalmat az XTB S.A. készítette, amelynek székhelye Varsóban található a következő címen, Prosta 67, 00-838 Varsó, Lengyelország (KRS szám: 0000217580), és a lengyel pénzügyi hatóság (KNF) felügyeli (sz. DDM-M-4021-57-1/2005). Ezen tartalom a 2014/65/EU irányelvének, ami az Európai Parlament és a Tanács 2014. május 15-i határozata a pénzügyi eszközök piacairól , 24. cikkének (3) bekezdése , valamint a 2002/92 / EK irányelv és a 2011/61 / EU irányelv (MiFID II) szerint marketingkommunikációnak minősül, továbbá nem minősül befektetési tanácsadásnak vagy befektetési kutatásnak. A marketingkommunikáció nem befektetési ajánlás vagy információ, amely befektetési stratégiát javasol a következő rendeleteknek megfelelően, Az Európai Parlament és a Tanács 596/2014 / EU rendelete (2014. április 16.) a piaci visszaélésekről (a piaci visszaélésekről szóló rendelet), valamint a 2003/6 / EK európai parlamenti és tanácsi irányelv és a 2003/124 / EK bizottsági irányelvek hatályon kívül helyezéséről / EK, 2003/125 / EK és 2004/72 / EK, valamint az (EU) 2016/958 bizottsági felhatalmazáson alapuló rendelet (2016. március 9.) az 596/2014 / EU európai parlamenti és tanácsi rendeletnek a szabályozási technikai szabályozás tekintetében történő kiegészítéséről a befektetési ajánlások vagy a befektetési stratégiát javasló vagy javasló egyéb információk objektív bemutatására, valamint az egyes érdekek vagy összeférhetetlenség utáni jelek nyilvánosságra hozatalának technikai szabályaira vonatkozó szabványok vagy egyéb tanácsadás, ideértve a befektetési tanácsadást is, az A pénzügyi eszközök kereskedelméről szóló, 2005. július 29-i törvény (azaz a 2019. évi Lap, módosított 875 tétel). Ezen marketingkommunikáció a legnagyobb gondossággal, tárgyilagossággal készült, bemutatja azokat a tényeket, amelyek a szerző számára a készítés időpontjában ismertek voltak , valamint mindenféle értékelési elemtől mentes. A marketingkommunikáció az Ügyfél igényeinek, az egyéni pénzügyi helyzetének figyelembevétele nélkül készül, és semmilyen módon nem terjeszt elő befektetési stratégiát. A marketingkommunikáció nem minősül semmilyen pénzügyi eszköz eladási, felajánlási, feliratkozási, vásárlási felhívásának, hirdetésének vagy promóciójának. Az XTB S.A. nem vállal felelősséget az Ügyfél ezen marketingkommunikációban foglalt információk alapján tett cselekedeteiért vagy mulasztásaiért, különösen a pénzügyi eszközök megszerzéséért vagy elidegenítéséért. Abban az esetben, ha a marketingkommunikáció bármilyen információt tartalmaz az abban megjelölt pénzügyi eszközökkel kapcsolatos eredményekről, azok nem jelentenek garanciát vagy előrejelzést a jövőbeli eredményekkel kapcsolatban.